$Okta Inc.(OKTA)$ This quarter's results validate the success of the transition from "high growth" to "high quality growth" (continued turnaround), and 2026 expectations are conservative but still ahead of the market.The 2026 forecast is conservative, but still ahead of market expectations.

Performance and market feedback

Core Financial Indicators

Revenue: $682M (+12.7% yoy), beating market expectations of $668.9M.

Earnings per share (EPS): $0.78 (+24% yoy), beating estimates of $0.74.

Operating Profit: $168M (+30.2% yoy), operating margin improved to 1.2% from -13.7% a year ago.

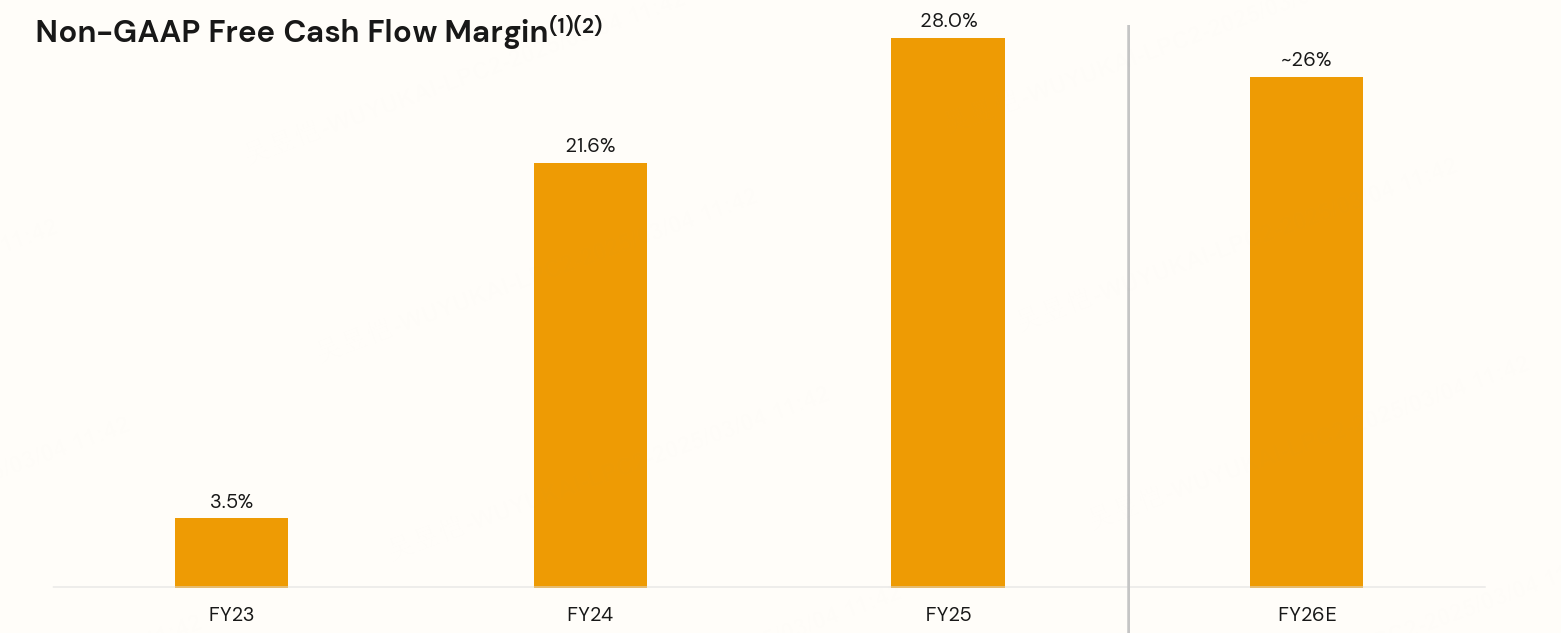

Free Cash Flow: Free cash flow margin of 41.6% (23.2% last quarter) and full year operating cash flow of $750M (+46% yoy).

Operational Efficiency Highlights

Subscription reserve: exceeded $4B (+25% yoy) with new products contributing 20% of subscription revenue.

Customer conversion rate: website traffic declined by 6.22% but revenue grew, reflecting improved conversion efficiency of paying customers.

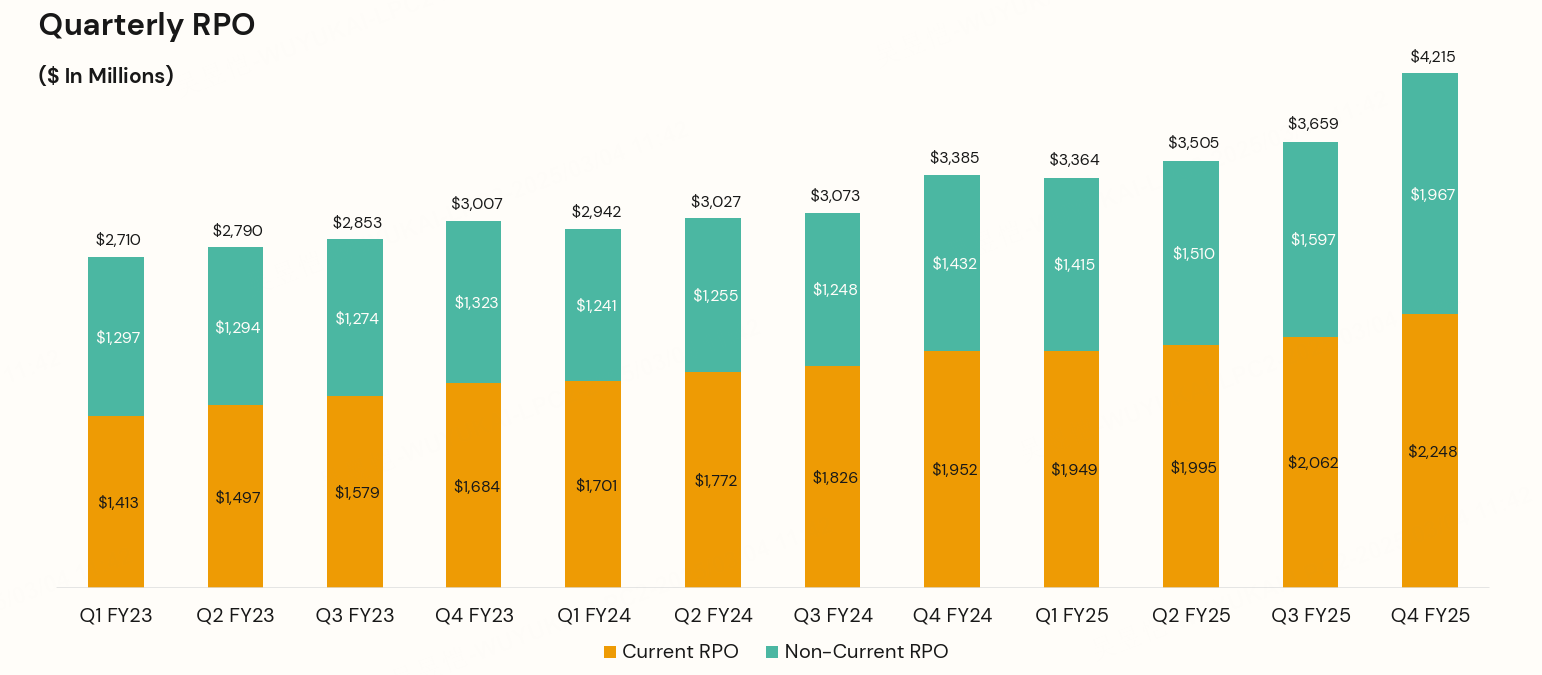

Total Contract Value (TCV): exceeded $1B for the first time, with subscription backlog (RPO) up 25% yoy to $4.215B.

cRPO (Current Remaining Performance Obligation): $2.18B-$2.19B (+12% yoy) with increased visibility into future revenue.

Website Traffic Change: Website traffic -6.22% reflects that there may be a bottleneck in the brand's ability to acquire customers, and we need to observe the subsequent adjustment of marketing strategies.

Market Feedback

Stock performance: After-hours surge of 15%, stock price accumulated +14.8% for the year, significantly outperforming the S&P 500 (+1.2%).

Investor Sentiment: Earnings beat expectations coupled with optimistic FY2026 guidance, market recognizes its SaaS model of "scale growth + margin improvement".

Investment highlights

Profitability Improvement: From "Burning Expansion" to "Profit Inflection"

Key figures: operating margin positive (1.2% vs -13.7% y/y), non-GAAP operating profit guidance of $710M (FY2026) beat by 13%.

Drivers: cost control (staff reduction and optimization), higher share of high margin subscription revenue (new products contributing 20% of subscription revenue).

Increased stickiness of major customers: number of customers with ACV over $1M reached 470 (+22% YoY);

Product synergies: Okta and Auth0 platform integration accelerating, identity security solutions expanding breadth of coverage, supporting RPO growth rebound to 25

Market concern: Can the surge in free cash flow ($750M for the year) be sustained?The company responded that it will maintain the strategy of "cash flow growth > revenue growth".

FY2026 guidance: growth and profitability both excellent

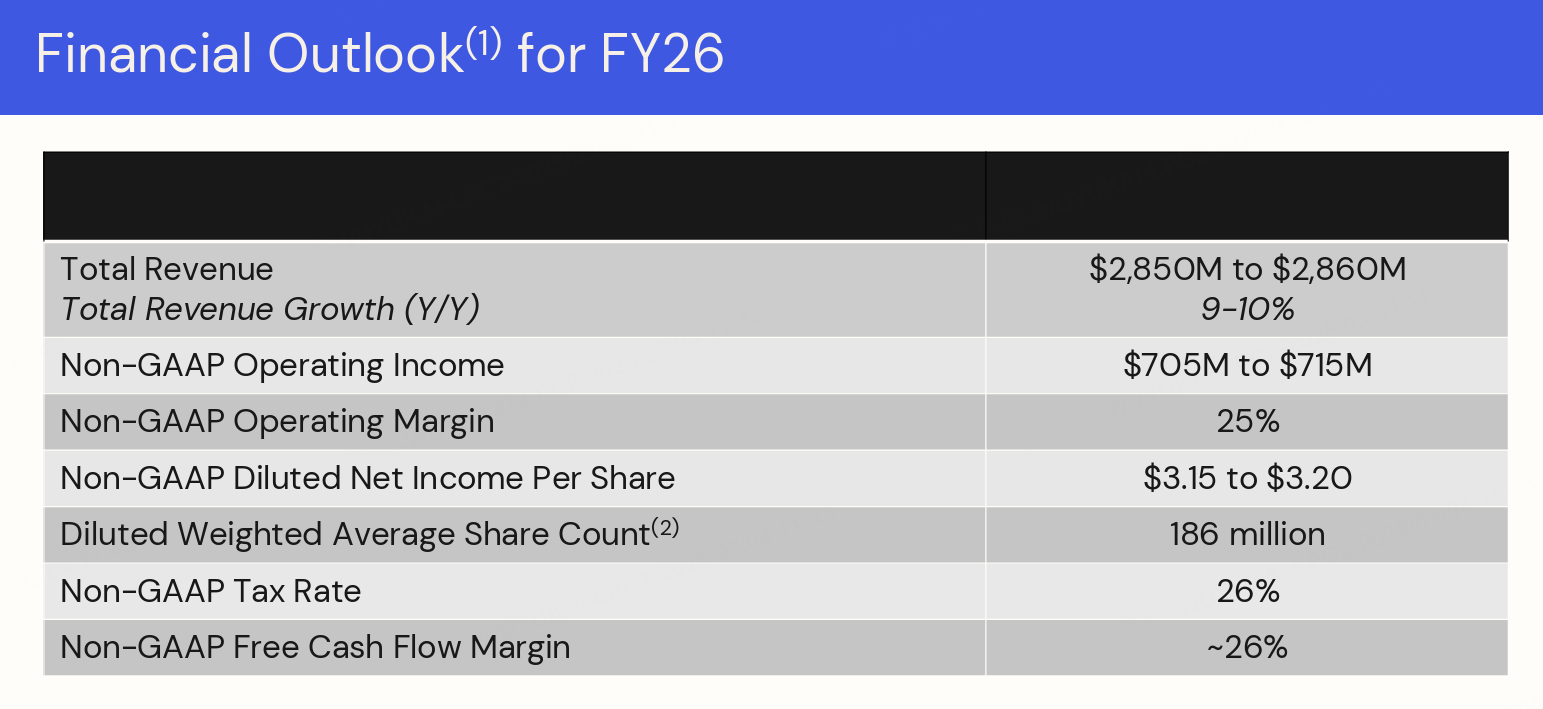

Revenue guidance: FY2026 revenue $2.85B-$2.86B (+9.4% yoy), ahead of market expectation of $2.8B.

Cost optimization: plan to cut expenses through organizational restructuring (Q1 cash impact of $11M), targeting non-GAAP operating margins to be maintained at 25

EPS guidance: FY2026 $3.15-$3.20 (beat $2.94), Q1 guidance $0.76-$0.77 (beat $0.70).Implied assumptions cRPO growth rate stabilizes (+12%), new product penetration increases (AI features on the ground).

AI integration and competitive barriers

AI strategy: CEO Todd McKinnon emphasizes the potential of AI in authentication and security, with plans to embed AI into core products (e.g., anomalous login detection, automated policy configuration).

Competitive barriers: Despite rivals such as Microsoft and Ping Identity ramping up identity management, Okta's vendor-independent positioning (not tied to public cloud) is a unique advantage; RPOs are accelerating to reflect customers' one-stop-shopping needs for multi-cloud identity management, and Okta's partner ecosystem (e.g., deep integrations with AWS, Azure) is a differentiator

Growth Sustainability: CEO Todd McKinnon emphasized that the structural rise in IT security demand and platform flexibility are long-term drivers, with a focus on "Okta Secure Identity Commitment" to raise industry standards by 25% by 2026.The focus on "Okta Secure Identity Commitment" in 2026 will raise industry standards by 25

Valuation

Current share price implies FY2026 P/S of ~10x (at $2.85B revenue), which is higher than the SaaS industry median of 8x, requiring higher growth to materialize;

According to the "Rule of 40", the sum of revenue growth (13%) and free cash flow margin (25%) amounted to 38%, which is one of the highest in the industry.

Comments