Abstracts

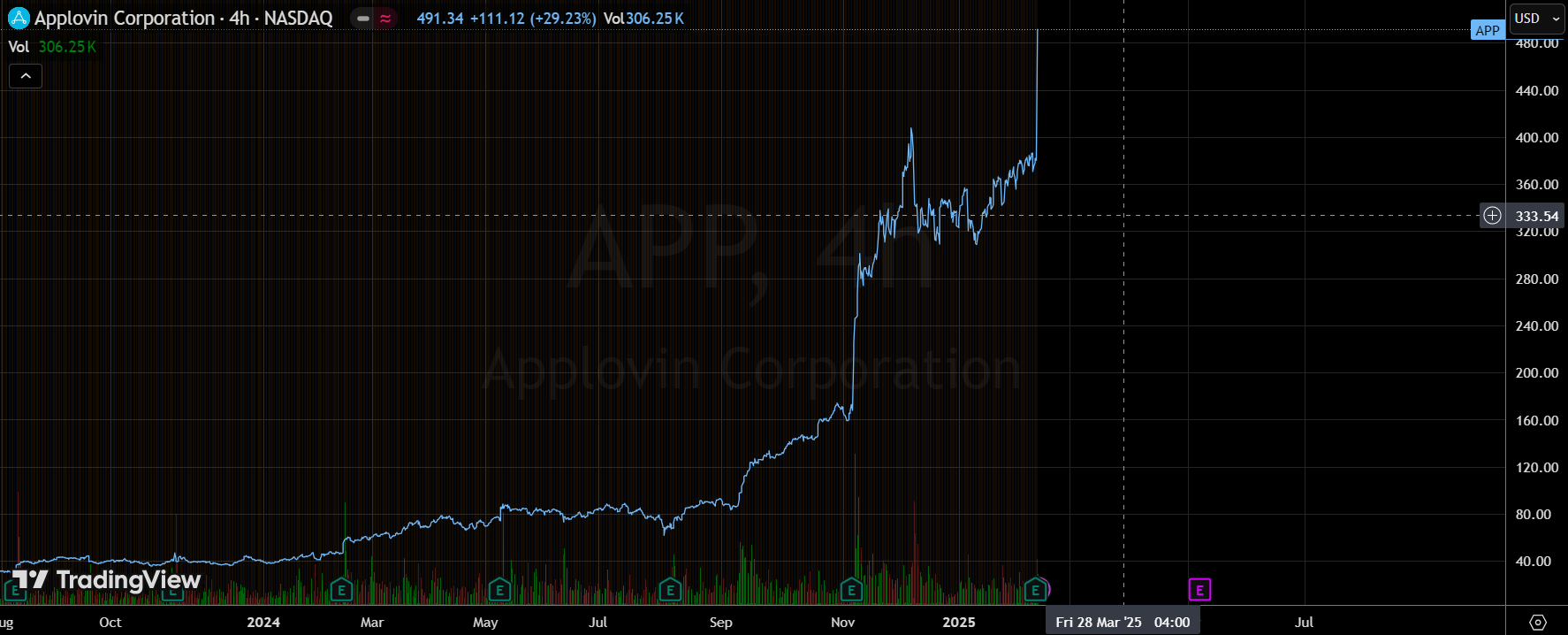

The most watched growth stock of the week , $AppLovin Corporation(APP)$ nnounced its 24Q4 results after the bell on February 12 and surged over 30% again after hours.

With a market share of 10% in the advertising intermediary industry, Applovin is already the leader, even leaving behind $Alphabet(GOOG)$ $Alphabet(GOOGL)$ $Meta Platforms, Inc.(META)$ the key component is the e-commerce advertising market .

The most critical part is the growth of e-commerce advertising, aka cross-border e-commerce placement in China, which is the main incremental market for META;

Management is thinking clearly, divesting part of its gaming business but improving the company's operational efficiency, while expecting more from its e-commerce business.If the short-term competitors such as $Unity Software Inc.(U)$ TikTok, META and other efficiency issues are not resolved, then Applovin's strong period is expected to continue

EBITDA margins are expected to improve further in FY25, and although the current valuation is not low, the market is valuing the company on the basis of expectations for FY26 and FY27 after growth.

Performance and market feedback

Q4 overall results and 25Q1 guidance both significantly exceeded expectations, and the buyer's expectations were already very high, so this Strong Surprise made the market give very optimistic feedback as a matter of course, and it went all the way up to +30% after +15% after the bell.

Previously well-known analyst Lauren Balik short APP's logic is not conflicting, misleading users to click on ads, game ads loading rate is too high, indeed there are problems, but the result is still the actual increase in the company's revenue, and in the peer group can not get the same technology to gain market share.The subsequent divestment of related businesses can also diversify some of the risks.The overly complex shareholding and suspected irregularities are also subject to further verification.

Key Investment Points

Rapid growth in e-commerce business with significant market share gains

Largest e-commerce customers' budgets in Applovin in 2025 are 6 times higher than in 2024, showing the confidence of e-commerce customers in the Applovin platform.

Applovin is already close to 10% of e-commerce budgets, ahead of TikTok and close to Google.

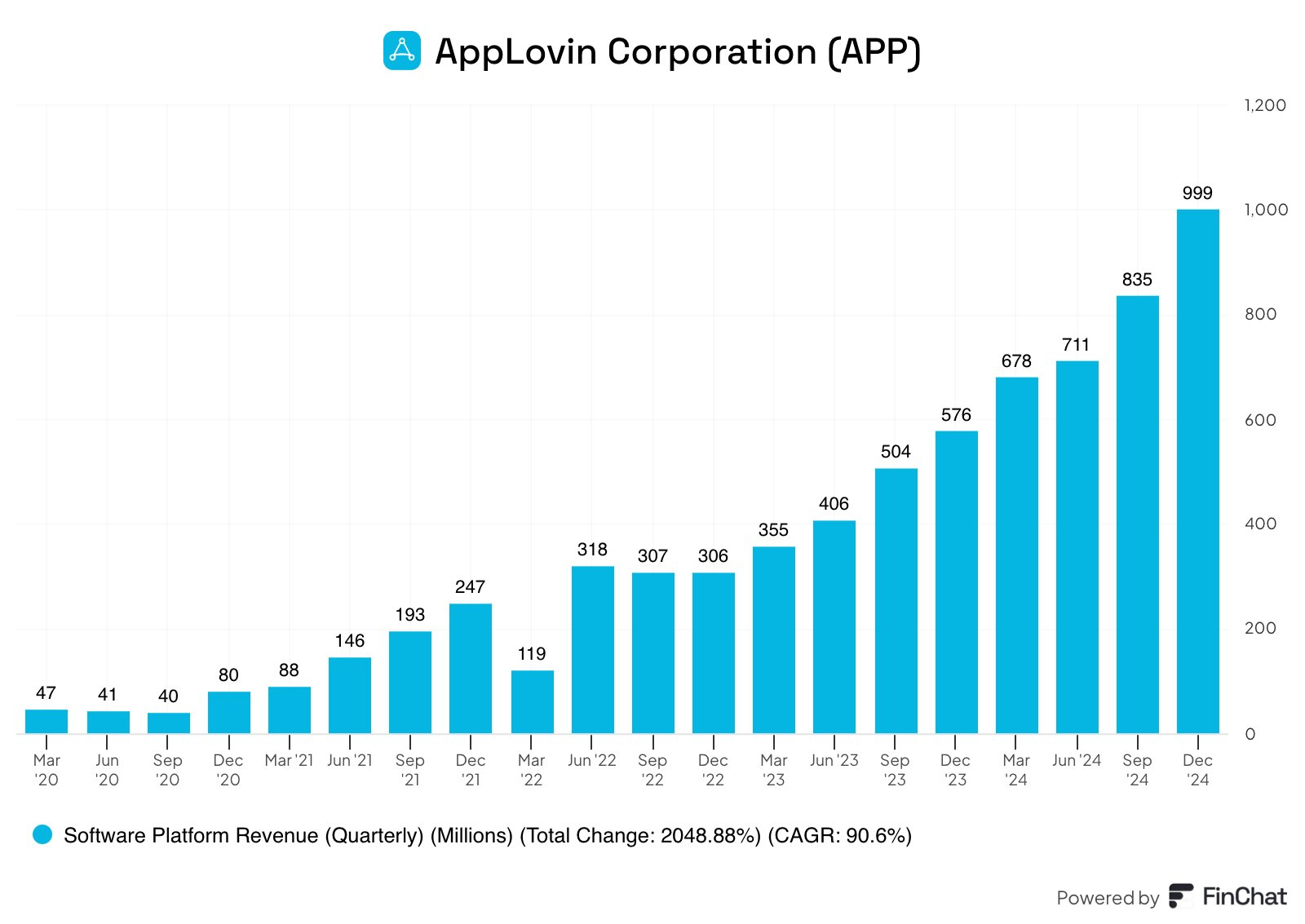

Q4's $1 billion ad revenue may include $50-100 million in e-commerce ad revenue, higher than expected .

Profitability remains stable, cost control still needs attention

The overall company realized EBITDA margin of 61.8% in Q4, slightly exceeding market expectations.

Advertising margin actually decreased YoY to 77.7% from 78.2% in Q3, requiring attention to cost control.

Management has high confidence in the company's operational efficiency and guided EBITDA margin to 63%-64% level from 62% in 4Q24.

Positive future outlook, but risks and uncertainties remain

Q1 advertising revenue is expected to grow at 52%-55% year-on-year, significantly higher than market expectations

1Q guidance is subject to risks such as Trump's De minimis disruption, leap year impact and exchange rate impact, but these issues may require further guidance

The e-commerce business is currently expected to be high, the company's existing challenge is that it has not yet accumulated the same user data as the gaming industry, it is difficult to have a large amount of IDFA data like META, and there are difficulties in doing Re-Targeting data.However, if we broaden to IAP, we will have the consumer behavior and consumption data of IAP users, and we may be able to expand our market share very quickly.

Valuation

Applovin has reached 10% market share in the ad intermediary industry and is the leader in the game customer acquisition ad segment, even surpassing Google and Meta.

If all Q4 ads are included in game-based ads, Applovin's market share has reached more than 30% in 2024, up 10pct compared to 2023.

The market share is expected to increase further in the future with Axon 2.0, but the difficulty is increasing.

The core risks to Q4 results are whether the company pursues maximizing revenue or maximizing advertising budget, as well as Take Rate and China customer placement.

The e-commerce business faces challenges in data accumulation and business advancement, as well as risks that the ceiling is not yet clear.

Comments