$Wal-Mart(WMT)$ opened high with Q2 Earnings beat, both revenue and profits suprised, but still, closed with 2% plummet.

In terms of store sales

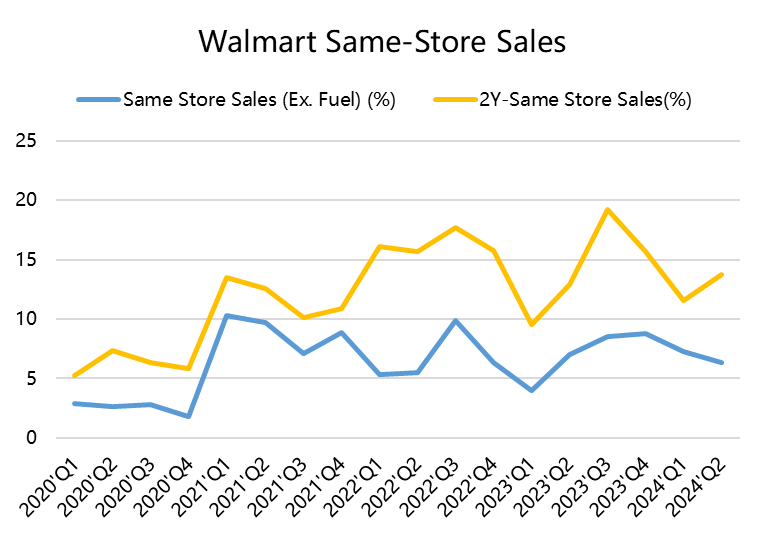

Same-store sales increased by 6.3%, higher than the market's expected 4.04%. Same-store sales in the US rose by 6.4%, exceeding expectations of 4.0%, with transaction volume increasing by 2.9% and average ticket prices rising by 3.4%. Due to the changes in the post-pandemic era, e-commerce's contribution to sales decreased by 230 basis points compared to last year.

Sam's Club's comparable sales increased by 5.5%, slightly lower than the expected 5.59%, with transactions growing by 2.9% and average ticket prices increasing by 3.5%.

In terms of revenue

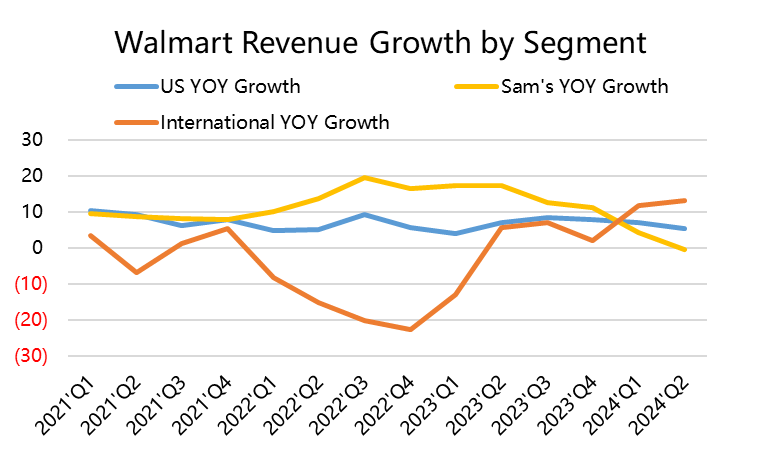

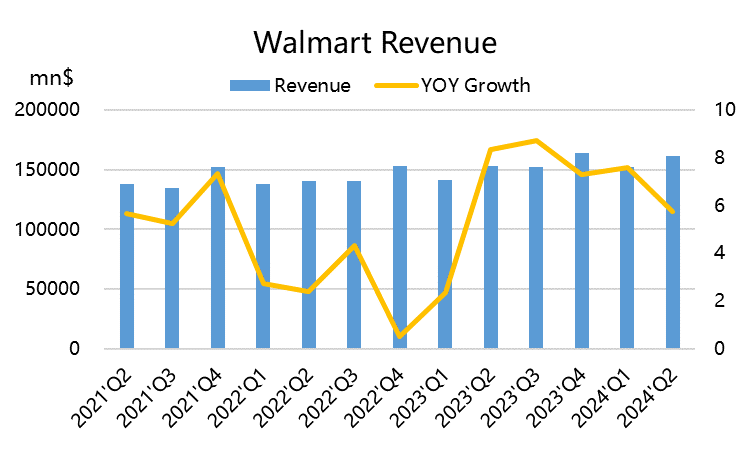

otal revenue reached $161.6 billion, a year-on-year increase of 5.9%, higher than the market's expected $159.7 billion. Walmart's US revenue reached $110.9 billion, a year-on-year increase of 5.44%; Walmart International's total sales increased by 13.3% this quarter, reaching $27.6 billion. Sam's Club's revenue was $21.8 billion, a year-on-year decrease of 0.32%.

Except for Sam's Club falling short of expectations, all other results exceeded expectations.

In terms of profit,

the comprehensive gross profit margin increased by 50 basis points to reach 24.0%, due to better-than-expected discounts and supply chain costs, partially offsetting the continued pressure in the

grocery and healthcare sectors. The ratio of comprehensive operating expenses to net sales increased by 33 basis points.

Pretax profit was $7.3 billion, a year-on-year increase of 6%; earnings per share increased by 4.0% to reach $1.84, exceeding the market's expected $1.71.

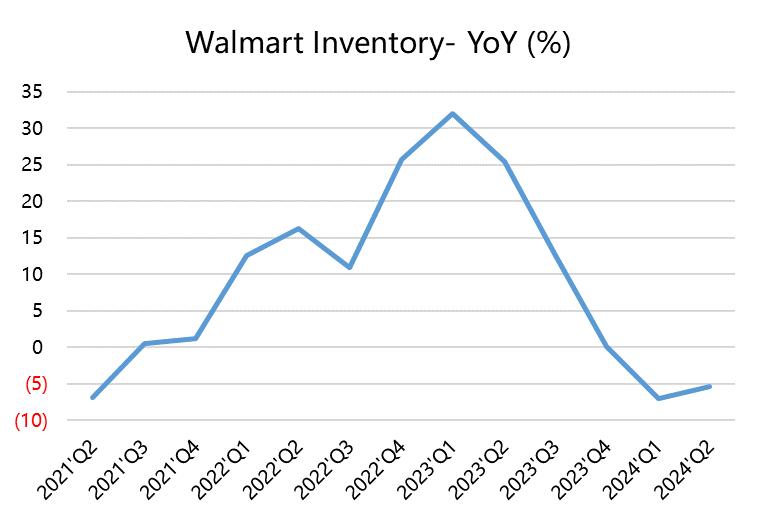

The company believes that food sales still maintain an advantage, and this quarter's performance in general groceries exceeded expectations, with profit growth faster than sales growth. At the same time, inventory conditions are good, and inventory continued to decrease by 5.3% year-on-year this quarter.

As for the Q3 outlook, the company expects revenue to increase by 3% year-on-year, with adjusted EPS of $1.45 to $1.50, which is in line with the market's expected $1.49. Full-year sales are expected to grow by 4% to 4.5%, with adjusted EPS of $6.36 to $6.46, higher than the market's expected $6.27 and the previously guided range of $6.10 to $6.20.

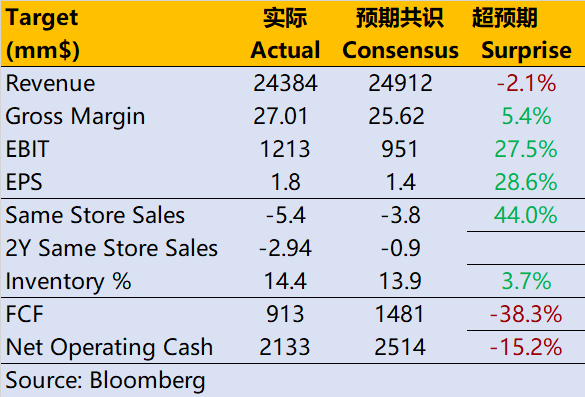

Compared with Target (TGT)

Walmart's performance is much better. $Target(TGT)$ revenue and same-store growth rates were lower than expected, while profit indicators improved significantly.

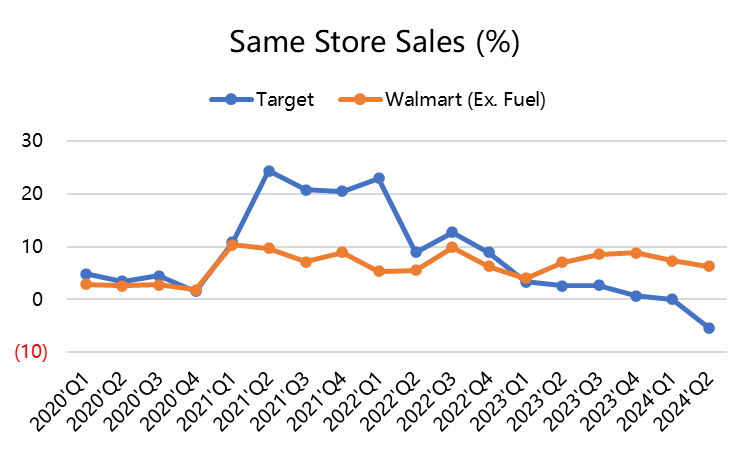

In terms of same-store sales, Target fell this quarter due to sluggish sales, but Walmart still recorded growth, especially in the US where same-store growth was 6.4%.

Therefore, in terms of revenue, Target was the first to fall back. Compared with Target, its elasticity is higher, and it rebounded stronger during the previous recovery.

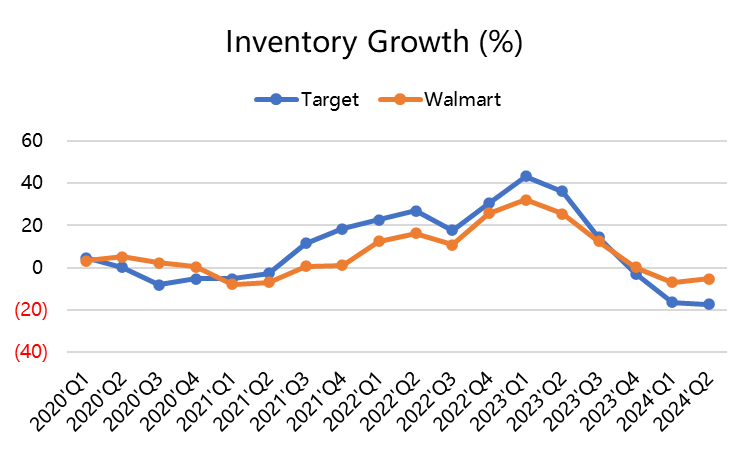

In terms of inventory, both companies' inventories accumulated rapidly in the early stage of inflation, but Walmart's inventory control and logistics cost control were more timely. Since last year, inventory growth rates have started to decline and turned negative two quarters ago.

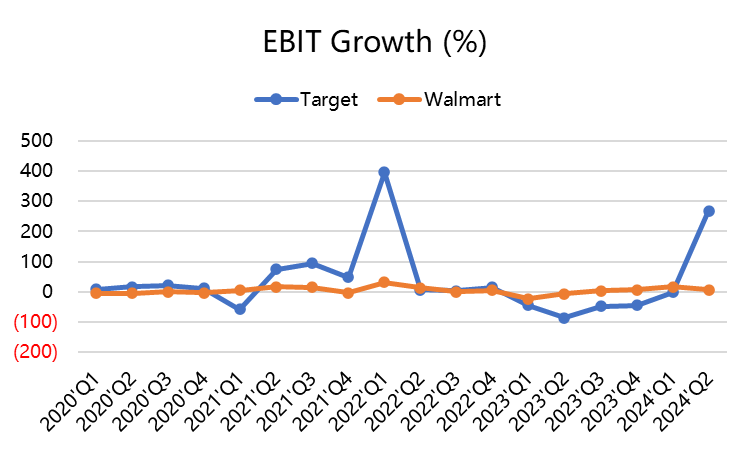

In terms of profit margin, Walmart's pretax profit growth rate is more stable.

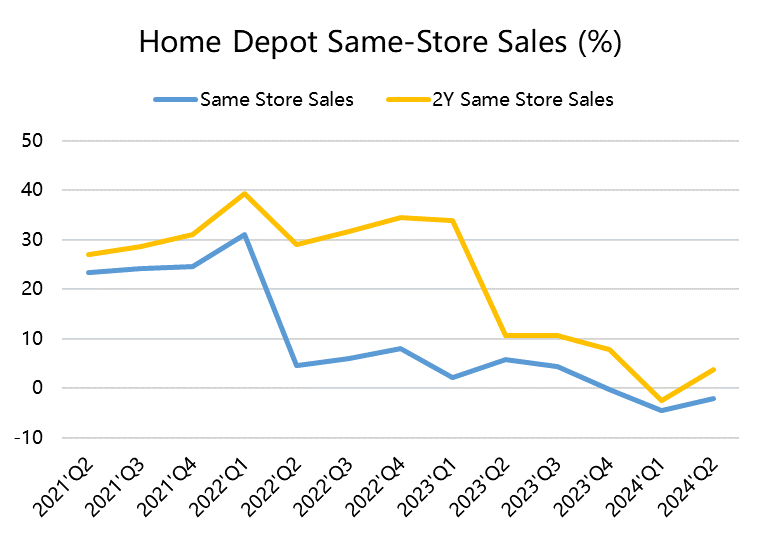

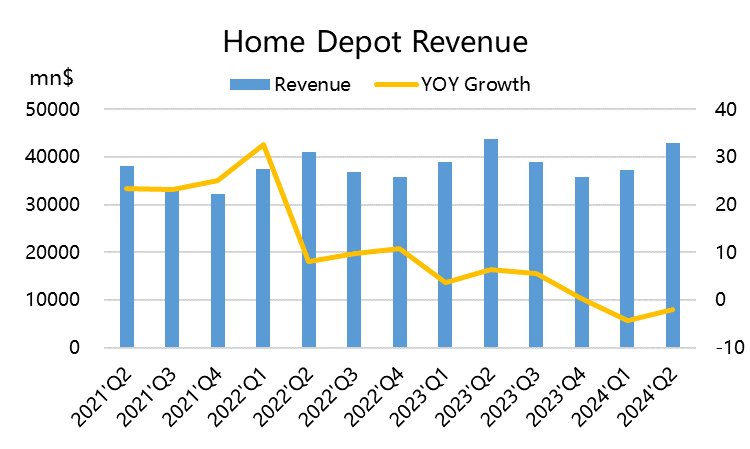

Compared with $Home Depot(HD)$

Home Depot also exceeded expectations in its Q2 financial report before, but same-store sales fell by 2.0%, although it exceeded the market's expected -4.1%, it is still a downward trend for the industry as a whole.

Since Home Depot has more home improvement products, Q2 performance for small items exceeded expectations while high-priced items continued to face pressure.

The company's operating profit fell by 8.6%, net profit fell by 9.9%, and EPS was $4.65, lower than the market's expected $4.45.

Comments

No way is market going to do better than US $1 equal 7.28 yuan and 4 quarters equal one-dollar and there’s four- quarters in a year. Maybe the reason why a football filed has a line ever ten yards and it’s again 100 yards total hence a dollar.

$沃尔玛(WMT)$ after zillion upgrades it only goes up 1.4%. Very weak. May see 150 next week

We’re witnessing the slow decline of Target. Bankrupt within the next ten years IMO. Leadership cares more about fantasies rather than business.

WMT keeping prices low during a long stretch of inflation and cash-strapped consumers noticing the relative price gaps versus Target and traditional grocers.

tape is pretty bearish, has been for hours now, yet the propping is being done quite well! lol