Big-Tech’s Performance

Weekly macro storyline: Exodus of "US Exceptionalism" trade.

In the last two weeks, market risk appetite has taken an extreme turn, with AI-narrative chipmakers tumbling, pulling the Nasdaq back as a whole, and risk aversion rising, while the Trump administration's tariffs have continued to make waves and even become a primary focus of the market.Investors lowered their dollar longs and flocked to Europe and Asia to diversify into the U.S. market.

Unlike the 2018 period, U.S. stock valuations are now at elevated levels, the market (institutional investor behavior with consistency such as CTAs) is cautious, and growth expectations are weakening (retail data from Walmart/Target/Bestbuy, etc.), overlaying not Price-in too much Trump policy uncertainty previously the market's current pullback can only be described as a gradual return to a reasonable range.The next trend will be more dependent on the fundamentals of the economy.

Big tech companies have naturally pulled back overall: Tesla's sales issues have worsened fundamentals (sales fell off a cliff in February, internally due to Model Y refresh and externally due to Elon Musk's DOGE/political rhetoric); Nvidia pulled back sharply post-earnings, and its forward P/E ratio is now at a 10-year low (around 24x). But investors reconsidering AI positions , discussions against arithmetic demand/secondary leads etc. also divided the market.

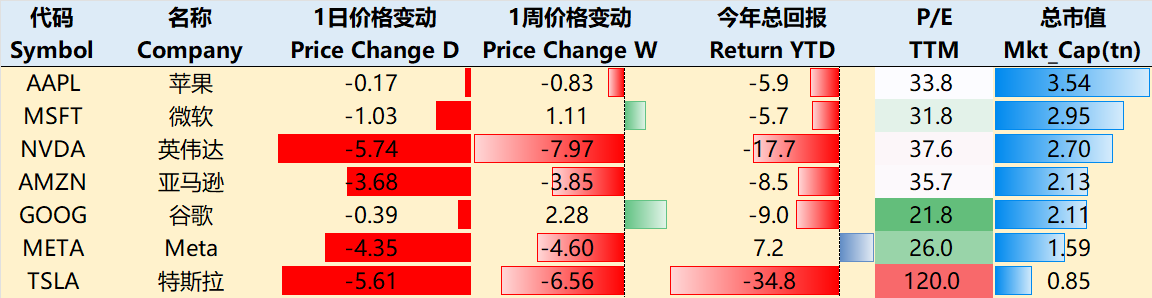

By the close of trading on March 6, big tech companies were lower across the board over the past week.Among them $Apple(AAPL)$ -0.83%, $NVIDIA(NVDA)$ -7.97%, $Microsoft(MSFT)$ +1.11%, $Amazon.com(AMZN)$ -3.85%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ +2.28%, $Meta Platforms, Inc.(META)$ -4.6% and $Tesla Motors(TSLA)$ -6.56%.

Big-Tech’s Key Strategy

Big Tech's volatility space from a valuation perspective

The sell-off in tech stocks has invariably brought about a reshaping of valuations, and with the rebalancing of AI positions, investors (major institutions) have begun to change their risk positions, overlaying quantitative, CTAs, and surprisingly, NVDA has begun to see a one-day plunge of 8% in the Great Escape.

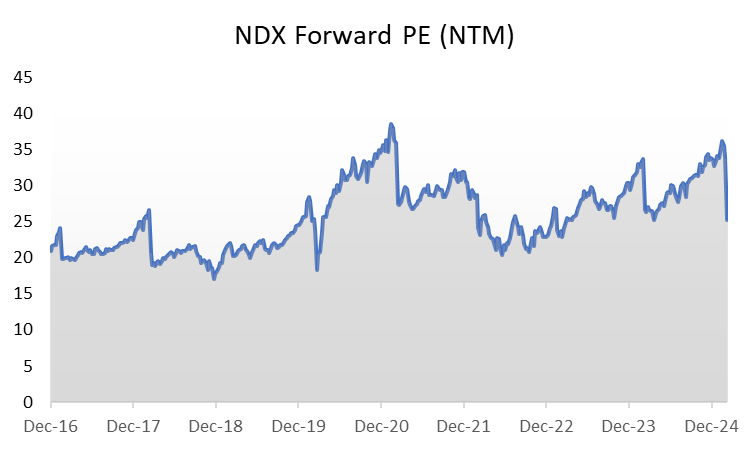

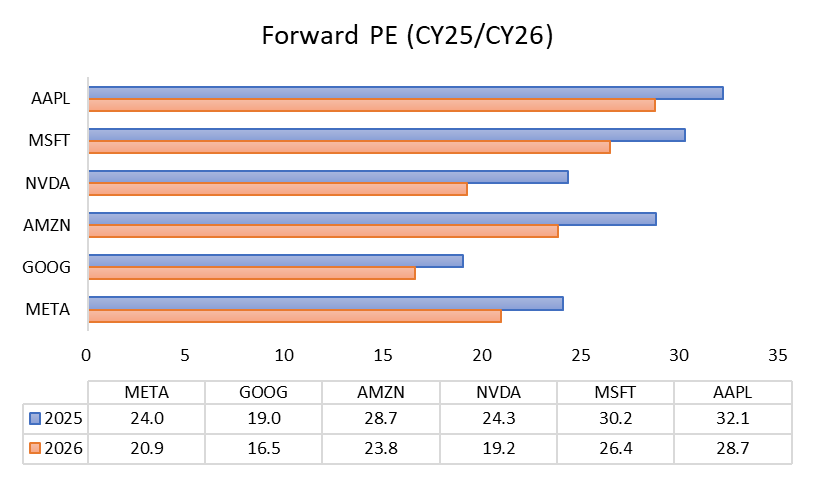

Just two weeks of change, so that NVDA's forward price-earnings ratio (Forward PE) fell to <25x, GOOG even fell below 19 times, a lot of investors to the "lowest valuation in 10 years" as a benchmark, so how much more specific "bottoming out"?Space?

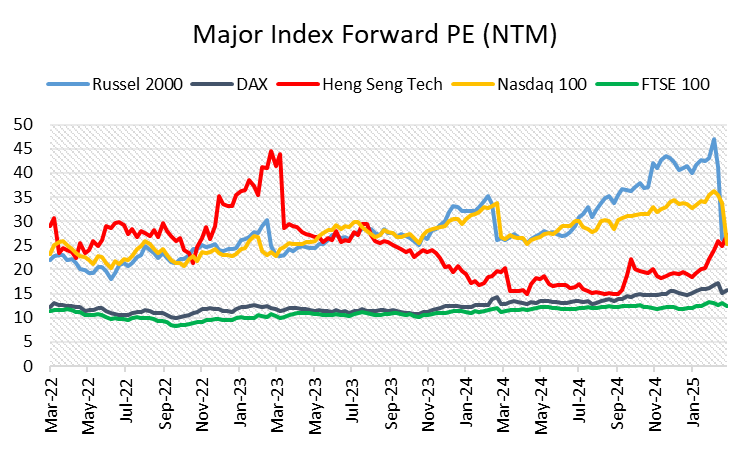

While U.S. stocks are currently experiencing a technical correction, the major indices are still at historically high valuations, with risk premium compensation more than adequate compared to major European valuations and the Hang Seng Index.

The Forward PE of the NDX index fell to 2019 levels after this week's sharp decline, but is still about 10% higher than during 2018

The small-cap premium is also fading in the recent overshoot.Looking at Forward PEs over the next 12 months, $HSTECH(HSTECH)$ $NASDAQ 100(NDX)$ $iShares Russell 2000 ETF(IWM)$ indexes are at nearly the same valuation level.

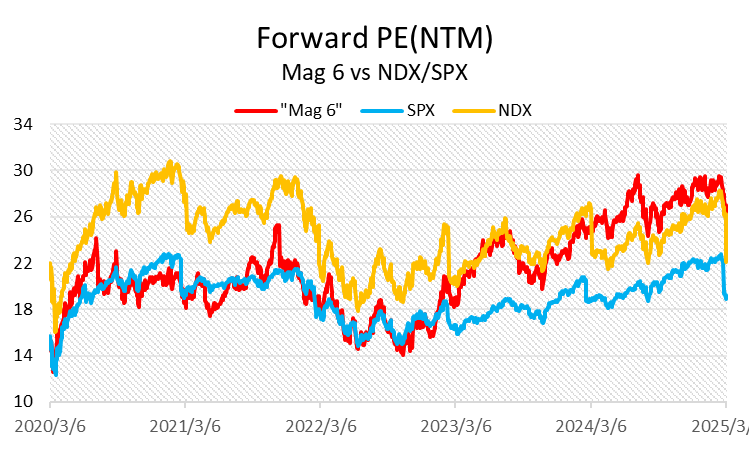

Big Tech ex TSLA "Mag 6" has a Forward PE of 26.3x, ahead of SPX's 18.9x and NDX's 22.1x. Concentration risk is still present, though it is expected to narrow;

Such a scenario does not necessarily represent equilibrium, and the current 10% correction is not enough to absorb valuation pressures if escalating trade frictions resonate with a macroeconomic stall.

Under a non-recession scenario, market volatility will give rise to structural trading opportunities:

There is always a window for valuation repair after technical overselling;

The downward channel is bound to be accompanied by a short-covering driven rally.

The real cautionary note is the risk of an economic hard landing, with the current S&P 500 dynamic P/E ratio nearly 20% higher than in 2018, and the potential room for retracement in the event of a systemic risk shock that could breach the 20% warning line.When the market correction breaks 15% and high-frequency economic data confirms recessionary signals, the Federal Reserve could revert to accommodative monetary policy, which could then restart the rate-cutting cycle and trigger a liquidity-driven rally.

Big Tech Options Strategy

Apple’s last stubborn?

AAPL had a relatively strong week with the release of its new MacBook Air with M4 chip, which went against the new tariffs and saw an overall $100 drop in pricing, while rumors swirled that the foldable iPhone could be expected to launch by the end of 2026;

It's been a month of several new product launches, including an iPhone SE with a larger OLED display, an iPad Air with an M3 chip, and a Mac Studio with an M4 Ultra chip. while all part of the product release planning, they also reveal Apple's current anxieties, including:

The actual utilization rate of the existing Apple Intelligence function suite is "extremely low", and the ability of the technology to land on the ground is doubtful;

Self-developed large language model has reached the capacity ceiling, unable to support the evolution of conversational AI needs, intelligent assistant habits may be cured by competitors in Apple's absence;

Self-research AI server capacity is still in the climbing stage, and the output of the AI field is not proportional to the input.

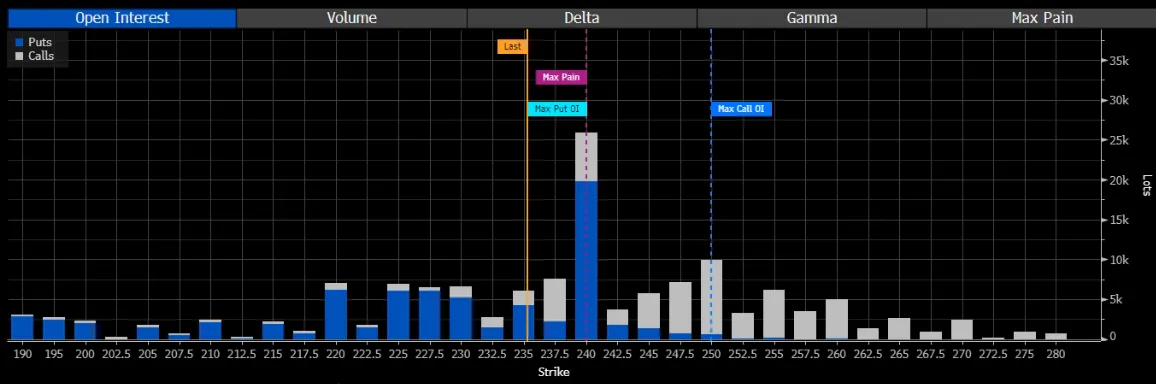

During this two-week tech stock pullback, AAPL stock price performance is relatively firm, its hard asset quality, heroic buybacks, and low relevance to AI are all reasons why it was spared, but none of this means that it hasn't been noticed, and next week's expiration of 240's PUTs have seen a sea of large orders, so much so that the maximum pain is actually more than the current price, which means that the shorts that are holding a large number of PUTs are currently in-the-money.

Big-Tech Portfolio

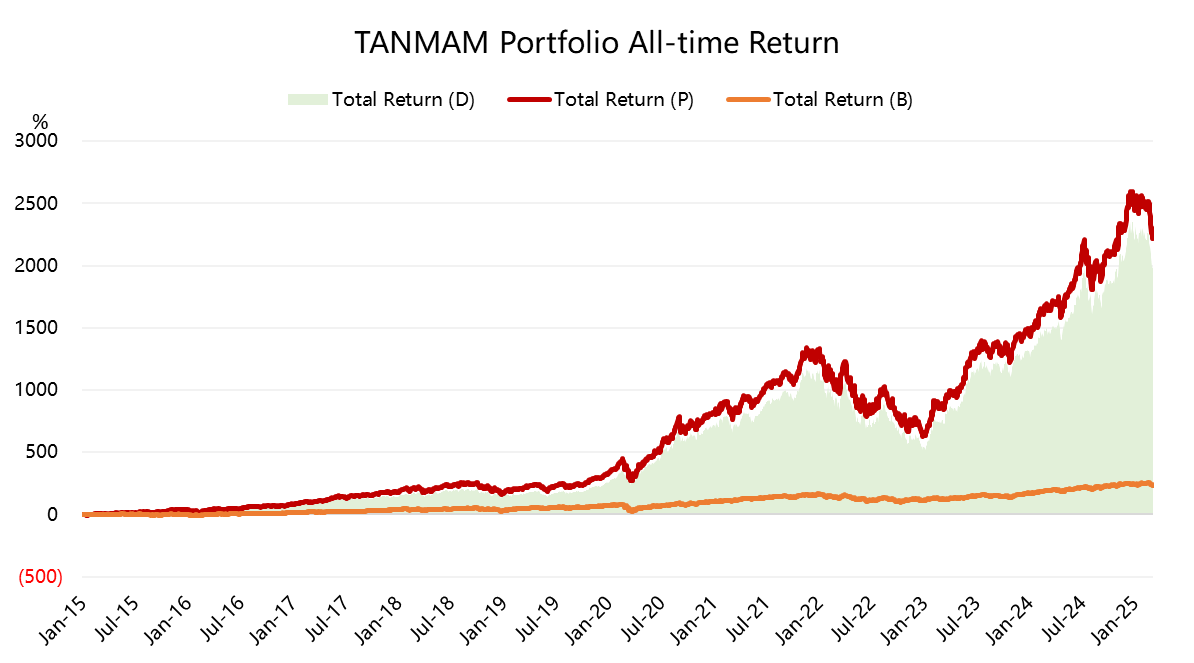

The Magnificent Seven form a portfolio (the "TANMAMG" portfolio) that is equally weighted and reweighted quarterly.The backtest results are far outperforming $S&P 500(.SPX)$ since 2015, with a total return of 2,252%, while $SPDR S&P 500 ETF Trust(SPY)$ has returned 239% over the same time period, for an excess return of 2017%.

Comments