In the markets, the scariest three words aren't "crash"—they're "topping out." And right now, as everyone piles into $POP MART(09992)$ chasing the Labubu craze, Bernstein's fresh October 16 report is throwing ice water on the party. They slap an Underperform rating on the stock, with a HK$225 target—implying 18% downside from the October 15 close of HK$288.80.

The kicker? Their headline: "Behind the toothy grin, when will the bubble burst?" Yeah, that's the vibe. With shares dipping to HK$284 on October 17, it's a timely gut check. Labubu's feast might be winding down faster than you think.

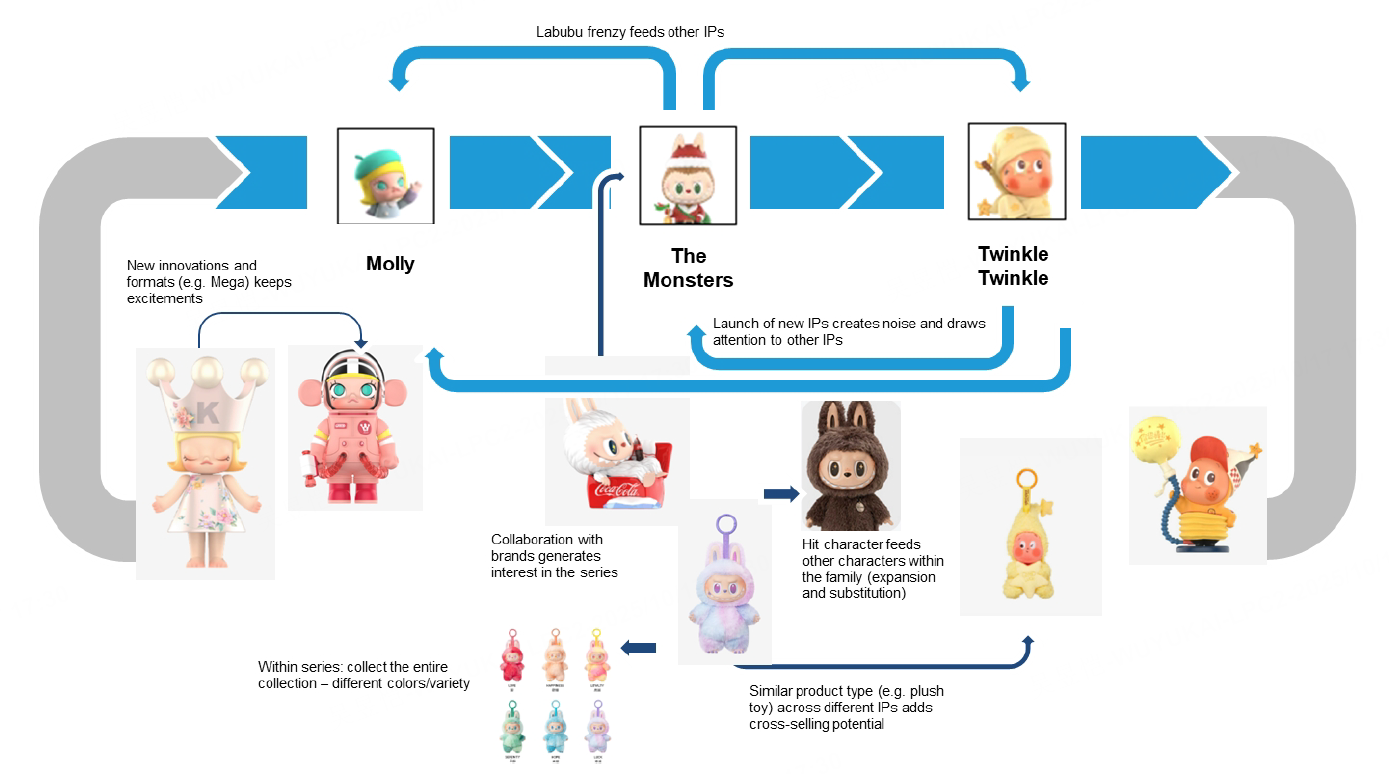

Pop Mart's story is pure magic: a niche blind-box toy exploding into a cultural icon, with secondary markets once rivaling Lego's hype. But peaks sneak up quietly. Since June 2025, Labubu's resale prices, volumes, and search buzz have all reversed hard. On China's Qiandao platform, average prices for Labubu 1.0 and 2.0 versions are down ~50% month-over-month, with rare editions cratering 70%. Over on U.S.-based StockX, "Toffee" and "Soymilk" models have shed 58% and 43%, respectively. Volumes? Even worse—daily trades on Qiandao have halved from peak levels. The scarcity premium, once fueled by hunger marketing, is getting diluted by production ramps. The crowd's exiting stage left, and the cooldown's brutal.

Digital Buzz: The Earliest Red Flag in the Virtual World

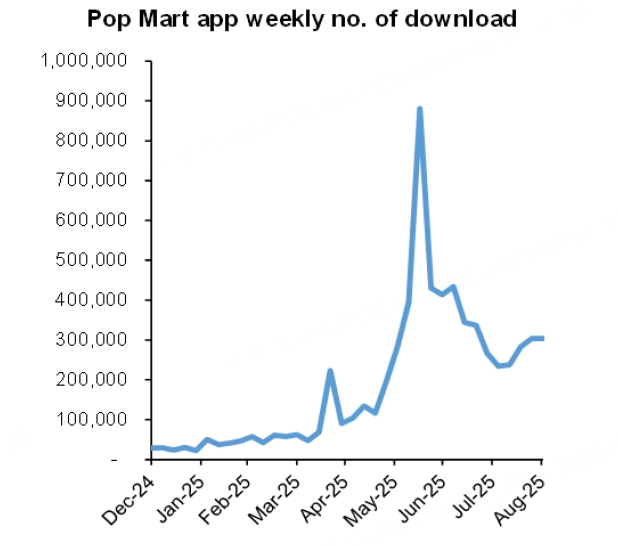

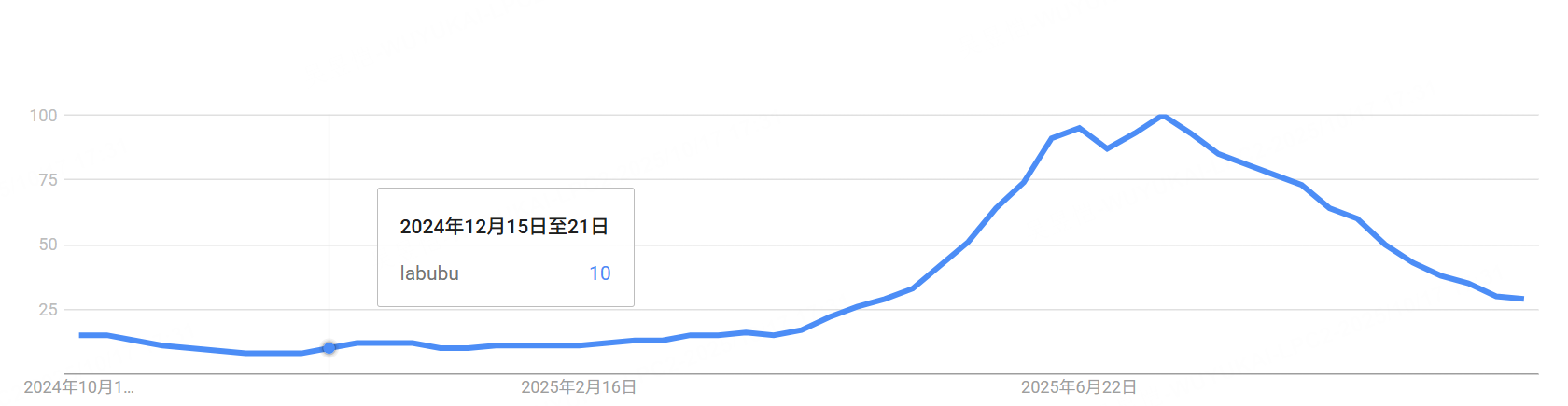

If you want to spot a company's future, start with traffic—it's the canary in the coal mine. Pop Mart's digital fire's flickering out since summer. Site visits, app downloads, and active users peaked in June and slid for four straight months. Overseas web traffic? Just 40% of Lego's, yet Pop Mart's valuation is neck-and-neck. Google Trends, Weibo, Bilibili, and Xiaohongshu searches for Labubu? Down over 80% on average since July.

[Insert placeholder for Labubu Google Trends chart here – interest spiking early 2025, then flatlining post-June.]

Traffic divergences like this often lead sales by 2-3 quarters, so Q4 could be Pop Mart's last "pretty quarter" before reality bites.

China Saturated, Overseas a Tough Sled

Domestically, store expansion's starting to trip over itself. Over 100 outlets in Tier 1 cities—saturation rivaling bubble tea chains like Heytea. Channel growth's slowing, private-domain engagement up a measly 8%, and even blind-box repurchase rates are dipping. Fakes, knockoffs, and supply bloat are eroding the brand premium fast. On Alibaba, knockoff Labubus go for pennies—how long can secondary-market faith hold?

Overseas? Growth's real, but pricey and culturally sticky. Labubu lit up Tokyo's Shibuya briefly, but the hype faded quicker than Pop Mart hoped. Cross-cultural toy narratives aren't plug-and-play; IP lifecycles here are meteoric, not evergreen.

Bernstein buckets toy cycles into three buckets:

Shooting Stars: Flash-in-the-pan fame, quick fade.

Speculative Waves: Bubbly cycles with wild swings (5-10 years)—think Beanie Babies or early Funko Pop.

Evergreens: Multi-gen icons like Lego or Hello Kitty.

Pop Mart? Textbook Speculative Wave. It rides emotional highs, but those same vibes will burn it out. "The brighter the meteor's trail, the faster the fall."

Valuation: A Bubble Stacked on Dreams

Let's break down the core assumptions driving this:

Market Consensus | Bernstein Forecast | Variance | |

2026 Revenue | RMB 456B | RMB 418B | -8% |

2027 EPS | RMB 14.8 | RMB 12.2 | -17% |

Current MCap | USD 49B | Fair Value USD 40B | -18% |

If growth holds, Pop Mart hits a $63B market cap by 2027—topping Lego's private valuation. But to justify that? They'd need to sling 150M Labubus annually. That's every third person aged 15-40 globally buying one. We're talking peak faith density—physically impossible long-term.

At 29.8x 2025 EV/EBITDA, Pop Mart trades above China peers like Miniso (18.5x) but below IP titans like Netflix (44.7x) or Sanrio (44.8x). PEG at 0.7x on 34% 2025-27 EPS CAGR looks cheap, but Chinese consumer P/Es hug growth tight (see Exhibit 3 correlation). IP tiers vary: gaming at 3.0-3.5x PEG, toys sub-1.0x.

Bernstein pegs 1x PEG (18x NTM+1), nodding to blind-box edges over vanilla toys but discounting unproven evergreen IP builds and single-IP risks. Why? Pop Mart values like a durable brand without the history—Hasbro (15.0x) or Mattel (11.1x) boast steadier ROEs (projected 76% and 1% for 2025 vs. Pop Mart's Labubu-boosted 255%).

Scenario Breakdown: Upside Capped, Downside Brutal

Risk asymmetry screams "sell": modest gains, massive pain.

Base Case (-18% downside): 31%/21% revenue growth in 2026/27, margins easing to 32% (still 8% above 2024), 18x multiple = HK$225 target.

Bear Case (-58% downside): Growth stalls at 15%, margins revert to 2024 levels, 15x multiple = HK$114.

Bull Case (+11% upside): Beats at 38%/24% growth, holds 34% margins, 20x expansion = HK$303.

Upside's razor-thin at 11%, but downside? A vicious loop if Labubu peaks in 2026/27: sales slump, margins crush, secondary markets tank.

Recent X chatter echoes the fade—posts since October 1 mix fan swaps, giveaways, and "next big thing" speculation like Jellycat. No viral frenzy; just resale noise and quiet longing. Secondary prices keep sliding—rare Labubus now ~840 yuan on Qiandao, down from 10,000 yuan highs; mini sets at 105 yuan, off 24% from peaks. Pop Mart even welcomes the drop—it juices primary demand.

Pop Mart's an aesthetic bubble tale: it tapped young loneliness, birthing an anthropomorphic emotional spend. But emotion-fueled models all share a fate—when attention wanes, the growth myth crumbles. Bernstein's right: take profits now, before the grin fades. Longs, trim or hedge; shorts, eye that earnings miss. At HK$284, the top's in sight.

Comments