Kroger Is A Buy, But I Don't Like The Merger

Summary

- Kroger reported mediocre second quarter results, but reaffirmed its full year guidance for fiscal 2023.

- In October 2022, Kroger announced its intent to merge with Albertsons but the deal will probably be challenged by the FTC.

- And due to the rather high debt levels for the business, I am also skeptical about the deal.

- Kroger by itself is undervalued and trading at a strong support level.

amgun

Since I have published my last article about The Kroger Co. (NYSE:KR) almost 16 months have passed, and as a lot has happen it seems to be time for another update. But while there is a lot to report from a fundamental point of view, the stock price has not moved much. And what is even worse – the stock price declined about 7.5% during that timeframe while the S&P 500 (SPY) increased about 14.26% and would have been the much better investment.

Nevertheless, I remain bullish about Kroger and stand by the title of my last article that Kroger is a good investment. In this article I will explain again, why I think that Kroger is a good long-term investment and why I don’t like the merger.

Quarterly Results

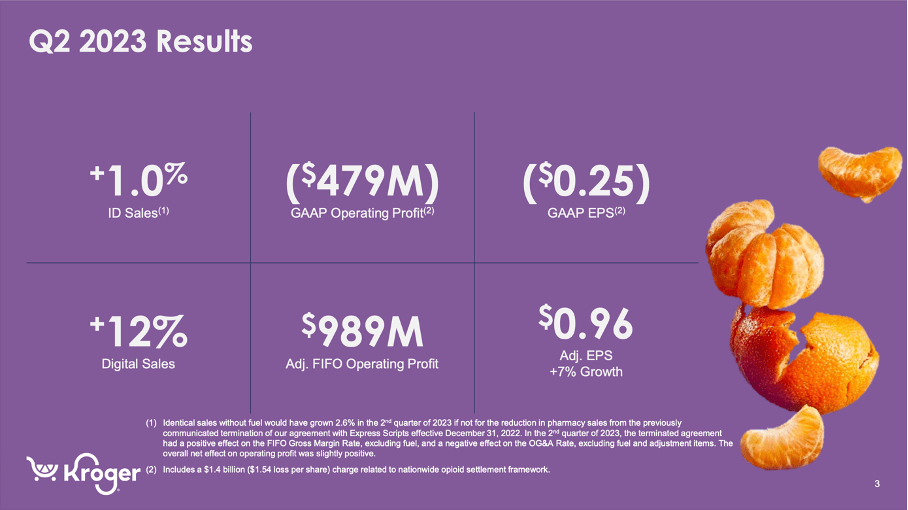

And we can start by looking at the quarterly results reported in September although these are no reason to be bullish. For starters, net sales declined from $34,658 million in Q2/22 to only $33,853 million in Q2/23 resulting in 2.3% YoY decline. And instead of an operating income of $954 million in Q2/22, Kroger had to report an operating loss of $479 million this quarter. When looking at the bottom line, the picture is similar: Instead of diluted net earnings per share of $1.00 in Q2/22, the company had to report a loss per share of $0.25 in Q2/23.

Kroger Q2/23 Presentation

When looking at the adjusted numbers, the picture is getting a bit better. When excluding fuel, sales increased 1.0% year-over-year from $29,238 million in Q2/22 to $29,534 million in Q2/23. This was mostly due to the lower fuel prices ($3.65 per gallon instead of $4.62 in the same quarter last year). And adjusted earnings per share increased from $0.90 to $0.96 – resulting in 6.7% year-over-year growth. And finally, Kroger reported $578 million in free cash flow. Compared to $640 million in free cash flow in the same quarter last year this is a decline of 9.7% but this decline is especially stemming from high capital expenditures.

Guidance 2023

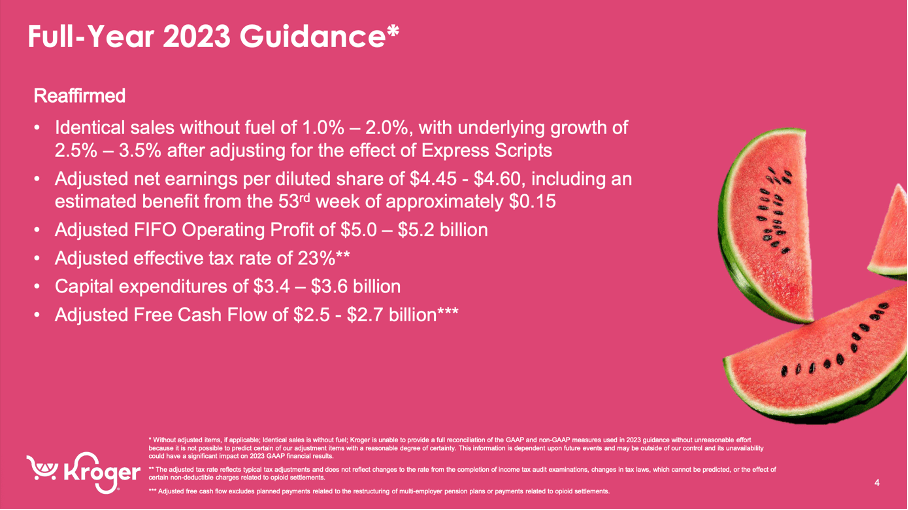

While the results for the second quarter of fiscal 2023 were not great, the company at least re-affirmed its full-year guidance. The company is expecting adjusted net earnings per diluted share to be in a range between $4.45 and $4.60. Compared to adjusted earnings per share of $4.23, this is reflecting a growth rate of 5% to 8.5%. However, we must consider that fiscal 2023 has a 53rd week, which has a positive effect.

Kroger Q2/23 Presentation

Kroger is also expecting adjusted free cash flow for fiscal 2023 to be between $2.5 billion and $2.7 billion with capital expenditures being somewhere between $3.4 billion and $3.6 billion. These are much higher capital expenditures than in the last few years indicating that Kroger is spending a lot right now. And the guidance is also showing that we should not freak out because of one quarter with mediocre numbers.

Kroger-Albertsons Merger

When looking for a reason why the stock rather struggled in the last few quarters, the merger between Kroger and Albertsons Companies, Inc. (ACI) could be a reason. On October 14, 2022, Kroger announced it had entered a definite agreement under which the two companies will merge.

It is not surprising that the Federal Trade Commission is taking a really close look at the merger as the combined business would have about 710k employees, about 5,000 stores, 66 distribution centers and 52 manufacturing plants. Additionally, it would also bring almost 4,000 pharmacies and more than 2,000 fuel centers to the table and would therefore be a dominant player. But Kroger and Albertsons already expected a rather complicated merger as both businesses did not expect the deal to be finalized before 2024.

And as part of getting FTC approval, Kroger and Albertsons will sell about 400 stores as well as 8 distribution centers for $1.9 billion in cash to C&S Wholesalers. Nevertheless, some voices argue that the FTC will challenge the acquisition.

My reasoning is certainly different than FTC Chair Lina Khan’s reservations regarding the deal, but I also don’t like the merger. For starters, I am always a bit cautious when it comes to “mega mergers” as they often don’t work out as planned and are not the best use of cash. And second, the deal would also have an impact on the balance sheet – in a negative way. Regarding financing the deal, Kroger wrote in October 2022:

"Kroger has $17.4 billion of fully committed bridge financing in place from Citi and Wells Fargo. At closing, the Company plans to fund the transaction using a combination of cash on hand and proceeds from new debt financing. Kroger expects to continue to have a solid balance sheet supported by strong free cash flow of the combined business."

It seems like Kroger will have about $27 to $28 billion in debt after the deal closed. According to the latest 10-Q, Kroger has $10,143 million in long-term debt and $545 million in short-term debt. Assuming that shareholder’s equity will stay more or less the same (assets added on the one side – including goodwill – should match the debt added on the liabilities side and the cash subtracted on the asset side), we compare the total debt to $10.6 billion in shareholders equity and get a debt-equity ratio around 2.5 which is rather high.

Additionally, when comparing the total debt to the operating income, it would also take about 3.5 times to 4 times the annual operating income to repay the outstanding debt. Kroger can generate about $4.5 billion to maybe $5 billion in annual operating income and when being optimistic, Albertsons can generate about $2.5 billion in operating income. Of course, these metrics are still acceptable for a business like Kroger – but it is not perfect.

And when looking at the current share price of Albertsons - $21 at the time of writing - the stock market also doesn’t seem to be convinced that the deal is going through. When considering that Kroger will purchase Albertsons for $34.10 per share and subtracting the special cash dividend of $6.85 per share that has already been paid, the stock should trade above $27.

Intrinsic Value Calculation

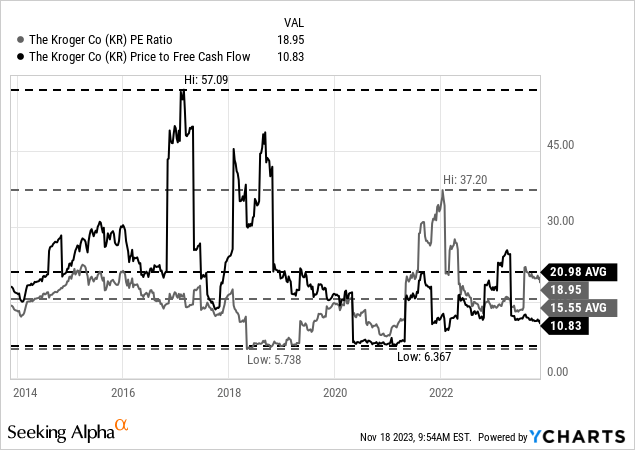

A final step in every analysis is to determine what a fair price for the stock should be – the intrinsic value. And to determine if a stock is rather overvalued or undervalued, we can start by looking at simple valuation metrics like the price-earnings ratio and the price-free cash flow ratio. And while a P/E ratio of 19 might indicate that Kroger is maybe fairly valued or even slightly overvalued, the price-free-cash-flow ratio is speaking a different language. Right now, Kroger is trading for 10.83 times free cash flow, and this is not only one of the cheaper P/FCF ratios of the last ten years – it is also clearly below the 10-year average of 20.98. And for a business that is still able to grow – in my opinion at least in the mid-single digits – a P/FCF ratio of 10 is too low and is implying that the stock is undervalued.

Data by YCharts

Data by YCharts

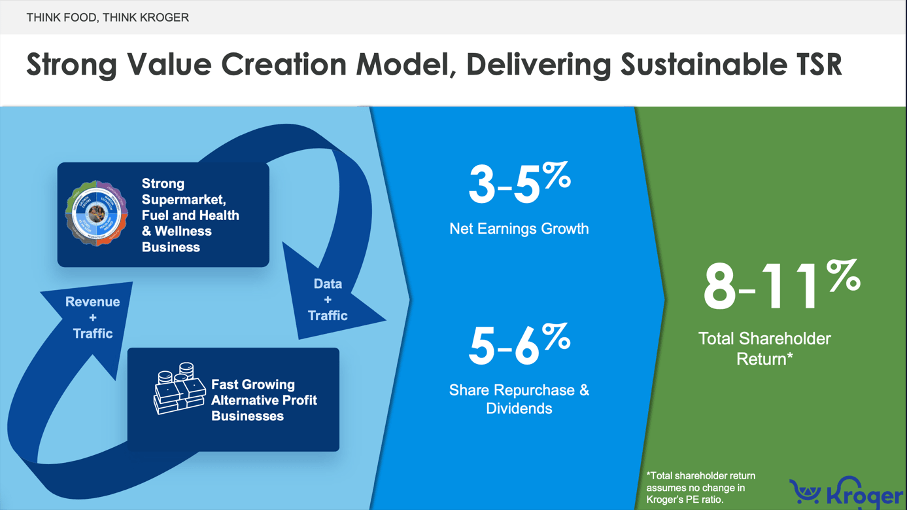

Aside from looking at simple valuation metrics, we can also determine an intrinsic value by using a discount cash flow analysis and for such an analysis we have to make several assumptions. Kroger is hanging on to its long-term targets of 8% to 11% total shareholder return. When looking at these numbers in more detail, we see that Kroger is expecting net earnings to grow between 3% and 5% for the long run. Additionally, Kroger is expecting share repurchases and dividends to contribute about 5% to 6% total shareholder return. However, we must not include dividends in the growth rate and when excluding about 2% to 3% return stemming from the dividend it would lead to about 5% to 9% growth for earnings per share (in my opinion).

Kroger Wells Fargo 6th Annual Consumer Conference Presentation

So, let’s be cautious and assume that Kroger can grow its bottom line only 5% in the years to come. As basis for our calculation, we can take the midpoint of free cash flow for fiscal 2023 ($2.6 billion). Additionally, we calculate with 719 million outstanding shares and, as always, a 10% discount rate. When calculating with these numbers we get an intrinsic value of $72.32 for Kroger and this is implying that the stock is deeply undervalued.

And we can also take a closer look at the growth assumptions to determine if these are realistic. First, let’s look at the long-term growth rates. When looking at the long-term growth rates, Kroger grew its top line at least 4% over the long run – the 10-year CAGR is 4.36% right now. And for earnings per share the CAGR in the last ten years was 8.25%. And when looking at the last 20 years, Kroger grew earnings per share with a CAGR of 7.07% and during the last 40 years the EPS CAGR was 7.47%. Hence, I think we can be confident in assuming a growth rate of 5% for the bottom line.

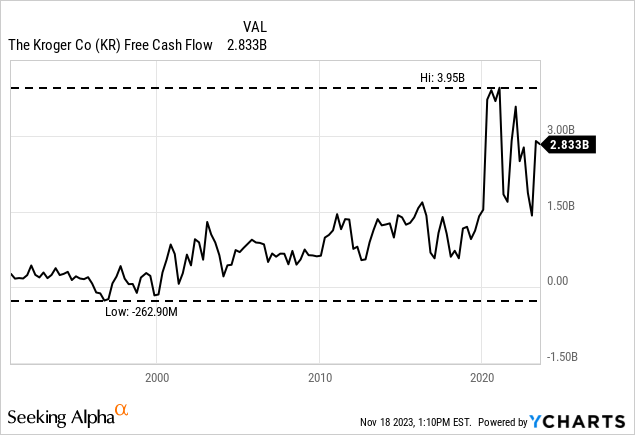

Additionally, we can look at the free cash flow in the past few decades. When looking at the chart we can clearly see that FCF was much higher in the last three years than in the years before. Similar to many other retailers, free cash flow jumped in 2020 with the beginning of the pandemic. But we also have to watch out for the risk of declining FCF again – similar to other retailers.

Data by YCharts

Data by YCharts

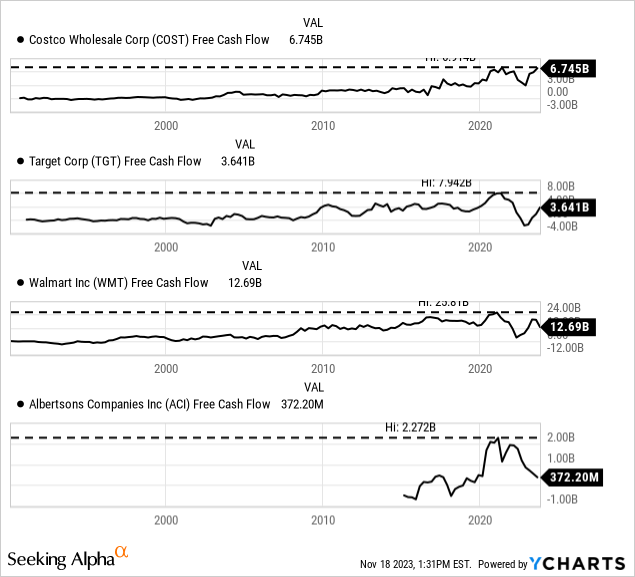

Especially Target is a clear warning sign that the high free cash flow during the pandemic might not be sustainable and free cash flow could collapse back to previous levels again.

Data by YCharts

Data by YCharts

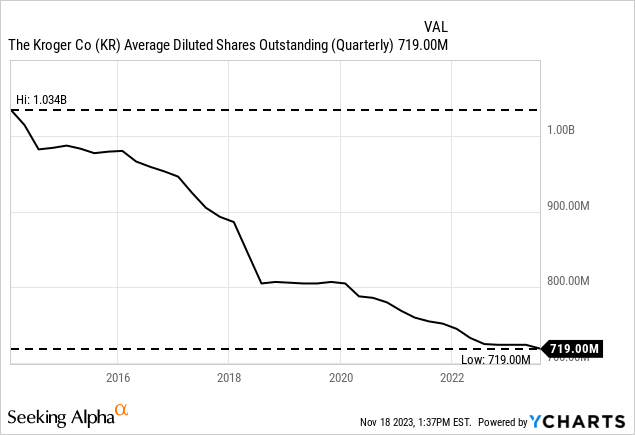

And we can also look at the number of outstanding shares to determine if a high contribution of share buybacks to bottom line growth is realistic. In the last ten years, the company decreased the number of outstanding shares with a CAGR of 3.57% and we can assume about 2-3% growth due to share buybacks. To reach 5% growth in the long run, Kroger has to grow its revenue between 2% and 3%. And growth has to stem from top line growth and share buybacks as margins were rather stable in the past (which is a good sign by the way).

Data by YCharts

Data by YCharts

I think my assumptions are realistic. Only for free cash flow we should be a little cautious. But even when using only $2.0 billion in FCF we still get an intrinsic value of $55.63, and Kroger is still undervalued at this point.

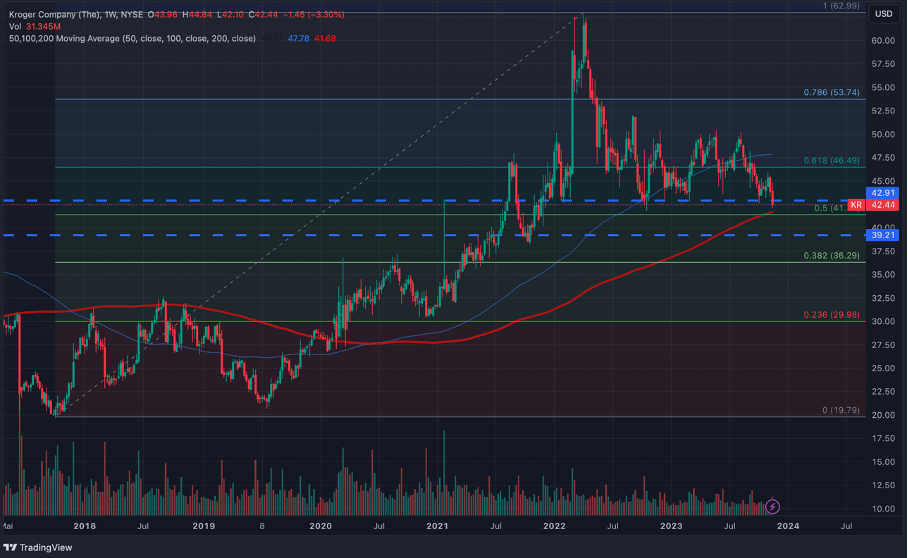

Technical Picture

And when looking for reasons to buy Kroger, we can also look at the chart. It seems like Kroger is at a rather strong support level at this point. And although the stock declined “only” 31% so far, we can be optimistic for the stock turning around and move higher again. At $42 we have several lows of the last two years forming a strong support level. Additionally, the highs of 2015 and the 200-week simple moving average at the same price level are leading to a really strong support level. And finally, we have the 50% Fibonacci retracement of the last upward wave (from 2017 till 2022) around $42 contributing to the strong support level as well.

Kroger Weekly Chart (TradingView)

Combined with the assumption that Kroger is rather undervalued at this level, the chart is telling us that Kroger might go higher.

Economic Moat

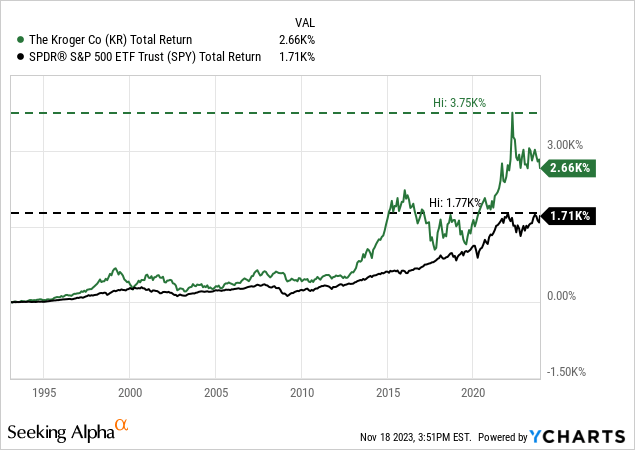

When looking for more reasons why Kroger might be a “Buy” – especially a “Buy” for the long term – we can also mention the economic moat. It is always difficult for retailers to create a (wide) economic moat around a business, but the numbers are indicating the Kroger might have a strong competitive advantage leading to a moat.

For starters, Kroger clearly outperformed the S&P 500 (in this case, I included dividends although the dividend is not playing such a huge role for Kroger). Although the S&P 500 is close to its all-time highs and Kroger declined 30%, the company still outperformed the index: Since the early 1990s, Kroger increased 2,660% in value while the S&P 500 increased 1,710%.

Data by YCharts

Data by YCharts

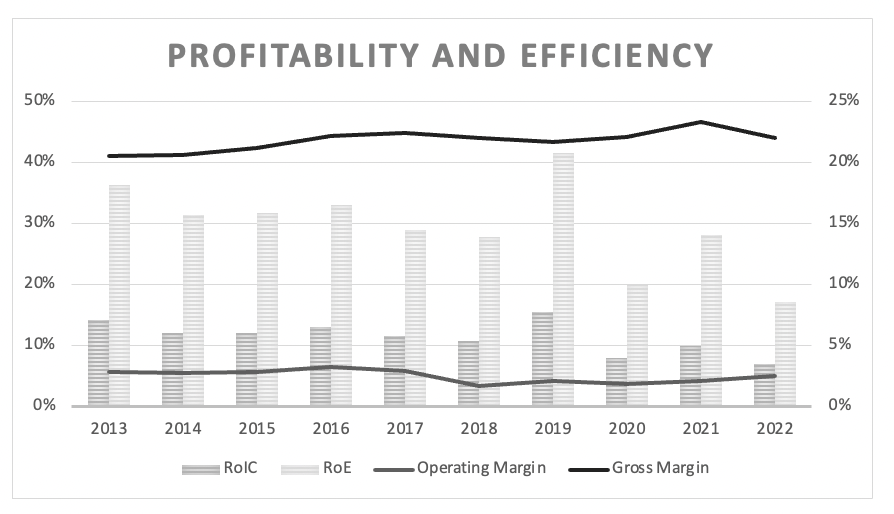

Additionally, Kroger is reporting very stable margins. Similar to many other retailers, margins are low, but we are seeing high levels of stability and consistency – as that is more important than higher margins on an absolute basis.

Kroger RoIC and Margins (Author's work)

Additionally, Kroger reported a return on invested capital of 11.42%. And a return on invested capital above 10% is a strong hint for a wide economic moat as it's one of the most referenced metrics for determining an economic moat.

The moat of Kroger is stemming from cost advantages. Being one of the biggest retailers in the United States enables Kroger to offer cheaper prices than many other competitors as the company can purchase many goods cheaper and also pass on these savings to the consumer. And for some products a few cents can make a huge difference.

Bottom Line

Kroger might be an interesting investment at this point as the stock is trading at a strong technical support level with and most likely below its intrinsic value. And without much doubt, Kroger is one of the better retailers and might have a wide economic moat around the business. However, I am not a big fan of the merger with Albertsons and would rather prefer Kroger as standalone company as such mega mergers lead to high debt levels but often disappoint regarding the performance in the years following the merger.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.