Ulta Beauty's Ugly Day

Summary

- Ulta Beauty, Inc.'s Q2 2024 results disappointed, with revenue and earnings below analyst expectations, leading to a 7% stock drop at one point during the day.

- Despite challenges, Ulta Beauty remains a strong, growing business with no debt, $414 million in cash, and an ongoing $2 billion share buyback program.

- The company's valuation is attractive, and management's confidence in share buybacks highlights the stock's perceived undervaluation, making it a compelling investment opportunity.

- I maintain a “buy” rating for Ulta Beauty, given its robust cash flows, growth prospects, and strategic capital allocation despite recent setbacks.

JHVEPhoto

August 30th was not a particularly pleasant day for shareholders of Ulta Beauty, Inc. (NASDAQ:ULTA), a company that operates as the largest beauty retailer in the US. Through its stores, it sells cosmetics, fragrances, skincare products, and hair care products, and even provides salon services. This is a space that, in prior years, had been quite attractive. Management has achieved robust growth and has not been shy to allocate excess capital toward things like share buybacks.

Unfortunately, though, the stock took a hit, dropping as much as 7% at one point, after having reported, the day prior after the market closed, financial results covering the second quarter of the company's 2024 fiscal year.

According to management, ULTA revenue and earnings came in lower than what analysts anticipated. The pain for the company extended just beyond that quarter, though. Management also was forced to decrease key guidance metrics for the 2024 fiscal year in its entirety. As disappointing as this is, this doesn't change my previous bullish assessment of the company in an article that I published in February 2022. Since then, shares are down roughly 1.7% while the S&P 500 (SP500) is up 23.6%. But when you consider that the company is continuing to expand, and you look at how attractively priced shares are, it's difficult to be anything other than bullish.

A tough quarter

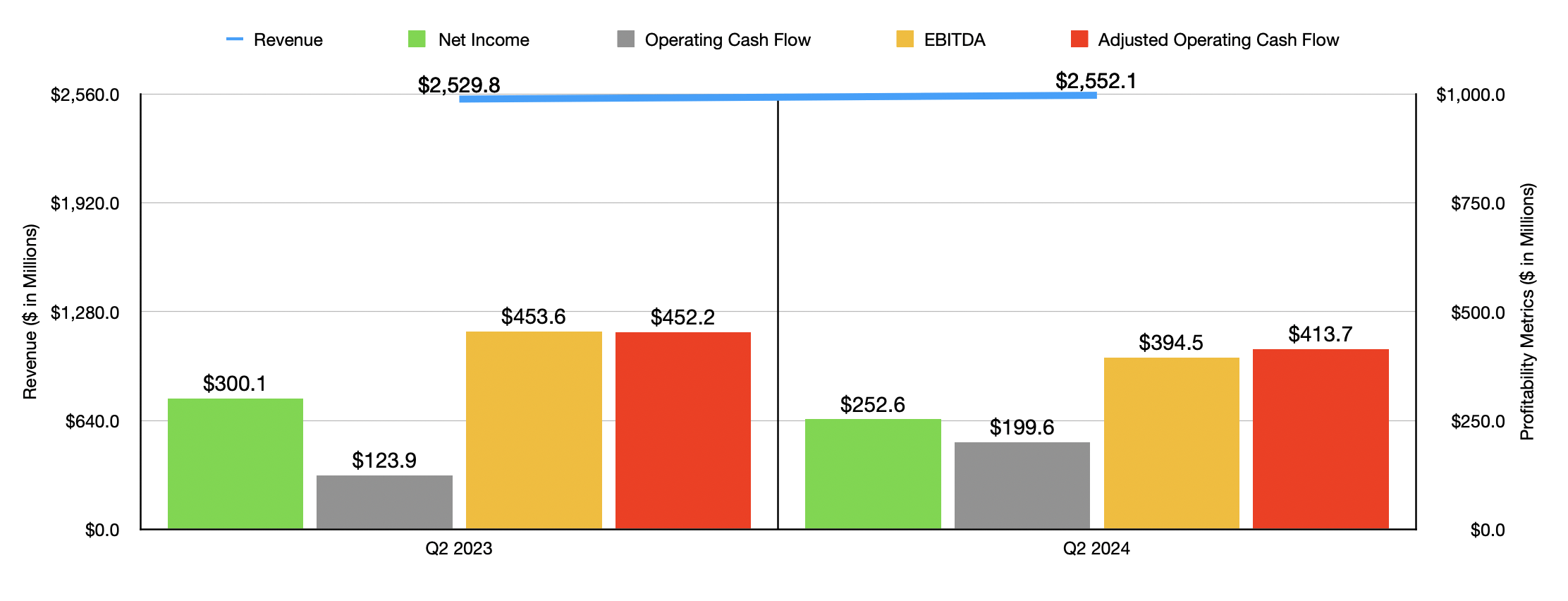

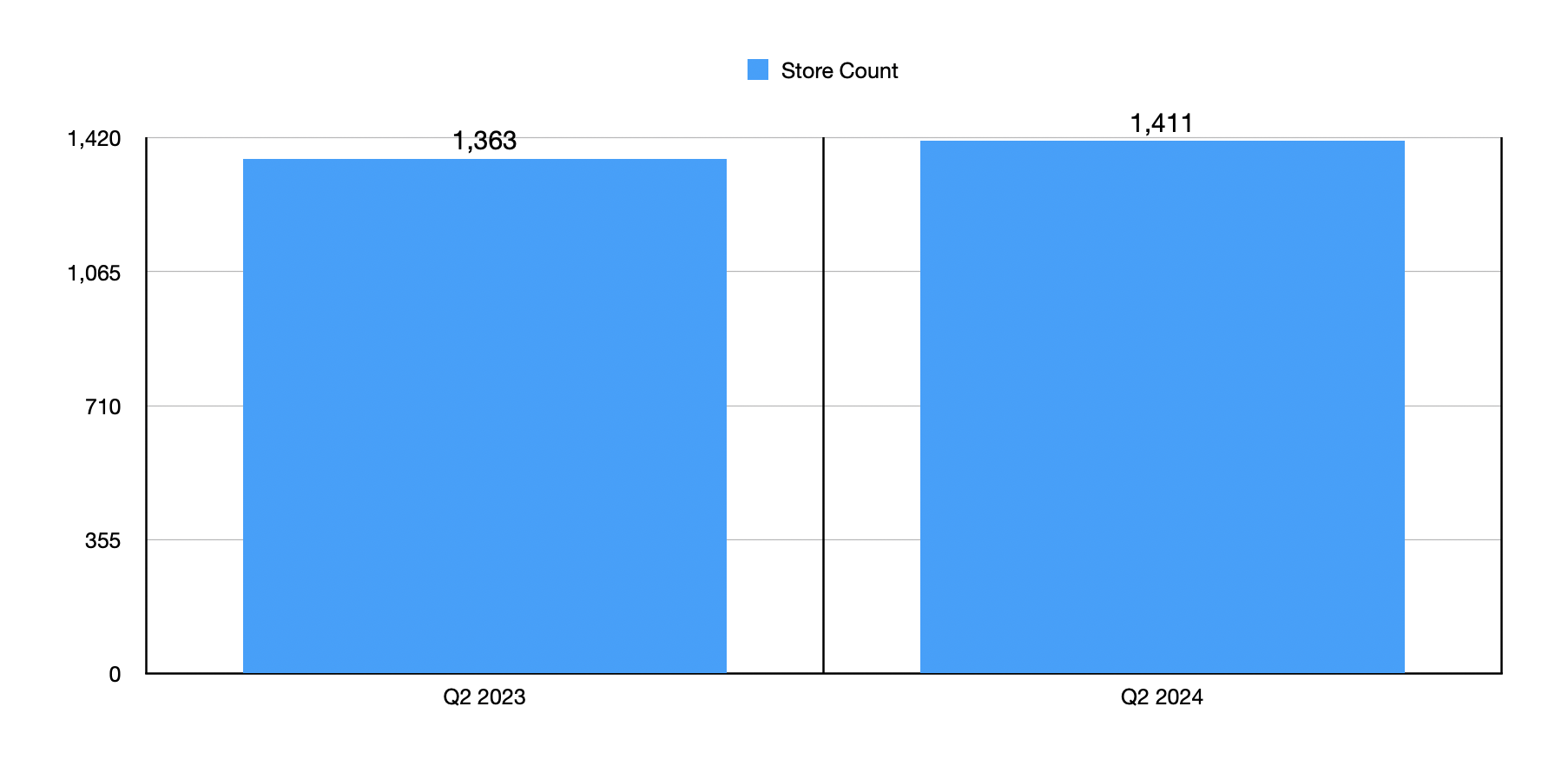

Compared to what analysts were anticipating, the second quarter of the 2024 fiscal year was a disappointing time for Ulta Beauty. Revenue for the quarter came in at $2.55 billion. That is 0.9% above the $2.53 billion the company reported one year earlier. Even though this represented an increase, the sales reported by the company did come in $10 million lower than what analysts anticipated. To be clear, the company did benefit nicely from a rise in store count. At the end of the second quarter of 2023, the firm had 1,362 stores in operation. That number by the end of the most recent quarter was 1,411.

Author - SEC EDGAR Data

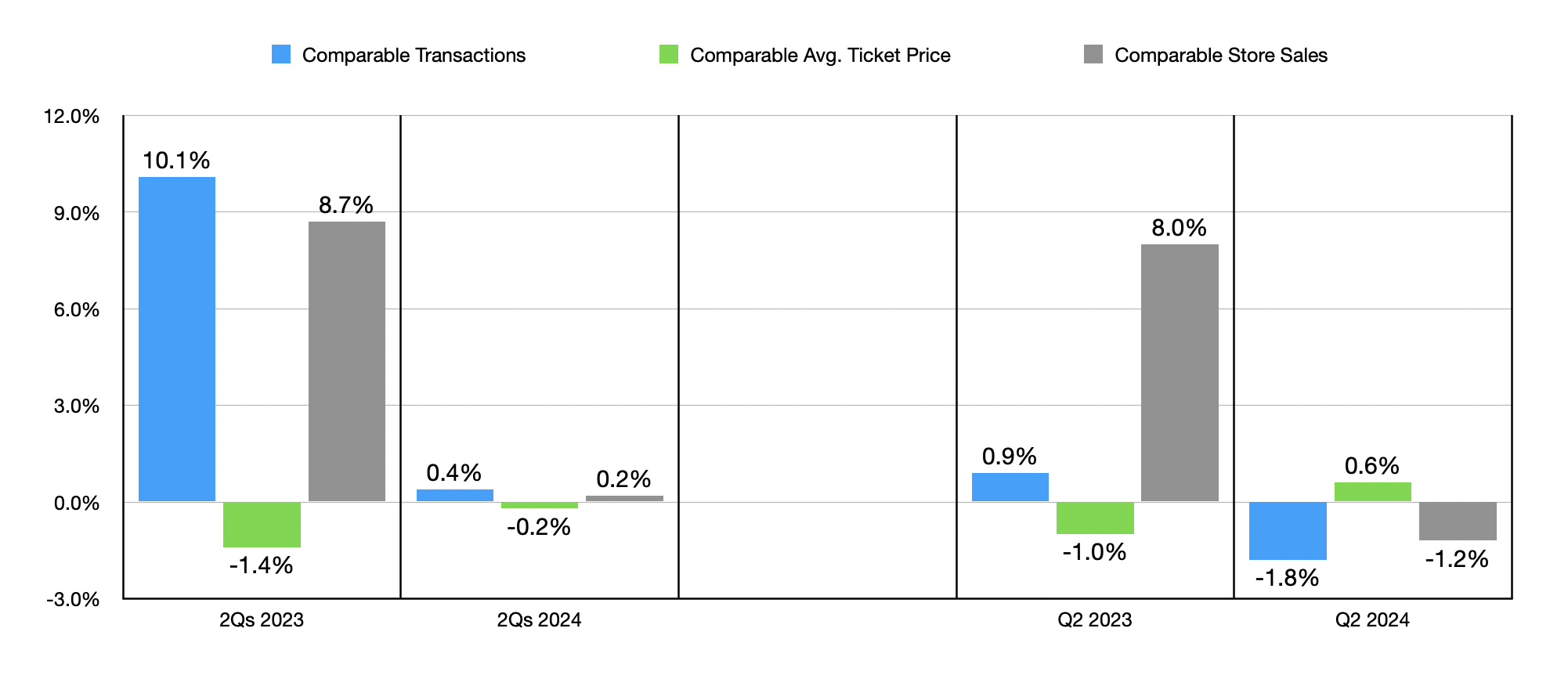

Even though the store count for the company increased, this was offset to some extent by a 1.2% drop in comparable store sales. Digging a bit deeper, we find that the company did benefit from higher average prices paid by customers per transaction of 0.6%. However, the number of transactions on a comparable basis declined by 1.8%. In its investor call regarding quarterly results, the company stated that the rise in ticket prices was because of price increases that the company levied on the customers. However, the drop in transactions was attributable to a few different factors.

Author - SEC EDGAR Data

Management claimed that while the beauty category of products has remained resilient, we are seeing a return to more normal growth following three years of rapid gains. Consumers are responding to higher prices and focusing more on value products. This seems to be at least in large part because of concerns about the economy more broadly. Increased demand in the beauty space is also a problem, as evidenced by the fact that, in just the last three years, over 1,000 new points of distribution have opened, industry-wide, in the markets in which the company operates. This has caused Ulta Beauty to lose some market share. In fact, management said that over 80% of the stores the company has in operation have been impacted by one or more competitive openings recently.

Internally, the company also experienced some issues, largely because of its new ERP platform. Long term, this will likely be worth the investment and the troubles faced. But in the near term, it did cause some disruption. And finally, the company said that incremental promotions did not deliver the sales increases that management had anticipated.

Author - SEC EDGAR Data

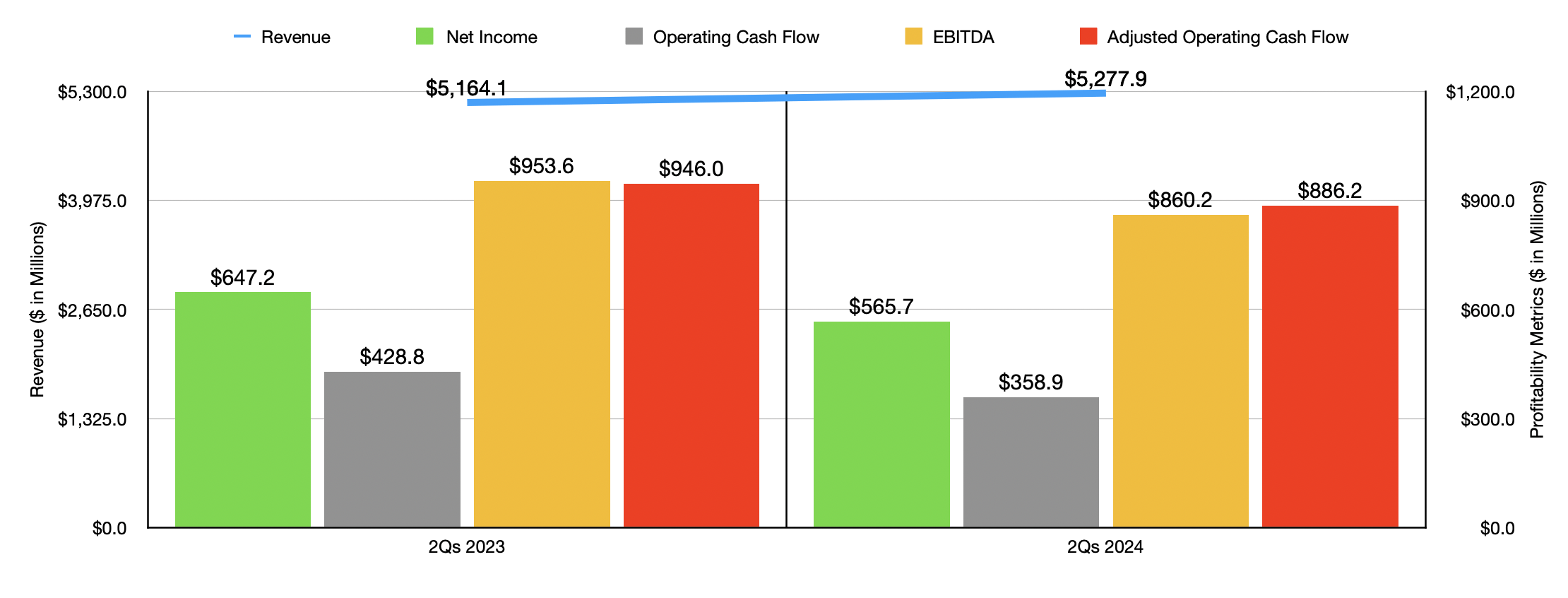

On the bottom line, Ulta Beauty experienced an unfortunate contraction. Earnings per share dropped from $6.02 to $5.30. Total profits per share ended up coming in $0.15 lower than what analysts were hoping for. Even with these problems, net profits still came in at $252.6 million. But that is lower than the $300.1 million the company generated one year earlier. Most other profitability metrics also took a hit. The one exception was operating cash flow, which rose from $123.9 million to $199.6 million. If we adjust for changes in working capital, though, we get a drop from $452.2 million to $413.7 million. Meanwhile, EBITDA for the company declined from $453.6 million to $394.5 million.

Ulta Beauty

These troubles on the bottom line stemmed from margin contraction. The decline in comparable store sales caused a deleveraging of store fixed costs. In addition to this, merchandise margins ended up being lower than anticipated. This brought gross profit as a percent of revenue down from 39.3% last year to 38.3% this year. Selling, general, and administrative costs, also increased year over year, climbing from 23.7% of sales to 25.3%. Delivery of store payroll and benefits costs, as well as higher corporate overhead caused by strategic investments, growing store expenses, and the aforementioned promotional activities, were responsible for this rise.

Author - SEC EDGAR Data

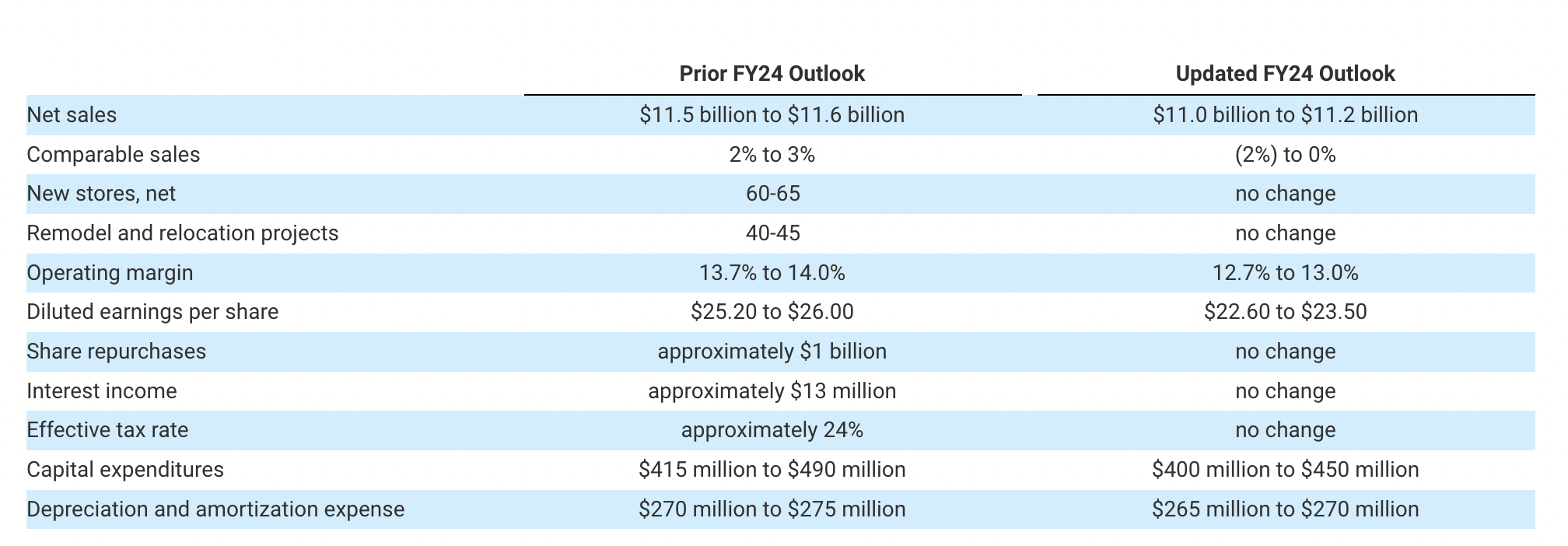

In the chart above, you can see the financial results for the first half of this year compared to the same time last year. As was the case in the second quarter on its own, the company benefited from growing revenue. However, profits and cash flows took a dive. Unfortunately, this trend is likely to continue in the near term. Management said that, as the second quarter neared its end, they saw the picture worsening. This was likely one of the main factors in encouraging management to change certain guidance figures for 2024 as a whole.

Even though the company still intends to open between 60 and 65 net new stores this year while also remodeling or relocating between 40 and 45, they expect overall sales now to come in at between $11 billion and $11.2 billion. This is down from the $11.5 billion to $11.6 billion previously anticipated. The culprit here should be comparable sales that could come in flat at best, but might come in negative by as much as 2%. Prior guidance had called for this metric to grow by between 2% and 3% year over year.

Management has fortunately been able to reduce capital expenditure guidance for this year compared to prior expectations. But seeing as how this is a cash flow item and not a cost item, it doesn't change the fact that the decline in comparable sales and other factors I mentioned already should now result in decreased profits.

Author - SEC EDGAR Data

For the year as a whole, management anticipates earnings per share of between $22.60 and $23.50. This is down from the $25.20 to $26 previously anticipated. At the midpoint, assuming the number of shares outstanding that the company had at the end of the most recent quarter, net profits should come in at about $1.10 billion. Estimates were not provided when it came to some other profitability metrics. But if we annualized the results seen so far for the year, we would expect adjusted operating cash flow of $1.83 billion and EBITDA of $1.73 billion.

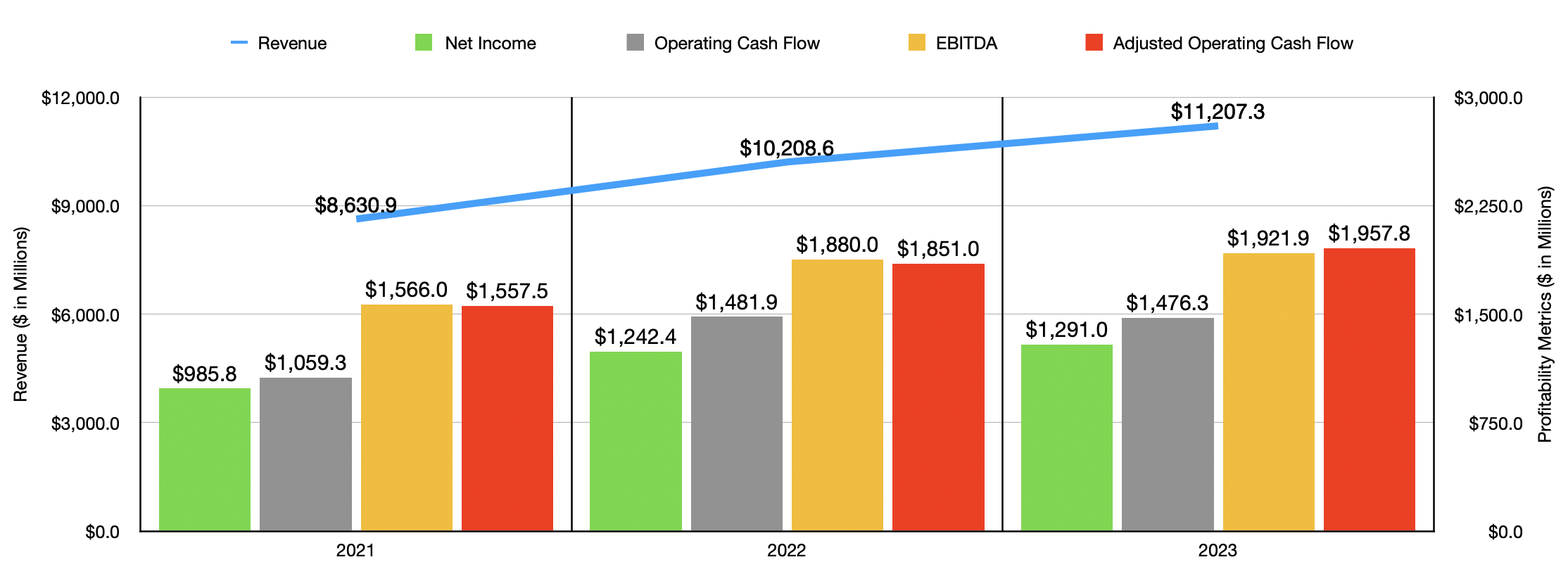

In the chart above, you can see financial results for the last three fiscal years. Clearly, 2024 as a whole will be worse than what 2023 ended up being. But the company is still doing remarkably better than it did in 2021 or 2022.

Author - SEC EDGAR Data

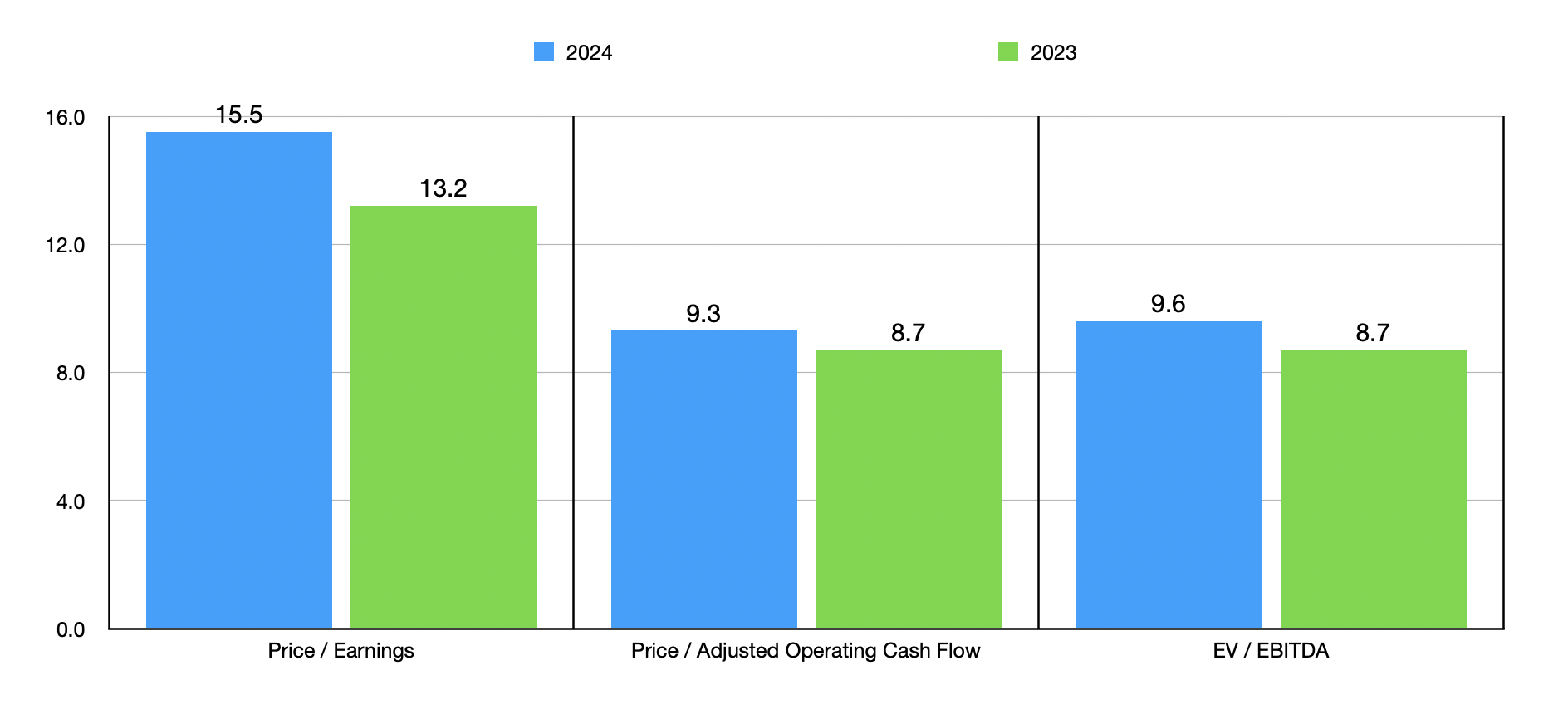

When it comes to valuing the company, in the chart above, you can see how the stock is priced on a forward basis and how it is priced using results from 2023. On a forward basis, shares clearly are more expensive. But considering how the stock is priced compared to cash flows, I would still place the company as a value candidate. There are other reasons for my optimism. For starters, the company has no debt on its books, and it has cash and cash equivalents of $414 million. This provides it a great deal of stability, stability that could come into play if economic conditions result in the economy devolving into a recession.

In addition to this, though, management seems confident that the stock is cheap. Despite the downward guidance in earnings for the year, management is still anticipating spending around $1 billion on share buybacks. In March of this year, management announced a new $2 billion share buyback program. After having completed $497.5 million in the first half of the year to buy back 1.1 million units, Ulta Beauty has around $1.6 billion under this buyback plan that it can still tap into.

Personally, I would prefer the capital be allocated toward additional growth or toward capturing additional synergies. But seeing as how cheap the stock is, I can understand why management is making the decision they are on this front.

Takeaway

It has not been the most pleasant ride for shareholders of Ulta Beauty, Inc. over the past couple of years. However, I do believe that this might represent a good buying opportunity for investors. The fact of the matter is that Ulta Beauty is still a large and healthy business. It's growing and has a net cash position. Shares are attractively priced and management is putting cash flows to work. Add all of this together, and I have no problem keeping the company rated a "buy" for now.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.