Summary

- Nvidia Corporation's stock price has tripled since the advent of generative AI solutions across day-to-day settings.

- And the company's latest earnings results reinforce a strong demand outlook underpinned by its mission-critical role in enabling the continued build-out of accelerated computing supporting AI developments.

- Paired with Nvidia's upcoming stock split, we expect further momentum to its valuation upsurge from current levels.

BING-JHEN HONG

Nvidia Corporation’s (NDVA) stock price has more than tripled since reporting an outsized growth trajectory last year unlocked by relentless AI momentum. The company’s technology continues to serve as the industry’s “gold standard” in facilitating AI developments. This is evident in Nvidia’s continued benefit from a first mover advantage underpinned by its ongoing commitment to being a “market maker” instead of a “share taker.”

Yet, the stock’s valuation multiple has largely remained consistent over the past year. Unlike its AI counterparts, much of Nvidia’s valuation gains realized over the past year have been underpinned by tangible fundamental outperformance. And Nvidia’s latest F1Q25 results continue to corroborate a strong demand outlook for its products, assuaging investors' concerns about the durability of the company's near-term outlook.

This is consistent with the accelerating transition from training to inferencing activities pertaining to generative AI developments, which will further catapult demand. The trend also complements a broader transformation from general purpose to accelerated computing, which Nvidia continues to benefit from as a pioneer.

With its growth outlook still a function of supply availability, Nvidia’s latest earnings update reinforces confidence in the durability of its valuation premium. Paired with the recently approved 10-for-1 stock split that will take effect in June, which typically harbingers a further upsurge, the Nvidia stock remains well-positioned for incremental gains from current levels.

“Nvidia is a Market Maker, Not a Share Taker”

During GTC 2024, Nvidia CEO Jensen Huang summarized the company as a market maker and not a share taker by outlining innovations over the years, counting real-time ray tracing to AI accelerators. This served as a stark reminder that Nvidia remains the critical backbone to not only next-generation innovations, but also economic growth.

And this was evident in the company’s latest earnings results update. The company maintained triple-digit percentage revenue growth in 1Q25, underpinned primarily by relentless demand for its GPUs. Specifically, data center revenue grew 428% y/y to $22.6 billion, driven by 5x expansion in compute demand and 3x expansion in networking demand. Nvidia also disclosed a mid-40% data center revenue mix from sales to hyperscalers, highlighting further headroom for growth as demand for its AI accelerators diversifies into other verticals.

1. Diversifying Demand Environment

The resilient demand outlook for Nvidia’s core data center segment is in line with robust capex allocations toward the build-out of AI infrastructure across its hyperscaler customers, all of which have benefitted from first dibs into the supply constrained environment. Specifically, Nvidia’s mega-cap peers spanning Amazon (AMZN), Microsoft (MSFT), Apple (AAPL), Google (GOOG, GOOGL), and Meta Platforms (META) have earmarked more than $200 billion in spending towards their respective AI strategies this year.

Meanwhile, the company is also starting to diversify its foray into addressing emerging demand across other enterprise verticals, particularly in the automotive segment supporting autonomous mobility developments. Specifically, Nvidia has highlighted Tesla (TSLA) as a key non-hyperscale customer during Q1, as the EV titan leverages 35,000 H100 GPUs in training its latest Full Self-Driving version 12. More importantly, the automotive vertical is expected to become a “multibillion dollar revenue opportunity” for the data center segment, as AI training pertaining to autonomous mobility and smart cockpit solutions continue to ramp.

2. Enhanced Product Pipeline

In addition to a diversifying demand environment, Nvidia’s upcoming shipment of its next-generation GPUs will also further its capture of expanded growth in the multi-year transition from general purpose to accelerated computing. While the H100 continues to be the leading driver of data center revenues, Nvidia expects upcoming shipments of the H200 and next-generation Blackwell chips to increasingly dominant sales through FY 2025.

This is consistent with the Blackwell architecture’s competitive total cost of ownership (“TCO”) advantage and performance gains compared to products based on its predecessor. Specifically, Blackwell enables 4x faster training speeds and 30x faster inferencing than the H100. This accordingly translates to as much as a 25x TCO reduction. Blackwell is also designed with better interoperability in mind, which we believe to be a key advantage in reinforcing Nvidia’s market share gains in the transition to accelerated computing. The new architecture, which is defined as more than just a chip, but instead a system, is compatible for all computing environments, spanning “hyperscale to enterprise, training to inference, x86 to Grace CPUs, Ethernet to InfiniBand networking, and air cooling to liquid cooling.”

Blackwell is also seamlessly integrated with Nvidia’s improving full-stack software, AI capabilities, and next-generation networking technologies to enable further advancements in industry AI developments. For instance, the company has recently introduced NVIDIA Inference Microservices (“NIMs”), which leverages its proprietary CUDA framework in better facilitating enterprise generative AI developments. Specifically, NIMs represents a compilation of “cloud-native microservices” designed to optimize inferencing on popular large language models (“LLMs") from industry leaders like Google, Microsoft, Meta Platforms, and Hugging Face. The use of NIMs has proven to accelerate deployment “from weeks to minutes,” which again enables efficiency gains and competitive TCO for customers.

In addition to software, Nvidia has also enhanced its networking capabilities. Given increasingly complex workloads and massive AI clusters in accelerated data centers, networking solutions play a critical role in improving scalability for customers. And Nvidia has continued to address this growing demand for networking solutions capable of supporting the accelerating volume of “AI factories” underpinned by “hundreds to tens of thousands of GPUs.”

In the latest networking development, Nvidia has introduced Spectrum-X, its proprietary Ethernet enhancement solution optimized for handling AI workloads. Specifically, Spectrum-X addresses the performance bottleneck of currently available Ethernet solutions in supporting communication between massive GPU clusters for AI training and inferencing. The new family of products include the Spectrum-4 switch and BlueField-3 DPU, which coupled with Nvidia’s full-stack software can augment traditional Ethernet networking performance by up to 1.6x. This is particularly fitting for improving scalability in executing complex and compute-demanding AI workloads.

Spectrum-X is already in volume shipment, with robust adoption across multiple customers to support massive AI clusters of up to 100,000 GPUs. This does not only provide validation to the performance and efficiency gains enabled by the innovative solution, but complements Nvidia’s broader networking product portfolio, spanning NVLink and InfiniBand, in enabling an adjacent multibillion-dollar product line.

3. Multi-Year Demand Resilience

While H100 GPU volumes have improved, Nvidia expects growth to remain a function of supply availability, especially as its next-generation chips enter production. The company confirmed during the latest earnings update that its latest H200 GPUs, which starts volume shipment later this quarter, remains supply constrained. Meanwhile, products based on the next-generation Blackwell architecture are also observing demand that is expected to remain “well ahead of supply” through next year.

Specifically, Blackwell system availability at launch is expected to double that of Hopper’s. This accordingly highlights a sustained data center demand environment for Nvidia, propelled by the next-generation architecture’s mission-critical role in supporting the ongoing transition to accelerated computing.

More importantly, we view Nvidia as still being in the early stages of an up to $2 trillion upgrade cycle underpinned by the transition of general purpose to accelerated computing. Specifically, much of the demand for Nvidia GPUs observed to date is for the build-out of brand new, accelerated data centers. It is essentially a replacement cycle for traditional CPU-based data centers, which paired with supporting software and networking solutions, management expects to create an annualized TAM of $250 billion in the next four years. And this will eventually transition to an upgrade cycle, whereby data centers running Ampere- and Hopper-based GPUs over the past several years upgrade to Blackwell+. With Nvidia’s end-to-end accelerated computing system still viewed as the industry’s gold standard, we expect durability to the company’s growth trajectory, underpinned by its leadership in capturing the majority of the accelerated computing total addressable market ("TAM") ahead.

Stock Split Implications

In addition to continued durability over its outsized growth outlook, Nvidia’s recent decision for a 10-for-1 stock split taking effect in June marks another near-term booster for its valuation. The company last split its shares into four in July 2021 when they were worth about $600 apiece. At the time, the Nvidia stock appreciated almost 25% during the period between the stock-split announcement in May 2021 through effectiveness in July 2021.

This is consistent with the post-split strength observed across its mega-cap peers like Apple and Tesla in 2020 before the latest cycle of Fed rate hikes spooked markets. Both Apple and Tesla saw their respective share prices surge towards new heights immediately after their respective stock splits at the time. This was likely thanks to incremental demand from a new group of individual investors that previously did not have access to the stocks due to their elevated per piece prices.

Nvidia is expected to benefit from a similar post-split upsurge this time around, given its mission-critical role in supporting AI developments, as well as favorable momentum from the broader market recovery. Admittedly, stock splits do not change underlying fundamental drivers of valuation prospects. However, they have typically been accompanied by a post-split boost. This is primarily driven by robust retail demand due to improved per piece affordability for those who previously did not have access to “fractional” shares – especially for fundamentally strong names like Nvidia during a risk-on environment. Any ensuing valuation upsurge could also result in options-driven implications and increased volatility, such as a potential short squeeze.

Fundamental Considerations

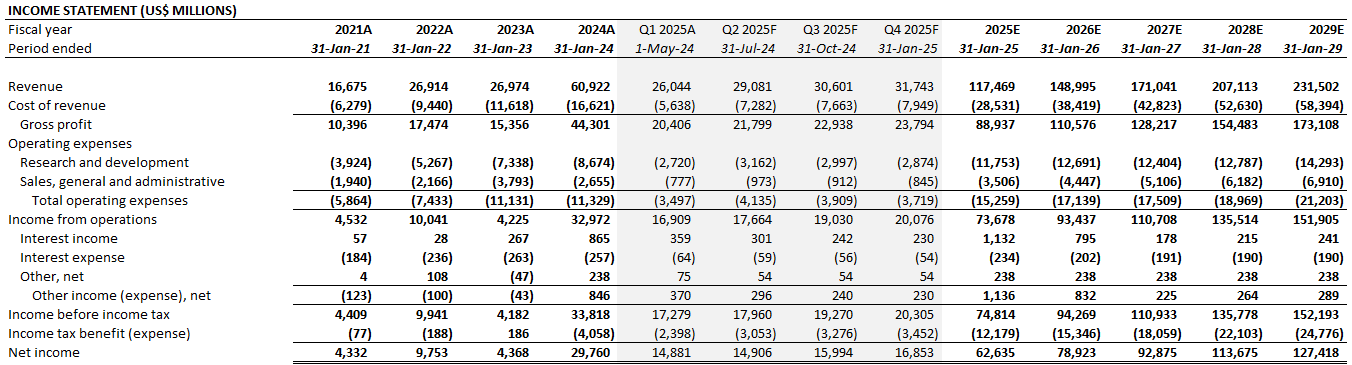

Adjusting our previous forecast for Nvidia’s actual first quarter performance and outlook considering the foregoing analysis, we expect the company to grow FY 2025 revenue by 93% y/y to $117.5 billion.

Author

Data center sales are expected to remain Nvidia’s core growth driver. In addition to the continued tailwind of improving H100 GPU supplies, the upcoming shipments of next-generation accelerators, such as the H200 and Blackwell platform, also provide reinforcement to Nvidia’s growth outlook. As discussed in the earlier section, capex and R&D prioritization on AI infrastructure remains resilient across Nvidia’s core hyperscaler customers. Meanwhile, improving supply availability is also allowing Nvidia to partake in continued growth stemming from a diversified demand environment across enterprise verticals, particularly the automotive industry.

Meanwhile, Nvidia’s profit outlook is also expected to improve as higher-margin data center sales continue to ramp at scale. This is consistent with management’s guidance for F2Q gross profit to potentially exceed the mid-70% range on a GAAP basis, which reinforces further margin expansion for full year FY 2025. This will likely further Nvidia’s valuation gains from current levels, which have primarily been underpinned by tangible fundamental strength over the past year.

Author

Price Considerations

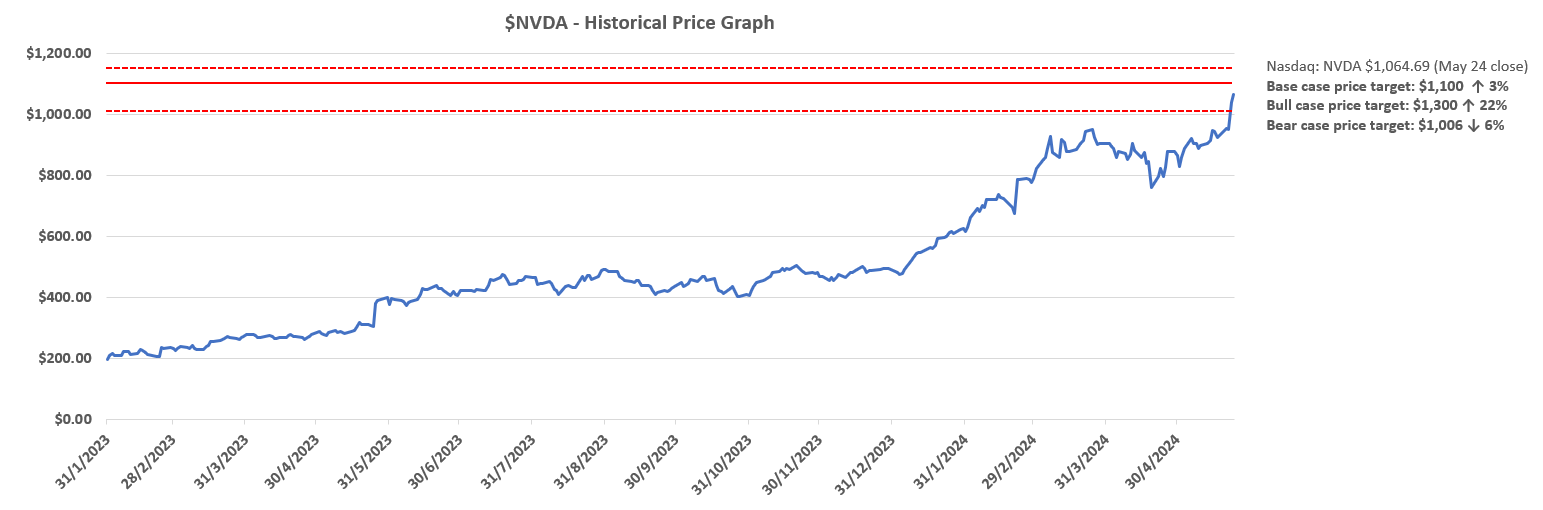

On a pre-split basis, we believe the Nvidia stock will continue to find durability in the $1,000+ range. Our base case price target, adjusted for its latest results and near-term outlook, is set at $1,100.

Author

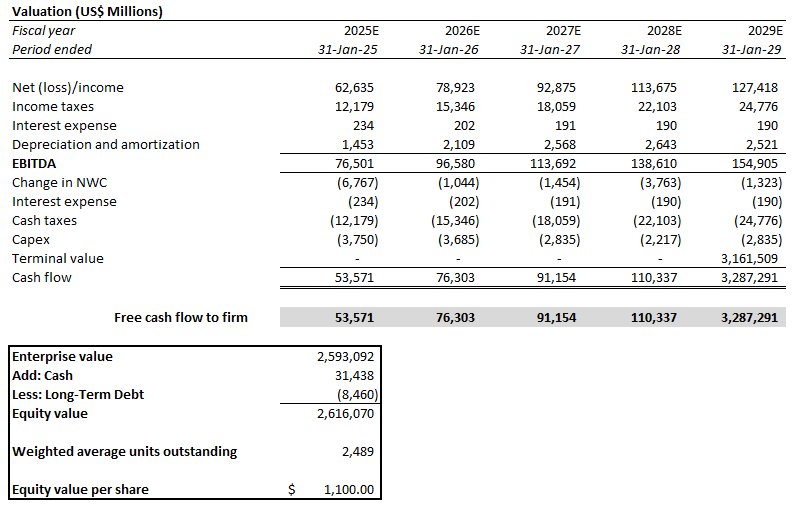

The price is set based on the application of a 35.8x NTM EV/EBITDA multiple on Nvidia’s FY 2025E EBITDA projection of $76.5 billion, considering 2.5 million diluted shares outstanding. The FY 2025E EBITDA projection is taken with our fundamental forecast discussed in the earlier section. Meanwhile, the valuation assumption of 35.8x NTM EV/EBITDA applied considers Nvidia’s current valuation at 31.1x, with a 15% premium. The 15% premium is consistent with the average jump observed in the NTM EV/EBITDA multiples of Apple (23x to 26x) and Tesla (58x to 70x) during the week of their respective stock splits in August 2020 when markets were in a risk-on environment. We believe this premium is warranted given Nvidia’s fundamental strength and leadership in supporting ongoing AI momentum.

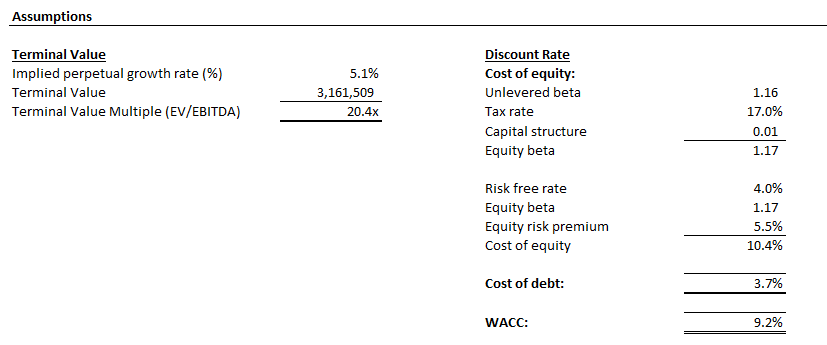

The estimated price resulting from the multiple-based approach is also consistent with our discounted cash flow ("DCF") analysis on projections taken with the fundamental forecast. Specifically, the DCF analysis also considers a WACC of 9.2% and an implied perpetual growth rate of 5.1% on FY 2029E EBITDA, and results in an estimated price of $1,100 apiece. The WACC considered is consistent with Nvidia’s risk profile and capital structure. Meanwhile, the premium terminal value assumption is reflective of applying a 3.5% implied perpetual growth rate on FY 2034E EBITDA, which is consistent with the normalized pace of economic expansion across Nvidia’s core operating regions.

Author

Author

Conclusion

Admittedly, Nvidia continues to trade at a lofty premium at current levels. Yet, its downside risks remain limited in the near-term, in our opinion, especially given Nvidia’s robust fundamental outlook underpinned by a longer-horizon AI-focused investment cycle across all industries.

Although a gap persists between the level of capex allocation to AI infrastructure (inclusive of Nvidia hardware and supporting full-stack software services) and AI-related monetization, we expect this margin to diminish as inferencing activity continues to ramp with the deployment of generative AI applications at scale. We believe Nvidia’s growth outlook is further reinforced by its reputation as the gold standard in hardware critical to supporting the increasingly urgent transition to accelerated computing. Taken together with Nvidia’s upcoming stock split, which we view as a positive catalyst for the stock, we expect a further valuation upsurge from current levels in the near-term.

Comments

Great article, would you like to share?

Here’s my take on Nvidia’s current state of play: Short-term Bears may have their say, but long-term Bulls are here to stay.

Nvidia’s Bullish Blueprint Amid a Bearish Blip 🙀

For the Bears: For those who doubt and share despair, Nvidia’s dip might make you stare:

1. MACD: Bearish, with the MACD line below the signal line.

2. RSI: 38.7, indicating it is in the sell zone and nearing oversold conditions.

3. Stochastic Oscillator: 26.3, showing the stock is oversold.

4. Bollinger Bands: Price near the lower band, indicating oversold conditions.

5. Candlesticks: Recent patterns suggest increased selling pressure.

6. Volume: High but not indicating a reversal.

7. Williams %R: -85.2, indicating oversold conditions.

8. CCI: -110.3, confirming a bearish outlook.

These indicators suggest a bearish trend for Nvidia in the short term.

For the Bulls: For those with vision, a future bright, Nvidia’s climb will soon take flight.

Based on a comprehensive analysis of Nvidia's current situation, including fundamental strengths, market trends, and upcoming events, here's my charge for the Bulls:

Key Points:

1. Strong Fundamental Outlook:

- Nvidia's significant role in AI developments and its robust product pipeline, including the H100, H200, and upcoming Blackwell chips, position it well for continued growth [oai_citation:1,NVDA - Nvidia Corp Stock Trader's Cheat Sheet - Barchart.com](https://www.barchart.com/stocks/quotes/NVDA/cheat-sheet) [oai_citation:2,NVDA Technical Analysis (NVDA) - Investing.com](https://www.investing.com/equities/nvidia-corp-technical).

- The company's recent earnings report showed strong demand, particularly in the data center segment, which grew 428% year-over-year [oai_citation:3,Nvidia Stock Price Today | NASDAQ NVDA Live Ticker - Investing.com](https://www.investing.com/equities/nvidia-corp%20).

- Nvidia is also expanding into new markets, such as the automotive sector, which adds to its growth potential [oai_citation:4,NVDA - Nvidia Corp Stock Trader's Cheat Sheet - Barchart.com](https://www.barchart.com/stocks/quotes/NVDA/cheat-sheet).

2. Stock Split Catalyst:

- The 10-for-1 stock split, effective in June, is historically a positive catalyst for stock price appreciation as it increases accessibility for retail investors [oai_citation:5,NVDA - Nvidia Corp Stock Trader's Cheat Sheet - Barchart.com](https://www.barchart.com/stocks/quotes/NVDA/cheat-sheet).

- Previous stock splits in similar companies like Apple and Tesla have led to significant post-split price increases due to increased demand from new investors [oai_citation:6,NVDA Technical Analysis (NVDA) - Investing.com](https://www.investing.com/equities/nvidia-corp-technical) [oai_citation:7,NVDA - Nvidia Corp Stock Trader's Cheat Sheet - Barchart.com](https://www.barchart.com/stocks/quotes/NVDA/cheat-sheet).

3. Market Sentiment and Analyst Expectations:

- Analysts, including those from LIVYinvestment, project the stock to reach around $1,100, driven by Nvidia's strong earnings, market position, and the upcoming stock split [oai_citation:8,NVDA - Nvidia Corp Stock Trader's Cheat Sheet - Barchart.com](https://www.barchart.com/stocks/quotes/NVDA/cheat-sheet) [oai_citation:9,Nvidia Stock Price Today | NASDAQ NVDA Live Ticker - Investing.com](https://www.investing.com/equities/nvidia-corp%20).

- The stock's valuation is expected to remain strong due to Nvidia's critical role in the AI and accelerated computing market [oai_citation:10,NVDA - Nvidia Corp Stock Trader's Cheat Sheet - Barchart.com](https://www.barchart.com/stocks/quotes/NVDA/cheat-sheet).

Conclusion:

Given Nvidia's strong fundamental outlook, robust demand for its products, the upcoming stock split, and positive analyst expectations, it is likely that the stock will see upward momentum, possibly reaching or surpassing $1,100 by June 7. Continued monitoring of market conditions and any significant news is recommended for the final days leading up to the expiration date.

🚀🚀🚀 When Bears see Nvidia's dip and mope, they miss the long-term Bullish scope. For in the tech world, trends can flip, and Nvidia's bound for another trip. 🚀🚀🚀

@TigerPM @Tiger_chat @Tiger_story @TigerObserver @Tiger_Earnings @MillionaireTiger @Tiger_comments @Daily_Discussion @CaptainTiger @SPACE ROCKET