$Snowflake(SNOW)$ Came to a stage of margin expansion for large SaaS companies and bumped up against the rapid expansion of AI offerings, which ushered in further favorable results.

Earnings and market feedback

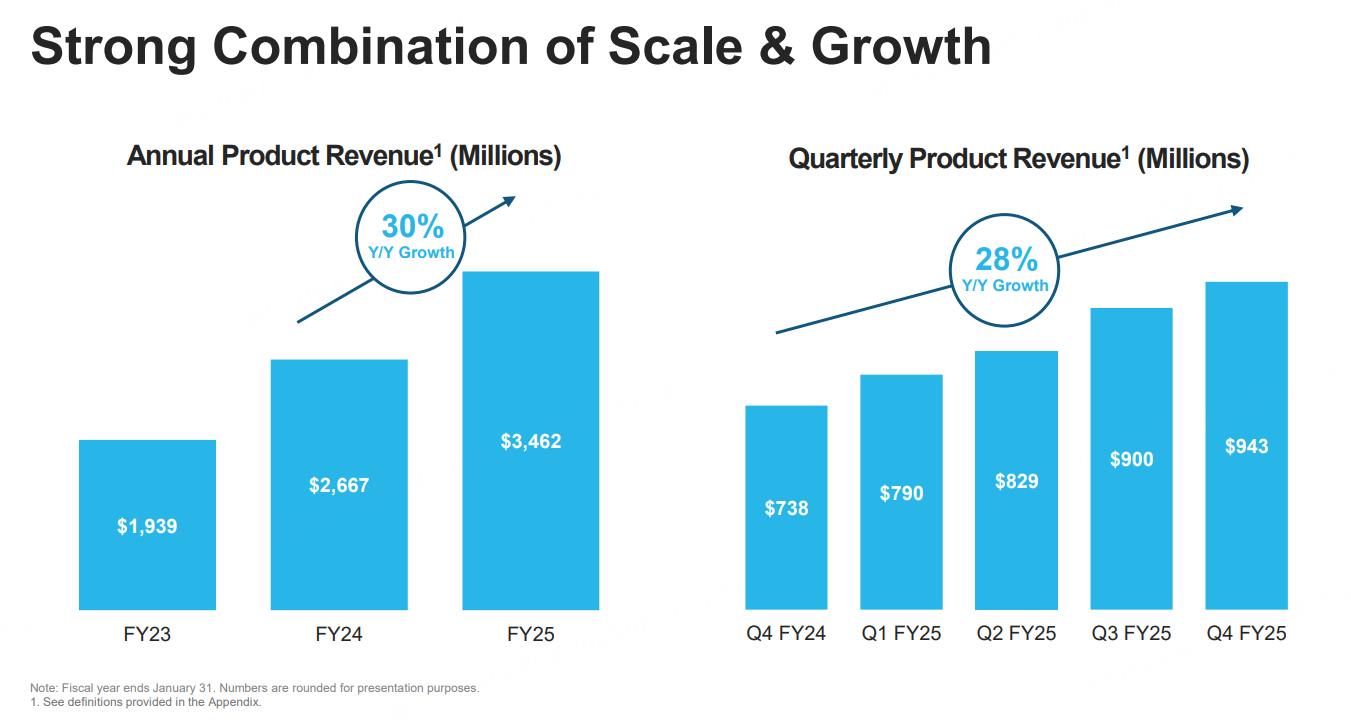

Q4 FY2025 results were announced after the bell on the 26th, continuing to show strong growth + beating market expectations across the board.

Q4 overall Top line and Bottom line both exceeded expectations, with Top line Surprise ranging around 3%; product revenue of $943.3M + 28% YoY, beat consensus $918.8M;

Guidance for FY26 is very clear and strong, with product revenue expected to be $4.28bn (> consensus $4.23bn), of which $955-$960m (YoY +21-22%) in Q1; Adjusted operating margin target upgraded to 8% (vs. 5% in FY25), with the earnings pathIs mostly scale effects, AI efficiencies, and operational moves (e.g., hiring slowdown, stock incentives, etc. will also decline)

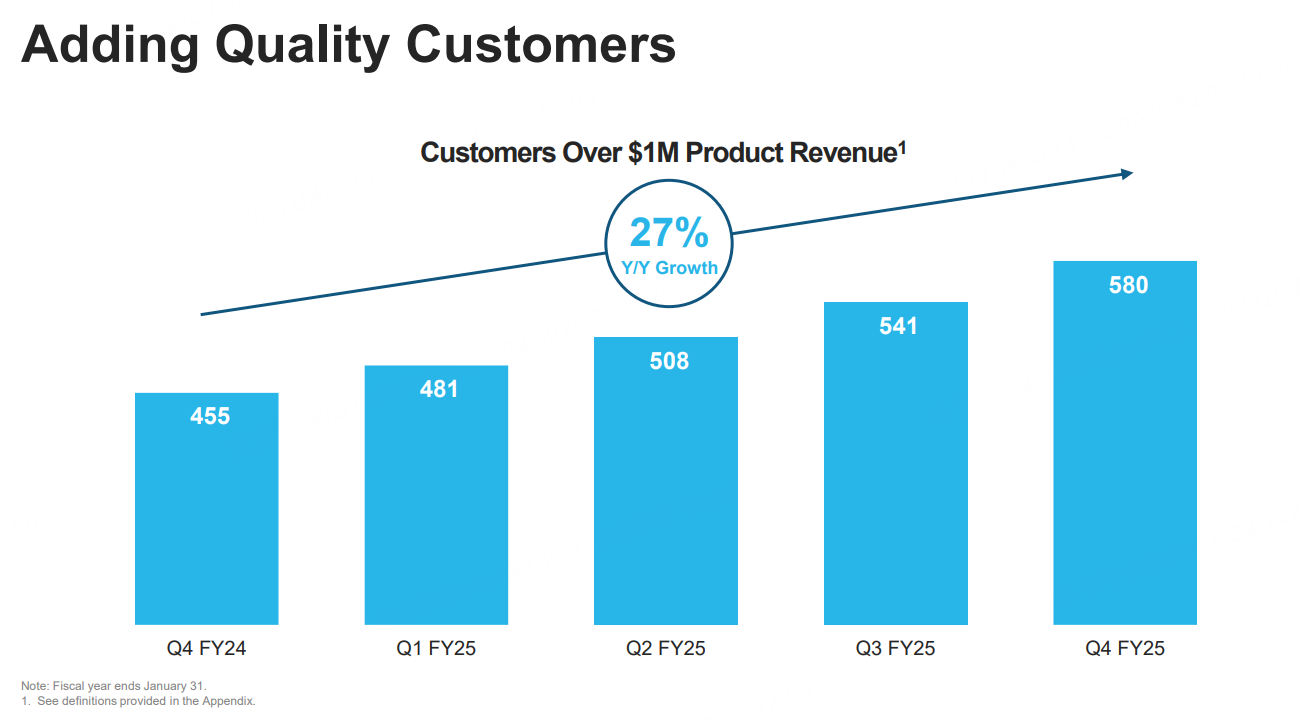

Net Dollar Retention at 126% (-4pct YoY, but >124% consensus), largely stabilized, but above industry average with 1M+ revenue "high quality customers" +27% YoY;

New products and AI-driven: Iceberg has attracted 300+ customer trials, supports direct access to cross-cloud data lakes, and is expected to reach 100-200x the amount of data of existing customers; AI product matrix Cortex AI platform, which has gained 750+ customers in two months), and Snowpark Container Service (which has been adopted by 50% of customers), reduce the cost of inference services by 40%, and accelerate AI modeling.Reduce 40%, accelerate AI model deployment

RPO +33% YoY, higher than revenue growth, cRPO +27% YoY, broadly in line with revenue growth, the

After-hours trend咋 earnings report within 1 minute after a large fluctuation, but then it has been stuck at 10%, the market may first worry about its margins, but mainly the impact of the SBC, adjusted margin performance exceeded expectations, and at the same time, the current new product Iceberg has just been launched, the initial period may be a negative impact on the Margin, but in the FY26 is expected to be very good.

Investment Key Points

The commercialization of Iceberg is likely to become a business unit with outstanding contribution in FY26

Early customer scale: 300+ enterprises have entered the technology validation phase in Q4, covering core enterprises such as financial services (JPM), retail (WMT), etc.; the first commercial customers contributed ~$1.5M QoQ, accounting for 32% of the new product line's revenue.

Technology Enhancement: Average Iceberg data volume managed by a single customer reaches 15PB, which is 50 times higher than traditional tabular format; cross-cloud data lake query performance is improved by 3-5 times, and storage cost is reduced by 40%.

Achieve global metadata synchronization across AWS S3, Azure Data Lake, data discovery efficiency increased by 70%; ACID features completed technical preview, planned FY26Q1 official GA; performance optimization: query engine refactoring to increase the speed of complex Join operations by 4 times

CEO's enhanced Data Engineering (Data Engineering) strategic intent focus: is changing Data Engineering from a cost center to a value creation engine.

Acquired Datavolo to enable full domain crawl of enterprise unstructured data, including Google Drive, SharePoint, and more;

Launched Dynamic Tables technology, enabling customers to reduce the size of their data engineer teams by 30% while increasing the number of tasks handled by 2.5x;

Data Engineering product line annualized revenue exceeded $200M, growing at +85% YoY, the fastest business unit; 87% of newly signed contracts included data engineering module purchase clauses

Collaboration with $Amazon.com(AMZN)$ AWS: exclusively enables Anthropic models to run within Snowflake's security perimeter, avoiding cross-border data risks.

Also announced is an expanded partnership with $Microsoft(MSFT)$ that gives customers direct access to the latest OpenAI models;

Meanwhile OpenAI is working hard to migrate from $Datadog(DDOG)$ to a new framework of Grafana+SNOW/Databricks and has already made a full switch attempt last December, which failed but the migration process and end game is hard to change

Cost reductions and efficiencies: the CFO left, but the market had previously expected this. the stock-based compensation (SBC) cost impact of FY26 will not be too aggressive; along with possible layoffs, etc.

78% of RPO is expected to be recognized in the next 12 months; revenue growth may be conservative;

Margin improvement path: sustainable source of Non-GAAP operating margin improvement from -2% to 5%:

Scale effect: 18% year-over-year reduction in infrastructure costs per dollar of revenue

AI efficiency improvement: customer support team processing efficiency increased by 30% through AI work order system

Operational efficiency improvement: annual output per sales rep increased from $4.5M to $5.2M, and customer acquisition costs decreased by 22%.

Snowflake is building a three-dimensional growth flywheel through technology upgrades (Iceberg/Cortex), efficiency optimization (AI-driven operations), and eco-expansion (Marketplace).

Comments