Why U.S. GoldMining Could Rebound If Gold Turns Bullish

Anthony Bradshaw

A Hold Rating for U.S. GoldMining Inc.

In this analysis, we recommend holding U.S. GoldMining Inc. (NASDAQ:USGO) shares which is a US gold operator that carries out exploration and development activities to open a gold mine in Alaska.

The updated rating represents a change from the previous rating of sell.

Compared to the previous assessment, the outlook for gold, the main target product of U.S. GoldMining Inc., has changed and now appears bright, with the demand for the precious metal as a safe-haven investment expected to be strong in the coming months.

Because the stock price is positively correlated with the price of gold that U.S. GoldMining Inc. develops in Alaska, shares are likely to follow the expected rise in the precious metal.

There is a chance that the retail investor can benefit significantly from holding U.S. GoldMining Inc.'s shares in his portfolio.

There is a chance that retail investors can benefit from having a position in U.S. GoldMining Inc. From these levels, which became surprisingly attractive after shares plunged 46.5% from the intraday peak of $17.24 apiece reached on May 10, 2023, the holding can deliver significant returns while the commodity is in a bull market, as this analysis expects.

Gold as a Safe Haven against Recession Headwinds

Despite the US Federal Reserve's very aggressive monetary policy to combat annual inflation, which reached its highest level in more than forty years in June 2022 due to the strong recovery from the Covid crisis, the energy crisis, and above all the war in Ukraine (after 19 months of conflict, the OECD and US Treasury Secretary Janet Yellen blame the war in Ukraine for inflation), economists are said to expect a soft landing for the economy rather than a recession.

A recession, that is, a regression in economic activity, usually follows a policy of raising interest rates implemented by the central bank to discourage consumption and investment (the YCharts shows that consumption was nearly 70% of US GDP as of June 2023). If people consume and businesses invest less due to increased borrowing costs, as demand for goods and services has meanwhile weakened, the negative dynamic is reflected in downward pressure on inflation (the rate of increase in the prices of goods and services).

Record high inflation evoked a strong sense of duty to guarantee price stability. That is why the Fed, in carrying out its mandate, pursued a policy of interest rate increases that has not been as drastic as the financial crisis of 2007/2008.

The normal course in such a situation is that after the monetary policy consequences have taken place, the next economic environment should not be a soft landing, but rather a significant regression of the business cycle, i.e., a recession.

Unlike the proponents of a soft landing, those who believe that the near future will have a dark recessionary character are gradually coming to light, and today we have the first names. The most prominent voices currently include economist David Rosenberg of Rosenberg Research (via this Business Insider article here) and Duke professor and Canadian economist Campbell Harvey (thanks to this Yahoo Finance article here), but it's likely that the list of proponents of the recession spreads over time.

This analysis is consistent with the views of economists David Rosenberg and Campbell Harvey, as analysts advocating the opposite soft-landing thesis, Goldman Sachs Group, Inc. (GS) being a prominent voice at the moment, appear to be making a mistake in their judgment.

GS's soft-landing thesis, which reduces the risk of recession to 15% (see Yahoo Finance here), is essentially based on a positive trend in income growth that would allow the economy to absorb the effects of the Fed's hawkish policy and high inflation by supporting consumption in a resilient manner.

However, there is a problem that undermines the validity of the scenario outlined by the GS analysts. When analysts point to the encouraging growth rate of US real disposable personal income of 4% in May 2023, they underestimate or seem to ignore a crucial factor: the sharp compression of real disposable income in the spring/summer of 2022 due to rising energy costs (see chart here from YCharts).

Given the magnitude of the increase in fossil fuel prices last year, the margin on real disposable personal income from 2022 to 2023 would likely be less pronounced or not occur at all without the 2022 energy crisis. This means that in reality the situation may be completely different than it seems at first glance, and this spending capacity cannot in any way allow consumption to continue to stay afloat in the coming months.

In addition, excess savings created during the COVID-19 pandemic are shrinking, possibly reflecting downward momentum in the U.S. real per capita disposable personal income curve, which contracted on a month-on-month basis in June 2023 (see chart here from YCharts).

Now that the soft-landing thesis has been seriously shaken, we are left with recessionary thoughts about possible future scenarios, while consumption actually seems to be giving anything but positive signals: as evidenced by recent quarterly earnings from online retailers Chewy (CHWY) and Target (TGT), which Yahoo Finance reports as a reliable indicator of U.S. consumption momentum, consumption among non-high-income households may be under pressure since discerning behaviors are detected in shopping activities in these company stores.

Thus, as mentioned above, the headwinds from the recession will trigger demand for safe-haven gold and its price should rise sharply.

The Ounce is Bound to Trade Higher Soon, So May Shares of U.S. GoldMining Inc.

Analysts at Trading Economics predict that the price of gold bullion will reach around $2,012 per ounce in a year, representing a good recovery from the current level of $1,909.43 per ounce at the time of writing.

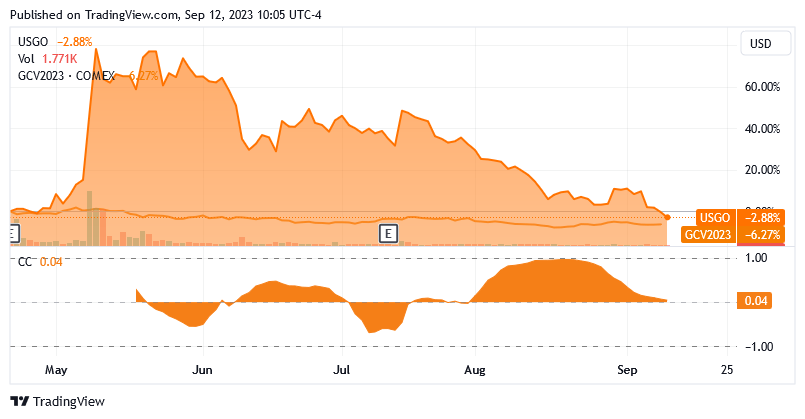

Backed by a strong positive correlation with the price of the commodity, as shown in the chart below from Seeking Alpha, shares of U.S. GoldMining Inc., listed on the Nasdaq stock exchange since the successful completion of the IPO last April, are also expected to experience recovery as well.

As you can see in the chart which compares USGO stock price with gold price measured by the benchmark of gold futures (GCV2023), the two securities have a strong positive correlation as evidenced by the yellow area underneath which has been mostly above zero so far.

Source: Seeking Alpha

The reason for making its share capital available for exchange on the American Stock Exchange since April 20, 2023 (the company reported via Seeking Alpha), was to raise an estimated $20 million in total funds, which the company intends to use to finance exploration and mining study activities, which are its primary focus in the Whistler Project in Alaska. To raise $20 million, the company offered 2 million units priced at $10 each. Each unit consisted of a common share traded on Nasdaq-CM under the symbol USGO and a warrant traded on Nasdaq-CM under the symbol USGOW. The holder of the warrant is entitled to purchase one common share of USGO stock at a price of $13, and this right can be exercised for a period of three years from the date of issuance.

U.S. GoldMining Inc.'s Mineral Operations in Alaska

It must also be remembered that U.S. GoldMining Inc. was formed from a spin-out of GoldMining (GLDG) - a Vancouver-based explorer and acquirer of gold properties in America - and that the latter is USGO's largest shareholder, owning around 80% of USGO's common shares after the IPO.

Whistler is the name of a 100% interest in a gold-copper exploration project currently covering approximately 53,700 acres in the Yentna mining district of Alaska.

The company will use the capital ($18.07 million in cash and no debt as of May 31, 2023, Q2-2023 report via Seeking Alpha indicates) to establish a gold equivalent-producing mine as the growth potential today is shown by approximately 3 million gold equivalent ounces of indicated resources and 6.4 million gold equivalent ounces of inferred resources.

Also, Whistler is a mineral resource found in gold-copper porphyry deposits. In addition, there are mineralized drill intersections that lie within several significant anomalies from a geophysical and geochemical point of view, but these require further drilling.

The site has adjacent infrastructure including runways, storage, drilling routes, and access to mineral deposits, as well as a seasonal winter road.

Currently, the resources are not the type by which the economic viability of the project can be demonstrated, and, in fact, no economic analysis is yet available to help estimate the value to Whistler.

In addition to upgrading the resources from 'indicated' to 'measured' and then to the mineral reserves category, from which a highly reliable estimate of the economic feasibility of the project can ultimately be derived, technical times are also required to obtain all necessary regulatory approvals for the operation of the deposit.

It is therefore difficult today to even roughly estimate when Whistler will be able to begin metal production. However, it could take several years, even seven years, for mining projects to receive approval in the United States, according to information from Italian industry experts recently disclosed by Minister of Enterprise and Made in Italy Adolfo Urso, according to this article on Unionesarda.it. This average estimate for mineral projects in the US is reliable, as the aim of the experts now is a strategic assessment of the national mineral maps and a comparison with other countries, in particular with regard to the time required to obtain permission from the authorities to start mining.

However, U.S. GoldMining Inc. shares, along with other gold stocks in the mining industry, already offer a solution to gain exposure and profit from the changes in the price of gold.

The Stock Valuation

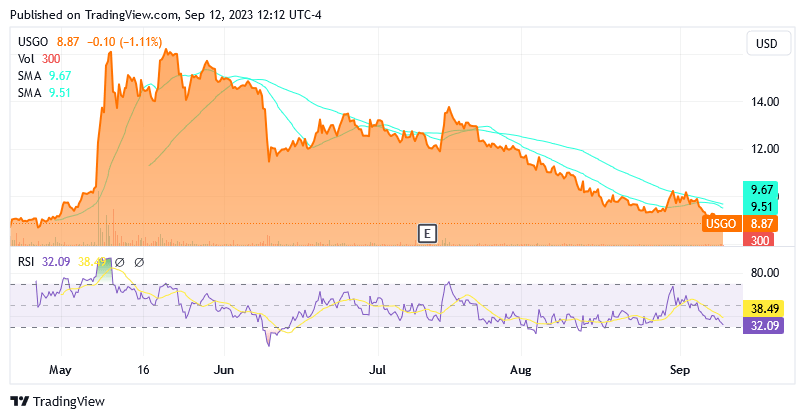

Shares of U.S. GoldMining were trading at $8.87 apiece as of this writing, giving it a market cap of $111.54 million.

Source: Seeking Alpha

Shares have declined significantly since July, trading below the 75-day simple moving average of $9.67 and below the 25-day simple moving average of $9.51.

In light of the strong upside potential, fueled by expectations of a rally in the gold price in response to the likely recession, as this stock is poised to benefit from its strong positive correlation with the commodity price, the shares may currently offer a very attractive entry point.

Additionally, the 14-day relative strength indicator of 32.09 suggests that the stock price is very close to the oversold level. The chances of the share price falling from current levels are not really a lot, but there is still a likelihood that shares will continue to face negative pressure from the Fed's intention to keep monetary policy tight in the coming months.

A high-yield environment is not good for gold because it increases the cost of holding an investment that tracks the metal rather than bonds.

However, it may take several weeks for gold prices to shed their bearish sentiment and turn bullish amid recession fears, so investors may want to wait and keep the stock on Hold for now.

The risk of investing in U.S. GoldMining is that the stock doesn't take the trend as above projected. This risk is mitigated by the following factor: based on the relationship that links the performance of this company's stock price to the development of the gold price, U.S. GoldMining has at least the same upside potential that many other gold mining companies have already exploited over their longer trading histories.

But the risk is exacerbated by the following factor: The stock's float of 2.32 million common shares is small compared to the total 12.39 million shares outstanding. In addition, trading volumes are very low: according to Yahoo Finance, an average of 19,000 shares were traded in the last three trading months, and an average of 8,440 shares were traded in the last 10 trading days. The retail investor must be very careful not to overload the position. Otherwise, it will be difficult to sell shares quickly, when necessary, which poses the risk of loss.

Conclusion

U.S. GoldMining Inc. is an exploration company that owns a mineral project for the future production of ounces of gold equivalent in Alaska.

The stock is relatively new to the US gold stocks sector. Following a spin-off from GoldMining Inc., the parent company and now majority shareholder, USGO shares have been available for trading on Nasdaq-CM since the IPO in April 2023.

The company is currently funding future exploration activities and mine studies that will lay the foundation for upgrading Indicated Resources to Measured Resources. There are currently no estimates regarding the economic feasibility of the project. It could be years before the Alaska project begins mining the metal.

However, the stock offers the opportunity to benefit from the gold price cycle as it has a strong positive correlation with the metal.

Gold may soon experience a strong recovery in response to the expected recession as the metal probably won't be able to miss the opportunity to act as a safe haven asset amid the related headwinds.

Shares are currently trading low, so they already offer the potential to deliver a significant return if the stock price rises alongside a recovery in the gold price.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.