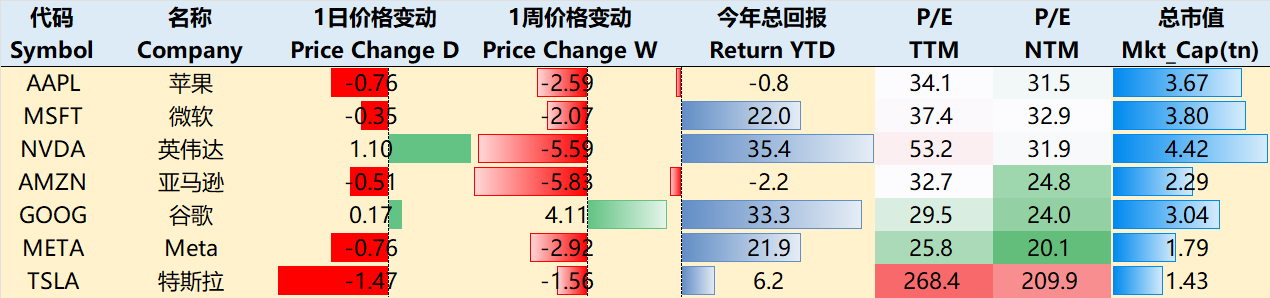

Big-Tech’s Performance

Macro Headlines This Week:

Regional banks lighting up the risk fuse again? Earnings from mid-tier players like $Zions(ZION)$ showed credit quality tanking, with bad debt rates spiking over 3%, sparking fresh panic about the whole regional banking sector. It's got echoes of the 2023 SVB meltdown, but this time the spotlight's on private credit woes—corporate defaults are climbing to 5% in this high-rate world, putting serious pressure on smaller banks' balance sheets. Add in the ISM manufacturing index unexpectedly dipping to 47.2 (way below forecasts), signaling economic slowdown vibes. Markets freaked: $Cboe Volatility Index(VIX)$ surged, gold $Gold - main 2512(GCmain)$ kept ripping higher, and $US10Y(US10Y.BOND)$ yields dipped below that psychological 4% mark.

Trade tensions heated up too. Trump doubled down on the trade war, threatening fresh tariffs on China—including extras on rare earths and port shipping. The August executive order extended the tariff truce to Nov 10, but new sanctions this week (like export controls on 19 Chinese entities) shattered the fragile peace. It's jacking up supply chain costs from semis to consumer goods, with U.S. households facing an extra ~$1,300 in tax hits on average. Wall Street's calling it the dawn of a "decoupling era," threatening global stability. Investors are sweating it'll fuel inflation and nudge the Fed toward rate cuts.

Gold hit new highs on safe-haven flows (trade wars + bank scares), Fed cut bets, and geo risks. But crypto like BTC pulled back, showing folks rotating out of risk assets. AI hype kept things afloat though— $ASML Holding NV(ASML)$ , $Taiwan Semiconductor Manufacturing(TSM)$ earnings, and $Oracle(ORCL)$ shindig reignited demand forecasts. Rate cut hopes are a tailwind for AI's capital-hungry plays, and structural tailwinds like compute shortages are propping up the sector.

Big Tech had that classic pump-and-dump vibe this week. NVDA peaked then faded; as of Oct 16 close, the past week's bloodbath: $Apple(AAPL)$ -4.94%, $Microsoft(MSFT)$ -1.23%, $NVIDIA(NVDA)$ -2.38%, $Amazon.com(AMZN)$ -1.43%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ -3.57%, $Meta Platforms, Inc.(META)$ -0.74%, $Tesla Motors(TSLA)$ -3.80%.

Big-Tech’s Key Strategy

Oracle Steals the Spotlight with Billion-Dollar Deals—What's Microsoft Thinking?

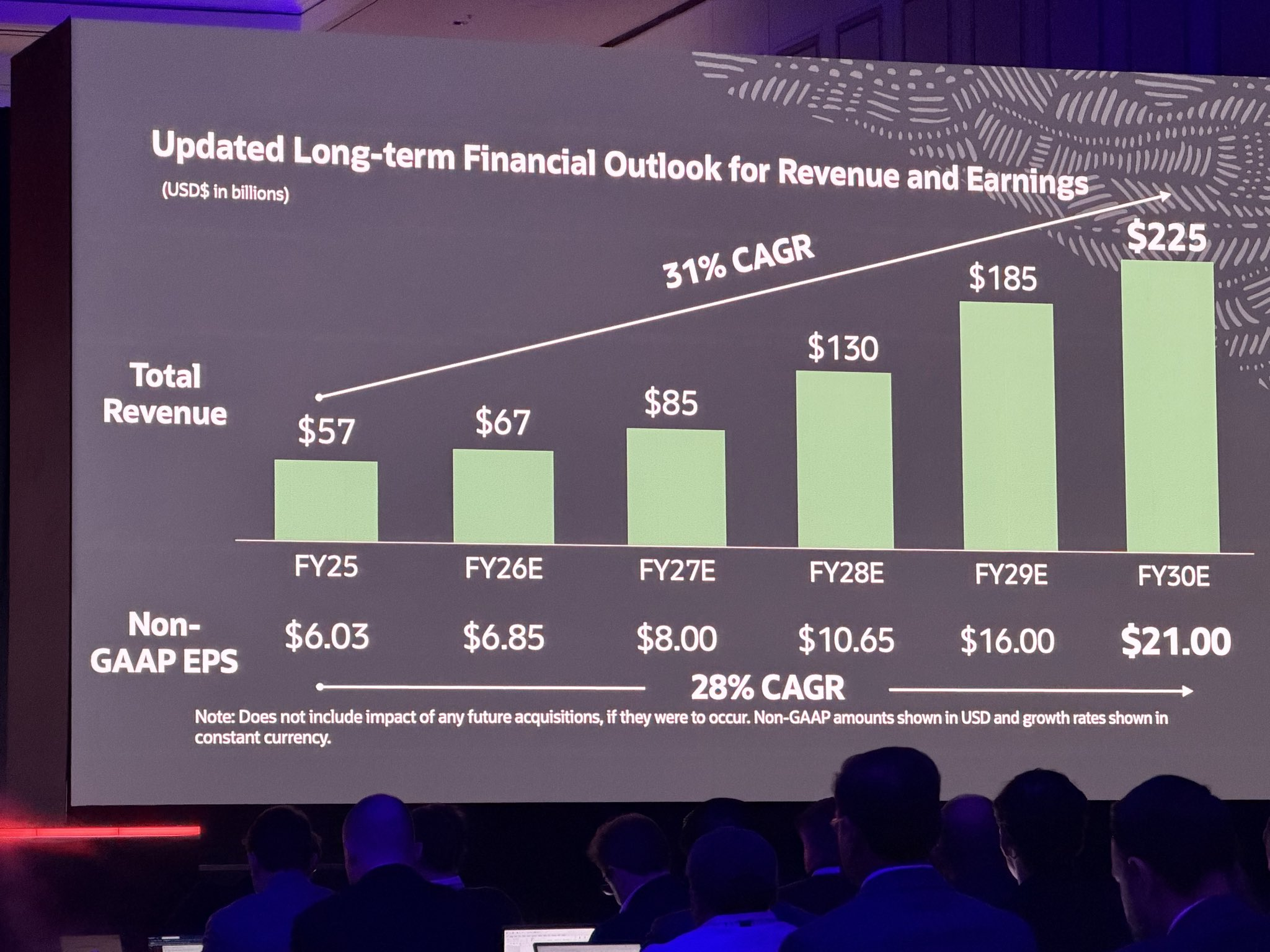

At Oracle's investor bash in Vegas, they clapped back at skeptics doubting their AI cloud infra profitability with real-deal examples, RPO/backlog numbers, and long-term revenue targets. Think a 6-year, $60B contract at ~35% gross margins—solid firepower for FY30 revenue/infra goals. Their RPO's ballooned to hundreds of billions (Q1 was already $455B), and they're inking or talking massive pacts with heavyweights like Meta and xAI. Key point: Customers aren't just OpenAI (they and the media stressed a diversified client mix to spread risk). Plus, they're branching out beyond NVIDIA with plans like AMD MI450 deploys to cut single-supplier dependency.

Short-term, it eases fears of "AI infra = money pit." But execution risks linger on costs and client concentration.

Here's the juicy angle: Why's Microsoft cool with OpenAI cozying up to Oracle?

Core #1: OpenAI's Compute Hunger is Exploding—That's the Real Driver for Partnership Shifts

OpenAI's compute needs are doubling monthly. By 2030, server spend alone could hit $450B, with plans for 250GW data center capacity by 2033 (that's a third of U.S. peak power demand today). Way beyond what one company like Microsoft can handle solo. MSFT's got its own bottlenecks—power hookups, build timelines—despite throwing cash at it. They hashed out a deal last summer to fast-track the "emergency scale-up."

Core #2: Microsoft's Triple Play in Opening the Door—Balancing Profits, Risks, and Reg Scrutiny

Dodge financial pitfalls, skip the "blind expansion" trap. Overbuilding DCs just for OpenAI could flop if AI demand wobbles—clashes with MSFT's cash-flow-first mature biz model.

Ease antitrust heat. MSFT's $13B OpenAI stake has FTC and EU sniffing around for monopoly vibes; they already ditched their board observer seat.

Lock in the golden goose. Post-deal, MSFT still gets 20% of OpenAI's revenue, a fat slice of future profits, and ~$135B in server rent from OpenAI by 2030.

Flip side: OpenAI snagged $10B from NVIDIA to build its own DCs, cutting reliance on cloud giants and dodging supply snags that could crimp R&D. That could nibble at Oracle's future revenue realization.

Can Oracle Actually Deliver?

Oracle's never tackled a 4.5GW compute project before, and DC builds are hamstrung by power, supply chains (NVIDIA's next-gen chip prices TBD). If they miss deadlines, OpenAI's AGI roadmap hits a wall.

The Wild Card on Costs?

GPUs: If Oracle's $166B OCI ambitions (plus OpenAI/other tie-ups) keep scaling, NVIDIA as prime GPU supplier scores more orders, boosting DC revenue and pricing power. A single 4.5GW ramp? That's hundreds of thousands to millions of high-end GPUs (depending on TDP and rack configs)—straight demand jolt for training chips.

DRAM/HBM/NAND: Massive DC builds supercharge HBM pull. AI/HPC shortages keep DRAM/HBM tight long-term, valuing up MU and crew. Korean giants ( $Samsung Electronics Co., Ltd.(SSNGY)$ , $SK Hynix, Inc.(HXSCF)$ ) lead in high-end DRAM/HBM fab, packaging, tech; capex ramps short/medium-term to feed the beast.

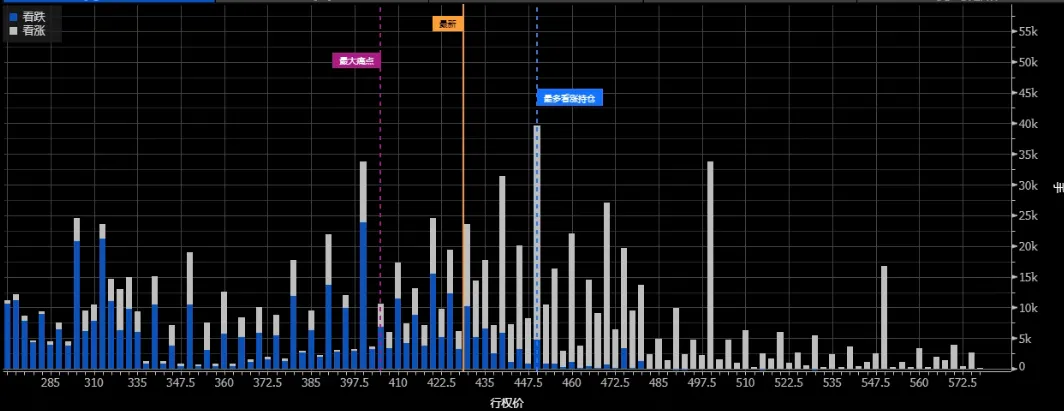

Big Tech Options Strategies

Tesla On Its Q3 Earnings Period

Standard Model 3/Y variants dropped in the U.S.—starting at $36,990 and $39,990, down 10-15% from base, but ditching goodies like panoramic roofs, ambient lights, rear screens. Slim differentiation, aimed at price hawks—expect mild sales bump, not a game-changer. Signals hardware innovation slowing, pivot to software: FSD V14 (pushed Oct 6) nails parking/lane changes, inching toward "eyes-off" smarts and unlocking Robotaxi cash flow.

Model Y L (3-row SUV) China debut could turbo U.S. (midsize SUVs = 19% market) and Europe growth.

Q3 earnings loom: Upside in high-margin segments, FSD V14 surprise, Cybertruck ramp, AI momentum—bullish vibes. But Q4 risks loom: Flat YoY revenue, post-tax credit demand fade questions.

Despite market wobbles (-1.56% for TSLA, beating the tape with low correlation), options show balanced calls/puts in 420-460 range. IV Rank ~28% (low for past year), but IV > HV hints at bigger swings ahead—watch earnings volatility.

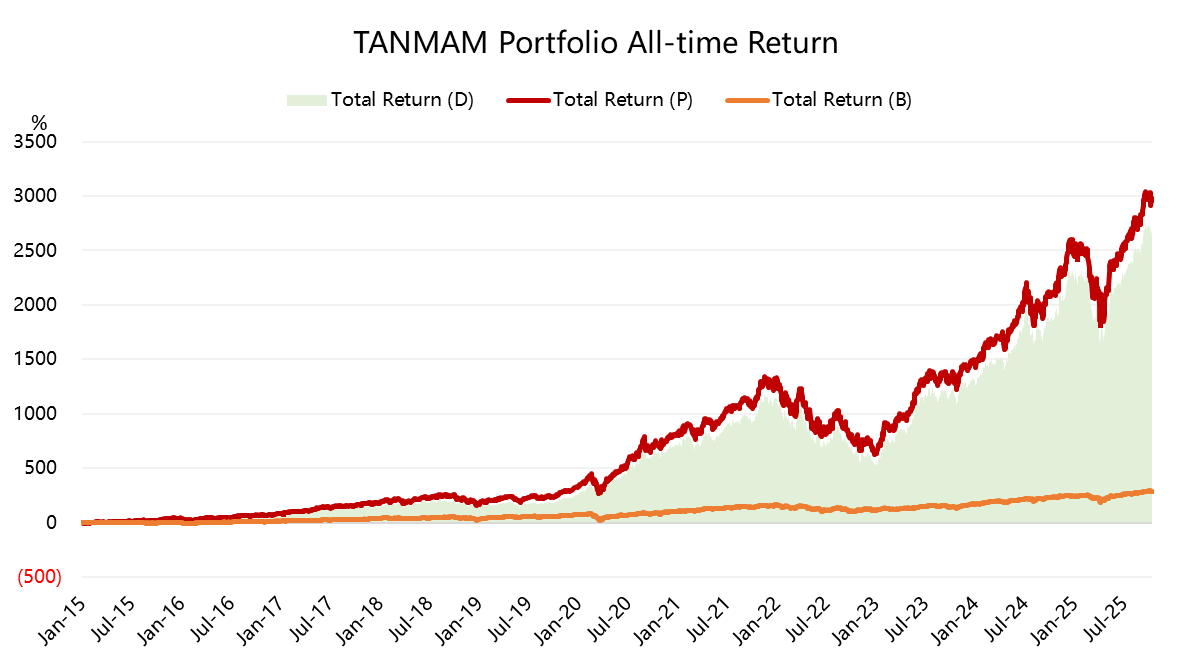

Big Tech Portfolio

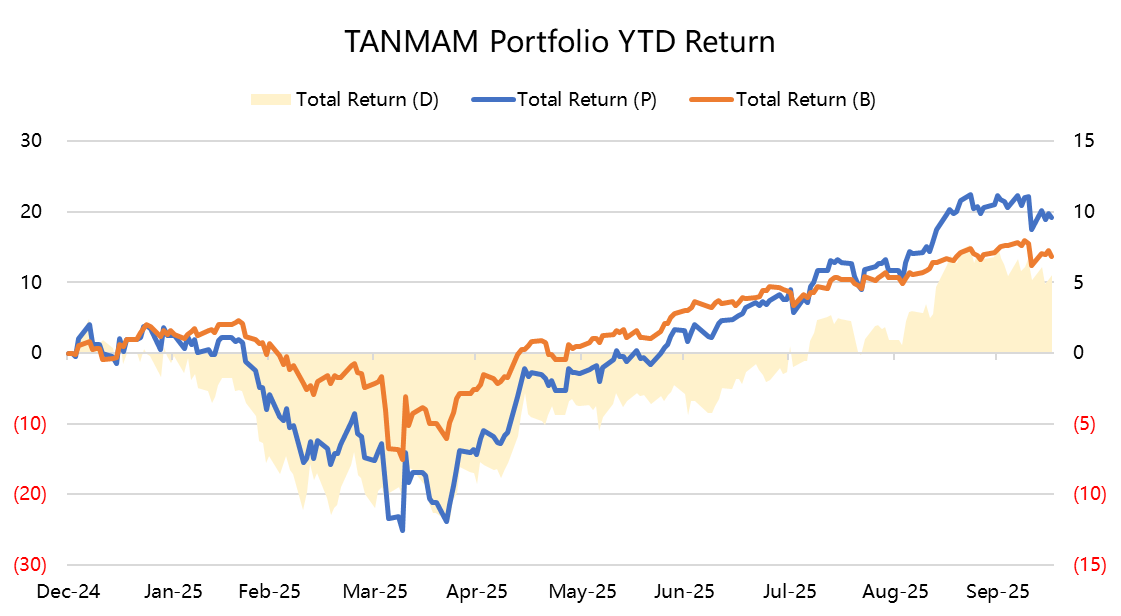

The Magnificent Seven (, AAPL, NVDA, MSFT, AMZN, META, GOOG) as an equal-weight portfolio ("TANMAMG"), rebalanced quarterly. Backtest since 2015? Crushes $S&P 500(.SPX)$ S&P 500—total return 2,959.19% vs. $SPDR S&P 500 ETF Trust(SPY)$ 's 286.47%, alpha of 2,672.72%. Still firing on all cylinders.

YTD, Big Tech's up 19.24%, topping SPY's 13.71%. Reasons to stay long?

$NASDAQ(.IXIC)$ $Invesco QQQ(QQQ)$ $NASDAQ 100(NDX)$ $ProShares UltraPro QQQ(TQQQ)$ $ProShares UltraPro Short QQQ(SQQQ)$

Comments