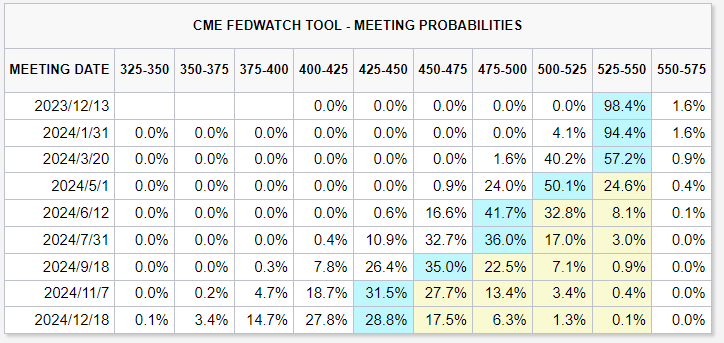

December FOMC meeting is coming, with the last suspenseful suspense of the year being revealed. Rate hikes are definitely over, and the market is just betting on how much longer the Fed's "Higher For Longer" will last.

According to CME interest rate trading, the market is betting on five rate cuts (25bps each time) throughout the year 2024, starting from March.

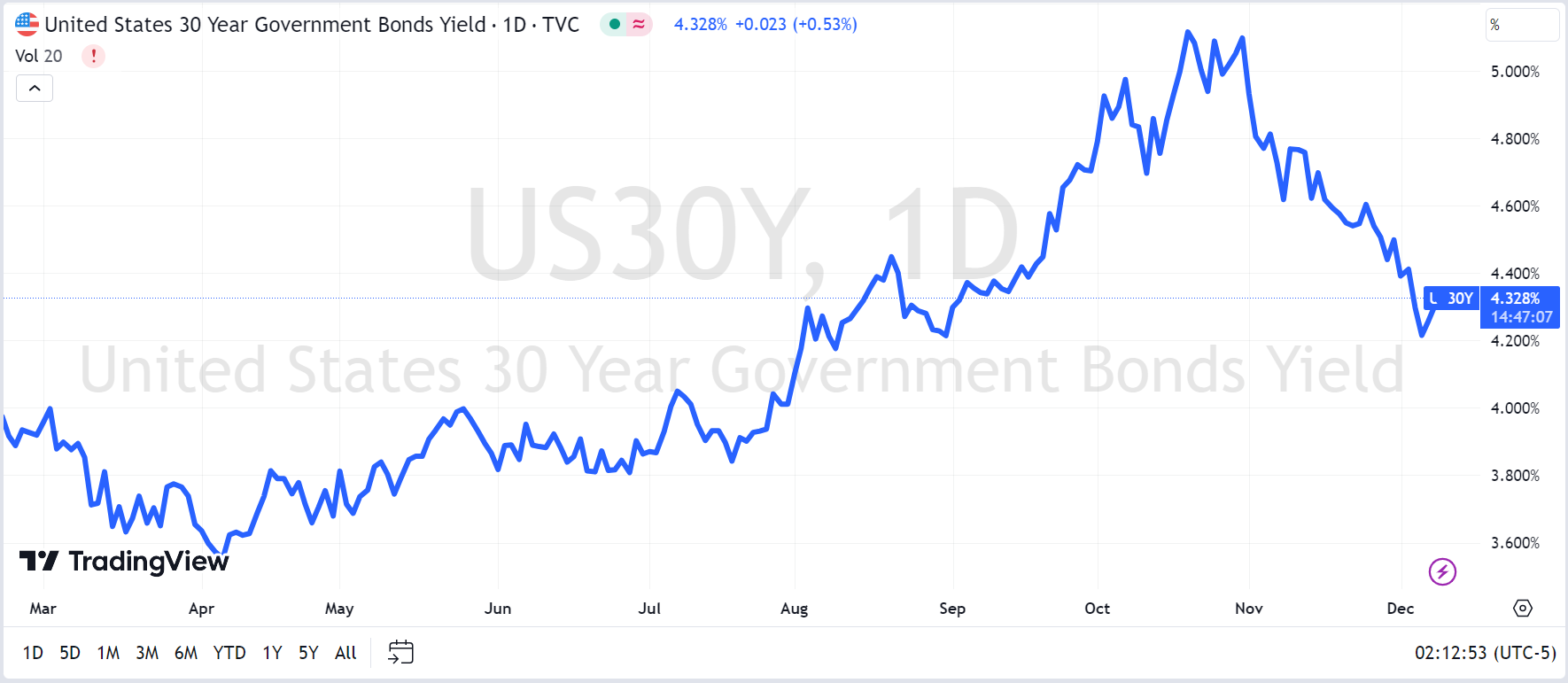

And over the past month, the long-term US Treasury bond yield quickly dropped from 5% to 4.2%, becoming the main driving force behind the performance of assets including US bonds, stock markets, gold, and cryptocurrencies.

So, what might be the stance of the Federal Reserve at the December FOMC meeting?

We anticipate:

1. No further interest rate hikes, maintaining the current level of rates, in line with market expectations.

2. An upward revision of the GDP growth forecast for the end of 2023, and a downward revision of inflation (mainly core PCE expectations).

3. An indication of potential interest rate cuts in 2024, with 2-3 instances on the dot plot, possibly indicating some disagreement.

However, based on Powell's tendency to "balance" his statements, it is possible that he may add some hawkish remarks to the dovish statement, such as: the timing for rate cuts is not yet appropriate, the probability of a soft landing has increased and is moving towards policy expectations, the effects still require patience and more data, and the current market has priced in too many rate cuts, and so on.

In terms of data, the US Q3-Q4 economic data has shown signs of slowing down but still remains resilient.

On one hand, there have been negative slowdowns in consumer sentiment, manufacturing PMI, manufacturing production, and employment. On the other hand, the just-released November non-farm payroll data still exceeded expectations, and the labor market remains robust and healthy.

The rebound in hourly wage growth rate is also worth noting (related to the end of strike negotiations and substantial wage increases).

In addition, the continuous decline in oil prices has put pressure on commodities as a whole, with energy-related prices continuing to slide. Core commodities, hotel prices, airfare, and other prices have been weakened. Therefore, the CPI and core CPI to be released this week may further slow down.

Market expectations are at 3.1%, but the actual figure may be lower.

Therefore, US Treasury yields may experience a trend of falling first and then rising this week.

The decline in long-term US Treasury yields is mainly driven by term premiums and a decrease in real interest rates, and is not closely related to short-term interest rates. Therefore, attention should also be paid to the issuance of new US Treasury bonds at the end of the year.

Comments