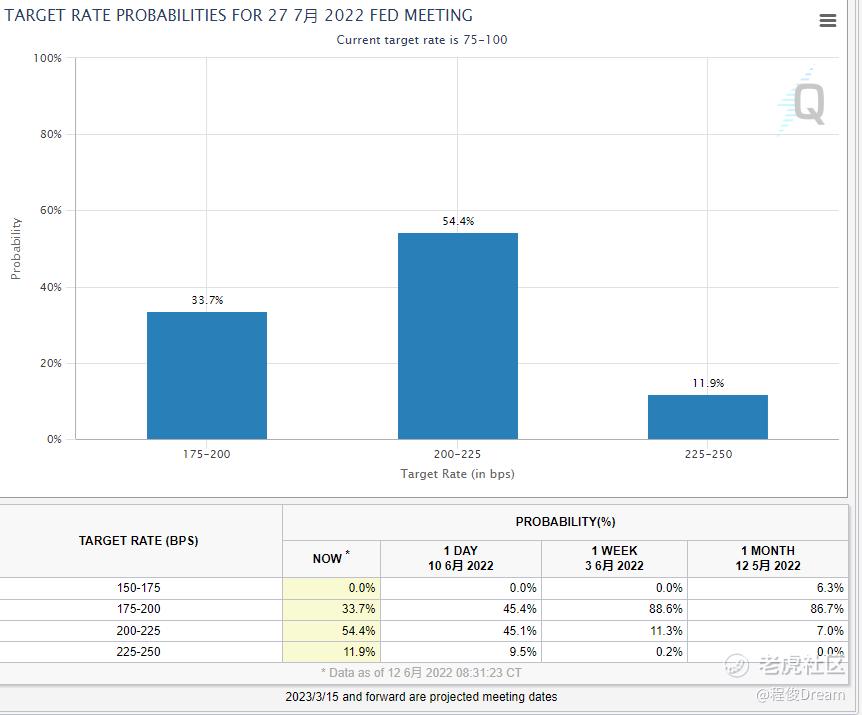

After the latest January inflation data was released and hit a new high, the market had new expectations for the Fed's actions. According to the latest Fedwatch data, the probability of FOMC in July has been 50-50. In this week's expectation, although there are some variables, the probability of 50 basis points is obviously superior.

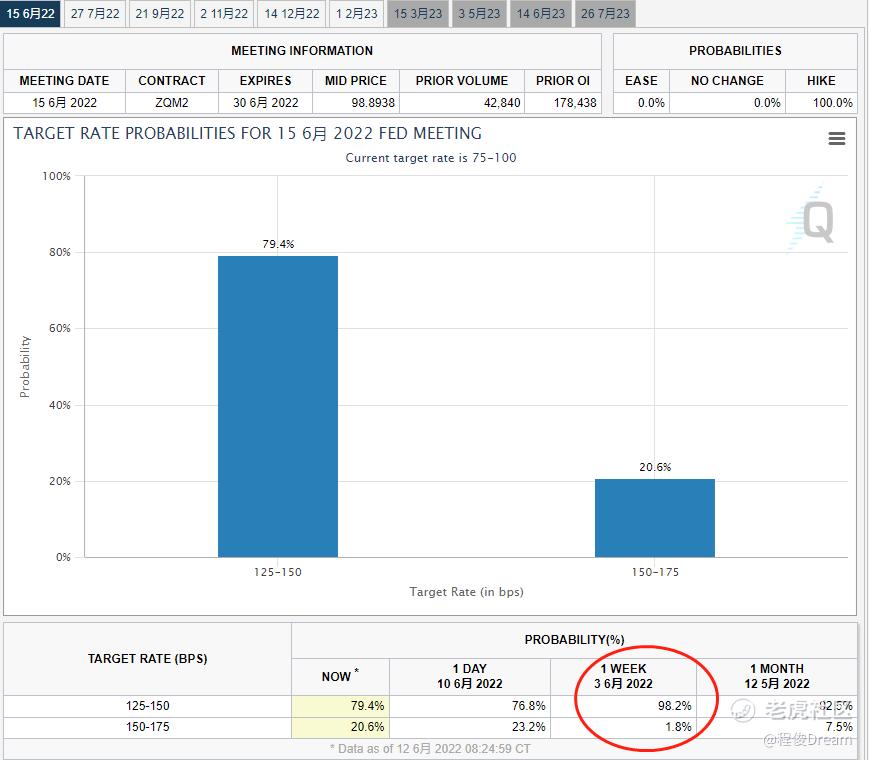

Data show that the probability of raising interest rates by 50 basis points on June 15th is close to 80%. Although this figure has dropped significantly compared with 98.2% a week ago, as we said before, it is still relatively stable when it exceeds 70%. In contrast, July's data, which also overwhelmingly raised interest rates by 50 basis points a week ago, is now seriously divided. Even the probability of raising interest rates by 75 basis points has reached half.

Judging from the data, there is still a greater possibility that the Fed will not take the initiative to make the market more turbulent this week. At the same time, we can also take this opportunity to fully communicate with the market again.

If the inflation data of next month still can't stop, then we will really start work in July.It should be noted that FedWatch data is changing, and there are still about 2 days before FOMC. You can pay close attention to the data situation. If the probability of 50 basis points is less than 70%, you should be careful.

From the market point of view, panic seems to have begun to appear. S&P has fallen vertically in the past three trading days, and its weekly line is almost bald and not far from the low of 3800. The low point in May is technically crucial, and setting a new low every other month will mean that the market will start a new round of decline. Combined with other risky assets, such as the recent stormy ETH, the risk-off atmosphere has a "liquidation" intention.

Last Friday, gold showed a trend of first suppressing and then rising, which was obviously stronger than silver. Many investors don't quite understand why gold will rise when the interest rate hike may be even greater.

First of all, as far as inflation itself is concerned, it is a neutral factor for gold, and there is no clear positive and negative correlation between them in history. Secondly, on the issue of interest rates, there have been signs of decoupling between US bond yields and gold performance since the beginning of last year.Higher nominal/real interest rates are of course not conducive to interest-free asset gold in theory, but don't forget that gold still has a safe haven aura. When gold and US dollar index run in the same direction, gold will remain strong with high probability.

At present, the price of gold still fluctuates in a relatively middle range, and last week's counterattack cannot declare that the bulls have won in an all-round way. It is expected that the market will try to build a rebound high point first, and then break again before confirming its strength. If the low level in May is broken down, we should change our thinking, and gold may turn to bear.

Crude oil has also begun to show a correction in recent trading days, so it is still necessary to observe the performance of oil prices and US stocks. The rise in crude oil and the fall in US stocks mean that the economic crisis will follow; Crude oil pullback US stock rebound hints at revised respite time; Both of them run in the same direction, no matter whether they rise or fall, they are in line with the correlation of most times. In addition, considering the actual situation in the United States, if the oil price continues to be high, I believe they will take some actions/measures.

$NQmain(NQmain)$ $YMmain(YMmain)$ $ESmain(ESmain)$ $GCmain(GCmain)$ $CLmain(CLmain)$

Comments