Arm IPO: How The Failed Nvidia Takeover Affects The Upcoming Offering

Ingenious Buddy

One of the world's most influential—and arguably most understated—technology companies is set to go public in September 2023.

The company in question is known as ARM Limited (NASDAQ:ARM), and is based in the United Kingdom.

This development is big news not only because it's set to supercharge the market for initial public offerings (IPO), but also because ARM's story is so closely intertwined with that of Nvidia (NVDA)—a company that's seen its fortunes soar to record heights in 2023.

ARM is somewhat unique in the tech world because instead of manufacturing advanced processors, the company designs them, and then licenses its intellectual property to other companies in the industry.

In essence, customers of the British chipmaker use ARM-designed blueprints as the foundation for their processors, while layering on top their own custom circuitry. As such, ARM revenues are driven by royalties and licensing fees.

Notably, ARM is wholly-owned by the Japanese conglomerate SoftBank Group (OTCPK:SFTBY), which will continue to control the majority of ARM even after the forthcoming IPO. Once the IPO is completed, SoftBank will control 90% of the shares in ARM.

Bloomberg

At present, most financial media outlets are quoting a valuation range between $50-$55 billion for the ARM offering, implying a stock price somewhere between $47 and $51/share. ARM is expected to debut on the Nasdaq exchange during the week of September 11—likely on September 14.

As most investors and traders are aware, Nvidia bid $40 billion to try and acquire ARM back in 2020, and then spent two years trying to convince global regulators that the move wasn't anti-competitive. Unfortunately for Nvidia, those efforts ultimately failed, and the takeover attempt was officially abandoned in early 2022.

Considering that context, it's easy to see why investors and traders might yearn to own a piece of ARM. After all, Nvidia's has transformed into one of the world's most innovative technology companies, and has been pushing the envelope in the field of artificial intelligence (AI).

Leaders at Nvidia apparently saw significant potential in ARM, otherwise they wouldn't have moved to try and acquire it. Accordingly, one could see how investors and traders might also see ARM as a good fit for their portfolios.

On the other hand, one could argue that ARM's value as a part of Nvidia exceeds its potential as a standalone company. And that ties back not only to ARM's unique position in the industry, but also the synergies that Nvidia was seeking to unlock through its failed acquisition bid.

Moreover, if Nvidia can't acquire ARM, that probably means nobody can, which removes some of the buyout buoyancy that a company like ARM would usually enjoy.

ARM's Potential is Arguably Diminished After the Failed Nvidia Takeover

Leaders at Nvidia never outlined their specific plans for ARM once the acquisition was complete, but some experts have hypothesized that Nvidia was interested in ARM's advanced central processing unit (CPU) designs, its wide footprint in mobile devices, and the advanced networking capabilities inherent in ARM-designed products.

Nvidia itself started out as a specialist in graphics processing units (GPUs), but steadily graduated to become a GPU systems company, and eventually a datacenter computing company.

That's according to the words of the company's co-founder and CEO, Jensen Huang, who said “We were a GPU company and then we became a GPU systems company. We became a computing company which started from the chip up, now we are extending ourselves into a datacenter computing company.”

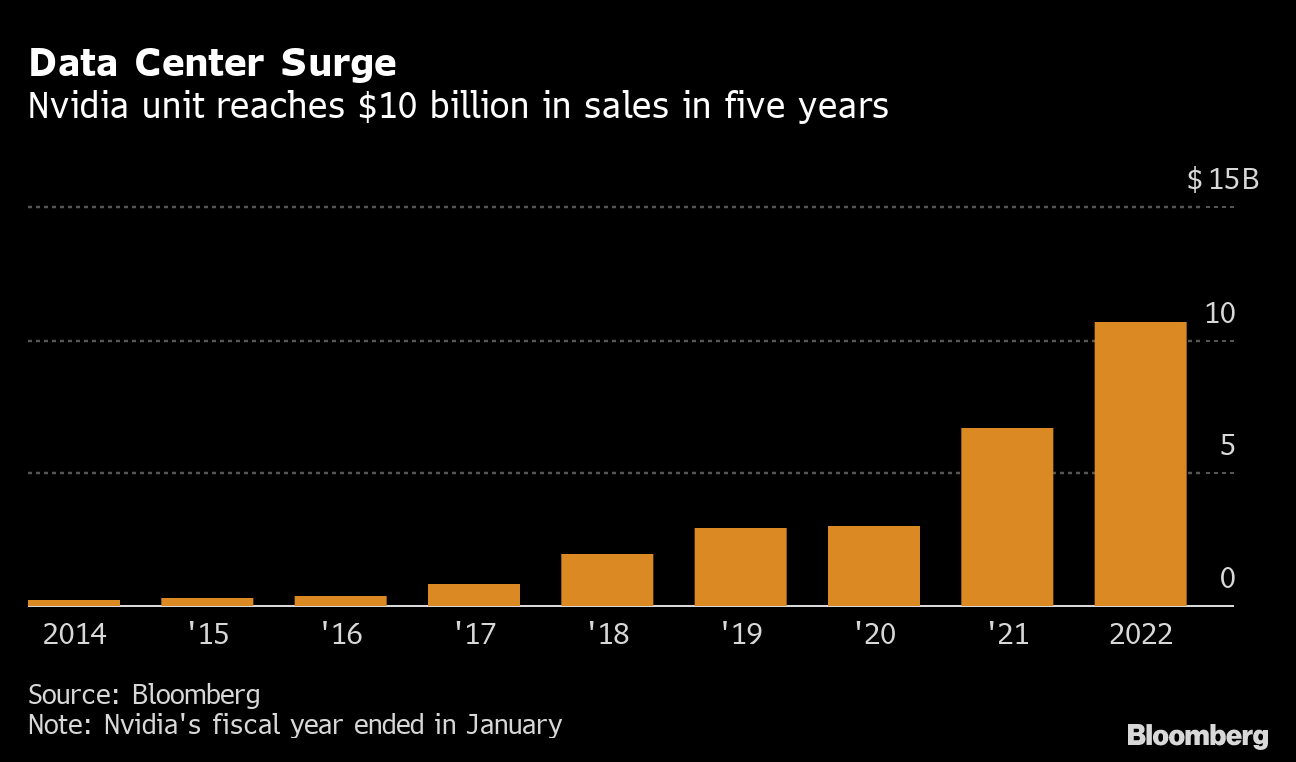

And as most investors and traders have observed, growth in Nvidia’s data center division is one of the key reasons the stock has skyrocketed this year. In its last two earnings reports, Nvidia has posted significant upside surprises for its projected revenues from its data center unit.

Bloomberg

Nvidia has been making inroads with data center customers because their GPUs are so well-suited for training generative AI models, which require the rapid processing of extremely deep data sets.

Traditionally, data centers have been primarily powered by CPUs, not GPUs. But with the emergence of advanced AI, GPU's like those offered by Nvidia will be a key building block in next generation data centers.

However, that doesn't mean CPUs are going to become obsolete. In fact, some experts see a future in which the pairing of CPUs and GPUs could unlock even greater efficiencies.

These technologies are represented by hybrid CPU/GPU chips, as well as so-called “systems on a chip (Soc)—the latter is basically an entire computer on a chip, including a CPU, GPU, memory, input/output controllers and potentially a lot more.

Nvidia is already at the forefront of GPU design and development, which will clearly be a key competitive differentiator in the coming years. But on the other end of the spectrum, one can see how Nvidia could suffer without an equally advanced CPU under its own roof.

Circling back to ARM, it probably won't come as much of a surprise to hear that the company designs some of the most advanced CPUs in existence, which is why ARM boasts heavyweight clients such as Apple (AAPL), Intel (INTC), Samsung, and even Nvidia itself.

Had Nvidia successfully acquired ARM, then it would have held one of the most important chips (literally and figuratively) in the race toward a comprehensive system on a chip, which would have featured Nvidia's advanced GPU capabilities, along with ARM's superior CPU design capabilities.

The incredible potential of the combined Nvidia-ARM enterprise really hits home when one considers that Nvidia's newest GH 200 Grace Hopper Superchip comes equipped with an ARM CPU—the 72 Core Arm Neoverse V2.

AS such, one can see quite easily how Nvidia would have benefited from having the full resources of ARM's enterprise intelligence focused on improving Nvidia’s competitive advantage, as opposed to the current paradigm, in which ARM is producing advanced chip designs for a wide swath of the industry.

Assuming that the system on a chip (SoC) wins out as the best possible technology for future data centers, that would have put Nvidia much further ahead of its competition. And now that the marriage between Nvidia and ARM is off the table, it’s easy to see how Nvidia’s position in the market is slightly less dominant.

As a customer of ARM, Nvidia does have access to advanced CPU designs, and can incorporate them into its products, as it has done with the GH200. But in this reality, companies like Intel (INTC) and Advanced Micro Devices (AMD) also have a fighting chance to produce superior CPU/GPU hybrids, or system on a chip, offerings.

Intel and Advanced Micro Devices currently dominate when it comes to CPUs in data centers, and both are working on developing cutting-edge GPUs. Between the two, AMD is arguably a step ahead with its new MI300X chip.

Additional Considerations Related to the ARM IPO

Looking beyond ARM’s CPU superiority, it should be noted that ARM’s processor designs are also ubiquitous in mobile devices. According to numerous sources, 99% of the smartphones in existence are equipped with ARM-designed technology.

Considering Nvidia’s limited presence in the mobile world, one can see how Nvidia might have quickly expanded its footprint into a completely new business segment (i.e. mobile) had it successfully acquired ARM.

GPUs like Nvidia’s do already exist in the mobile arena, as evidenced by Apple’s M1 chip, which also relies on ARM technology. That suggests that with the help of ARM, Nvidia could have expanded quite easily into the mobile arena.

Considering all of this background, it's a lot easier to see why many in the industry were so strongly opposed to the Nvidia-ARM combination. It's also easy to see how ARM’s future potential isn’t as rosy as a standalone company.

That may be why one analyst at Bernstein—Sara Russo —values ARM at only $46 billion, which is well below the target valuation of $50-55 billion that the company is targeting in its IPO. And even further below the implied $64 billion valuation that SoftBank recently paid internally to transfer 25% of its stake in ARM from one of its funds (the Vision Fund) back to the parent company.

On the plus side, the forthcoming IPO will provide ARM with a good amount of fresh capital—ARM will collect an estimated $5-7 billion from the IPO. Moreover, leaders at the company should be better positioned to focus on the company’s growth strategy, as opposed to dealing with the latest takeover rumors.

Some have even speculated that ARM could try and expand beyond a design-only company, and attempt to manufacture its own line of chips. But such a venture wouldn’t be easy, nor cheap. And with SoftBank ultimately at the helm, it’s hard to envision the company embracing such a high-risk endeavor.

Either way, ARM maintains a dominant position in a critical global industry, and there’s no reason to think that a bright future doesn’t lie ahead. It’s just not as bright as it could have been as a part of Nvidia. Especially with ARM’s takeout potential now theoretically off the table.

For these reasons, potential ARM investors may want to tread carefully on the company’s first day of trading (likely Sept. 14). If shares in ARM dip below the targeted valuation range ($50-$55 billion), that may represent an attractive entry point for market participants that are bullish on ARM, or the broader chip industry.

On the other hand, if ARM’s valuation exceeds the target valuation range on the first day of trading, that could be a sign to steer clear of this offering, and wait for a more advantageous entry point. With a valuation of $55 billion or more, the risk-reward dynamics of a long stock position just aren’t as attractive, especially with the tech-heavy Nasdaq 100 already up 40% this year.

This article is courtesy of Luckbox magazine.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.