Forex reflects the strength of economic activities, but short-term fluctuations are event-driven, especially when investors have consistent expectations

Chinese Yuan began to strengthen at the end of November. The exchange rate of US dollar against offshore RMB once again returned to below "7" after three months, and once rose above 6.95. $HKEX USD/CNH - main 2212(CNHmain)$ $HKEX USD/CNH - main 2212(CNHmain)$

Reasons for rapid appreciation

First, the reopening promotion of China's domestic economic recovery.In November, the Chinese government introduced a series of measures to stabilize growth, including 20 measures to optimize epidemic prevention and control. In December, all localities have been closer to the optimized plan at the implementation level. All these make the market expect that the consumption and investment demand of China's economy will be strongly boosted next year.

On December 7th, New Explanation of Joint Prevention and Control Mechanism of the State Council Asymptomatic persons and mild cases with home isolation conditions are generally isolated at home.

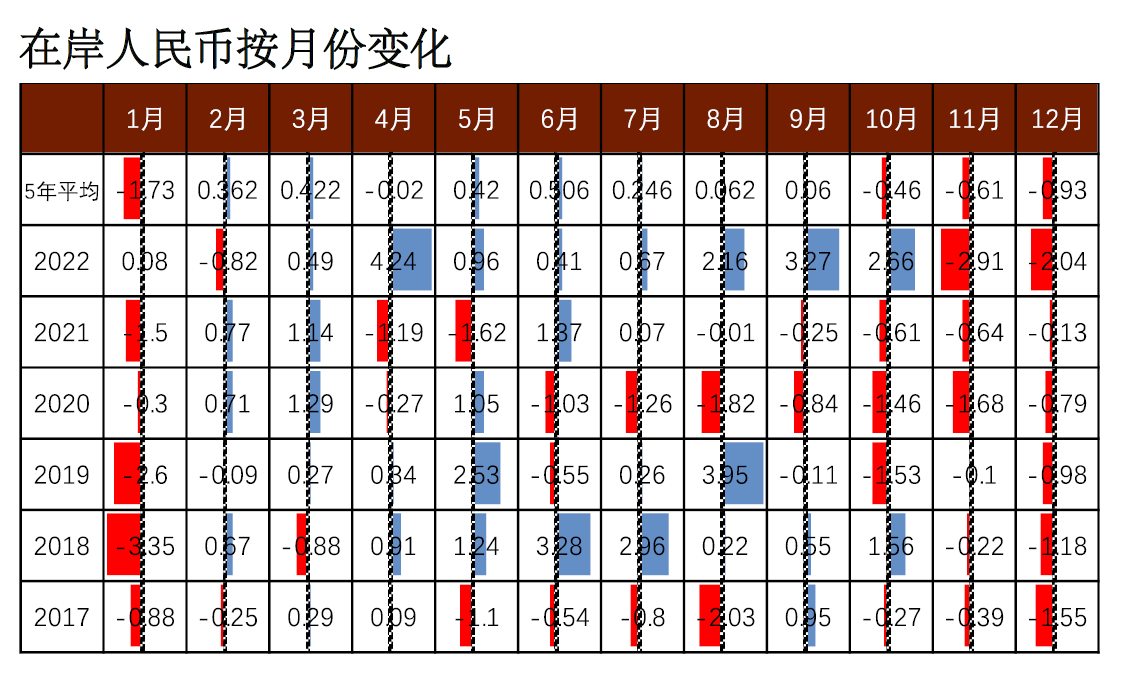

Second, seasonal effect.November and December are seasonally favorable months for the RMB exchange rate. Since 2017, the RMB exchange rate against the US dollar has strengthened in November and December, because both import and export settlement and individual settlement years ago will take this opportunity to complete.

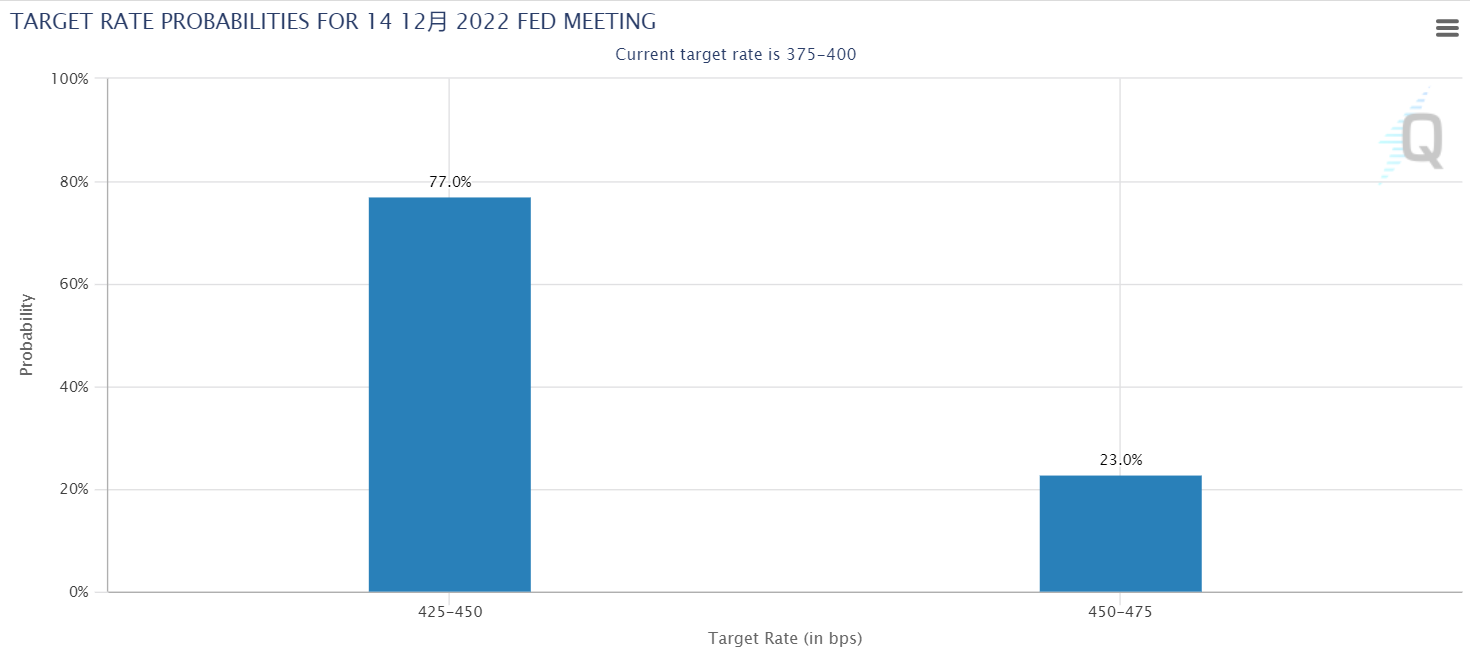

Third, the US dollar index fell, and the Fed's expectation of raising interest rates declined.The US dollar index has halved its gains this year, and Federal Reserve Chairman Powell also said in his recent speech that it is appropriate to slow down the rate hike. This gives the market a greater expectation of "slowing down interest rate hikes". According to the CME Monetary Policy Watch tool, the probability of raising interest rates by 75 basis points in December is 77%

The expectation of further decline of the US dollar will continue to be reflected, and non-US dollar monetary assets are likely to be improved.

To sum up, will the RMB still be strong in December?

1. The risk preference of foreign capital for Chinese assets has returned again. According to Bloomberg data, the total net inflow of northbound funds in November was about 60 billion yuan, which was the second largest net inflow in a single month this year. In December, it still maintained the momentum of backflow. The return of northbound capital also represents an increase in demand for RMB.

2. According to the historical trend, the seasonal influence is still great.In the first 10 months of this year, China's accumulated trade surplus in goods and services was 494.5 billion US dollars (Bureau of Statistics), while the surplus of bank current account settlement and sales of foreign exchange on behalf of customers was only 127.6 billion US dollars, with a difference of about 366.9 billion US dollars between the two, which was 2015.The second highest level in the same period. The existence of these balances represents that traders may have some behaviors of delaying foreign exchange settlement, and the time point of trade payment may be more concentrated at the end of the year.

3. Strong Macroeconomic booming expectation.Previously, the excessive depreciation factor included in RMB was a concern about the uncertainty of economic environment. At present, this sentiment has been alleviated, and it is just around the corner that economic activities will fully return to normal. At the same time, the market's risk aversion to Europe, America and other places is heating up, because their economies still have a high probability of recession next year, and the funds of emerging markets may need to find an investment export.

Therefore, in the short term, RMB is still promising before the end of the year.

In the medium term, it still depends on the monetary policy shift (and rhythm) of the Federal Reserve and other central banks around the world. It is highly probable that China will still maintain a loose pace next year.

$HSI(HSI)$ $HSTECH(HSTECH)$ $HSCEI(HSCEI)$ $China A50 Index - main 2212(CNmain)$

Comments