As most of the market traders had expected, the Fed released its June meeting minutes at 2 a.m. last night, a departure from the June decision to suspend rate hike It‘s a very hawkish meeting minutes.

His announcement once again consolidated the market's expectation that the Federal Reserve will rate hike twice again in the future. At the same time, it also echoed Powell's hawkish speech after the interest rate meeting in June. Stimulated by the expectation of rising interest rates, the US stocks that rose to a high level began to gradually pull back.

Let's take a look at the details of this meeting minutes.:

This summary is a record of the meeting in June, showing many unknown details. What we need to pay attention to is the following points:

1. There are serious differences within the Federal Reserve on the June resolution. Some officials who agreed to "suspend the rate hike" originally tended to "rate hike", which increased the possibility of further rate hike by the Federal Reserve;

2. The reasons given by rate hike officials are that the momentum of economic activity is stronger than previously expected, and there is almost no sign that the inflation rate is falling towards the target of 2%;

3. Most officials believe that keeping interest rates unchanged at the June meeting will give more time to assess economic progress;

4. Almost all officials said that further rate hike may be appropriate, and most people stressed that communication with the market after the meeting is very important to convey this message;

5. The minutes of this meeting mentioned the economic recession three times, while the minutes of February mentioned it four times, March mentioned it three times and May mentioned it two times. Federal Reserve researchers believe that the probability of avoiding economic recession is basically equal to that of falling into mild recession.

After the minutes of the meeting were released, Williams, the third person of the Federal Reserve and chairman of the New York Federal Reserve, said:It was right to suspend rate hike in June, but it may shrink further in the future. Such a speech has once again consolidated the overall hawkish attitude of the Federal Reserve.

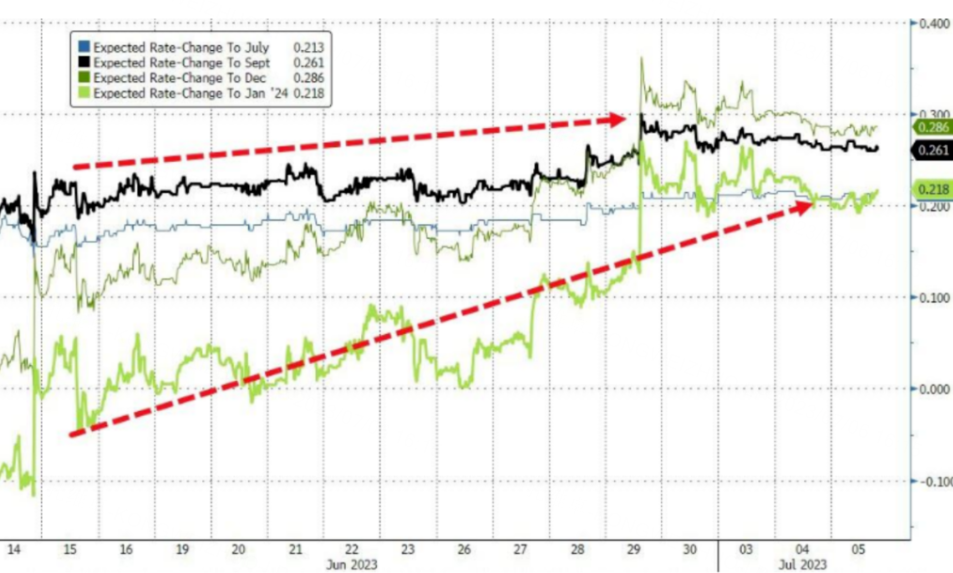

After the release of this purely hawkish summary, the market also priced in the future rate hike higher, and the expectations of the future rate hike in July, September, December and even January next year are all rising simultaneously

So what gives the Fed the confidence to give such obviously hawkish minutes? This may start with the fundamental data of American economy.

Let's briefly review the macroeconomic data of the United States in the past week.

On June 27th, orders for durable goods in the United States increased by 1.7% month-on-month in May, far exceeding the expected value of 1.1%, indicating that the US economy remained resilient and once again increased its bargaining chip for the Federal Reserve's rate hike in July.

From June 28 to 30, the US banking industry passed the stress test of the Federal Reserve, and the performance of consumption and real estate data released in the same period exceeded market expectations, giving the Federal Reserve more reasons for rate hike,

On July 3rd, the ISM manufacturing PMI of the United States recorded 46 in June, which was lower than expected, indicating that the pressure of future economic recession in the United States still exists, but the inflation data released last week is still high, and the number of people claiming unemployment benefits at the beginning of the week released in the latest issue exceeded market expectations, which was lower than the previous value, indicating that the labor market is still tightening.

The overall data gives an image of a resilient American economy,This also means that if the suppression of interest rates is relaxed a little, the rebound of inflation may come more violently.

Let's take a look at the macro data in detail

In June, ISM manufacturing PMI in the United States fell short of expectations, and the pressure on Federal Reserve rate hike eased.

According to the data released on July 1st, the PMI of ISM manufacturing industry in the United States recorded 46 in June, with the previous value of 46.9. It is expected that ISM manufacturing industry in 47 and June fell short of expectations and continued to decline.

The American manufacturing industry shows that the American economy is still facing greater downward pressure. According to PMI breakdown data, the new order index increased month-on-month, but it was still below threshold, the output index and employment index declined significantly month-on-month, the customer inventory and self-owned inventory both declined month-on-month, and the order inventory increased slightly, indicating that the demand for replenishment in the middle and lower reaches of the manufacturing industry was obviously insufficient, and the price continued to decline.

The manufacturing industry showed that the US economy would face greater downward pressure in the future, which eased the rate hike pressure of the Federal Reserve to a certain extent.

The core PCE index of the United States declined slightly, and the policy pressure of the Federal Reserve eased, but the stagflation pressure continued, and the probability of rate hike increased in July.

According to the data released on June 30th, the core PCE price index of the United States increased by 4.6% year-on-year in May, with the previous value of 4.7% and the expected value of 4.7%. According to the breakdown data of PCE index, the year-on-year growth rate of durable goods prices expanded, the year-on-year growth rate of non-durable goods slowed down, and the year-on-year growth rate of services declined.

The overall decline of PCE in May indicated that the inflation pressure of consumers eased and the inflation in the United States was in a downward channel. However, because the inflation level was still far from the target level and the stagflation pressure continued, the Fed still had the possibility of continuing rate hike, and the inflation data exceeding expectations supported the Fed's rate hike in July.

The number of jobless claims in the United States at the beginning of the week exceeded expectations.

According to the data released on June 29th, the number of jobless claims in the United States recorded 239,000 in the week ending June 24th, with the previous value of 265,000 and the expected number of 265,000.

In the United States, the number of initial jobless claims exceeded market expectations and declined from the previous value. Although the downward pressure of the economy was gradually transmitted downward under the background of rate hike, the job market, especially the manufacturing job market, showed signs of slowing down. The decline in the number of initial jobless claims while the demand for service industry remained resilient showed the flexibility of the US job market, eased the employment pressure and supported the Fed policy.

On the whole,

Although the unexpected slowdown of PCE data in May and manufacturing PMI data in June eased the rate hike pressure of the Federal Reserve, Chairman Powell's speech was more hawkish. At the same time, Markit service PMI in the United States remained resilient in June, real estate investment exceeded expectations, and manufacturing industry may gradually stabilize in the second half of the year.

At the same time, under the stagflation environment of controllable employment and high inflation, the Federal Reserve still considered giving priority to reducing inflation before the economy and employment deteriorated in an all-round way, so there is still a great possibility of continuing rate hike in July.

Therefore, under the expectation that interest rates will continue to rise in the future, the short-term yield of US bonds is likely to continue to rise

This will suppress the trend of the US stock index. In the short term, the S&P index of US stocks seems to have shown a weak upward trend, and the double-headed form has become more and more obvious.

However, after the correction, US stocks may continue to rise.Because the strong fundamentals support the future profit expectations of enterprises, the beginning of the second quarterly report has given US stocks more room for speculation. What's more, the long-term upward trend of US stocks has not been destroyed.

Then this pullback may give the holders of short-term short position in the market a good profit opportunity.

Do you agree with me? And at what point do you think the S&P index is most likely to stop its correction?

Let's discuss it. Give me a comment?

$NQ100 Index Main Connection 2309 (NQmain) $Main link of Dow Jones index2309 (YMmain) $$SP500 Index Main Connection 2309 (ESmain) $$Gold Main Link 2308 (GCmain) $$WTI Crude Oil Main Link 2308 (CLmain) $

Comments

Great ariticle, would you like to share it?

[强] [强]