Since early August, a new round of depreciation of the Japanese yen against the US dollar has appeared again. On September 6th, the US dollar once broke through the 140-point mark against the Japanese yen.

The author believes that the current depreciation of the yen is the result of resonance of many factors: the Fed's monetary tightening brings international capital outflow, Japan's economic growth is weak, the Bank of Japan maintains loose monetary policy against the trend, the rising cost of energy imports leads to the convergence of trade surplus, and the rebound of Japanese inflation makes it difficult to continue the yen carry trade.

Japan's capital outflow caused by Fed tightening

From the economic data, although the American job market has experienced moderate weakness, from the historical experience,The trend of American inflation indicators is the key to the Fed's monetary policy.At the Jackson Hole Global Central Bank Annual Meeting, The key message that Powell's speech can convey more than the minutes of the meeting is that, It is allowed to curb inflation at the expense of appropriate economic slowdown, especially to match supply and demand by cooling demand, because the current high inflation in the United States is indeed the product of strong demand and limited supply, and the tools of the Federal Reserve mainly play a role in aggregate demand. Therefore, we believe that the Fed will continue to allow the US bond yield curve to be upside down.

In the job market, the number of non-farm payrolls in the United States increased by 315,000 in August. Although the U.S. job market shows signs of slowing down, the number of new non-agricultural jobs and wage increases have declined, and the rising unemployment rate has increased recession concerns, the number of job vacancies is still at a historically high level, the labor market tension is still high, and the high growth rate of hourly wages may still be difficult to alleviate.

The CPI data in August will provide more influential guidance. From the current global energy, food and non-agricultural wage growth in the United States, the wage-inflation spiral and residents' energy costs will support the CPI in the United States, and the growth rate may only decline moderately. From the historical experience, the Fed will slow down the pace of raising interest rates unless the year-on-year growth rate of CPI in the United States returns to the range of 3%-4%. According to FedWatch, an interest rate observation tool of Chicago Mercantile Exchange, on September 6th, the market predicted that the probability of the Federal Reserve raising interest rates by 75 basis points in September was 66%, slightly lower than the 73% a week ago.

Due to the differentiation of monetary policies between the United States and Japan, the spread of national debt between the United States and Japan continues to widen. Take the spread of 10-year treasury bonds as an example. Before the Federal Reserve raised interest rates in March, the spread of US and Japanese treasury bonds was below 200 basis points, and on September 6, the spread between the two expanded to about 295 basis points. If the Bank of Japan maintains its current monetary policy unchanged, the spread between US and Japanese government bonds will probably further widen, which will lead to the outflow of international capital from Japan and aggravate the pressure of yen depreciation.

Downward pressure on Japan's economy may exceed that of the United States

Economic fundamentals determine the long-term trend of the exchange rate of Japanese yen against US dollar. From the perspective of Japan's long-term growth driving force, factors such as aging population and declining labor productivity all restrict Japan's economic growth. The potential growth rate of Japan's economy is very low, and there is actually little room for repairing the output gap.

From the perspective of short-term and medium-term factors, on the one hand, the Japanese government exerts too much strength in fiscal policy and monetary policy, and the space for exerting strength is limited. The expansion of Japanese public sector debt makes the effect of Japanese fiscal stimulus marginally diminish; On the other hand, the rising energy price leads to the continuous convergence of Japan's trade surplus, which to a great extent leads to the weakening of the boosting effect of the depreciation of the yen on Japan's exports. The Japanese government lowered its GDP growth forecast for fiscal year 2022-2023 from 3.2% in January to 2%, and the GDP growth forecast for the next fiscal year starting from April 2023 is 1.1%.

With high energy costs, Japan's manufacturing industry is under great pressure. According to the relevant survey released by the Bank of Japan, in the second quarter of 2022, the confidence index of large Japanese manufacturing enterprises continued to decline, and the decline rate was larger than before. At the same time, the increase in the number of bankruptcies of Japanese enterprises will also adversely affect the economic recovery. According to a report from the Tokyo Chamber of Commerce and Industry Survey, in the first half of 2022, the number of bankruptcies of Japanese enterprises reached 3,060, a year-on-year increase of 0.52%.

From the perspective of consumption, although private sector consumption played a pulling role in Japan's GDP growth in the second quarter, with the rise of prices in July, residents' consumption expenditure began to decline. Data show that Japanese household expenditure increased by 3.4% year-on-year in July, which is slower than the 3.5% growth in June. Compared with June, household expenditure in July decreased by 1.4% month-on-month, which exceeded market expectations. Because global commodity inflation and a weak yen have pushed up the cost of imported goods.

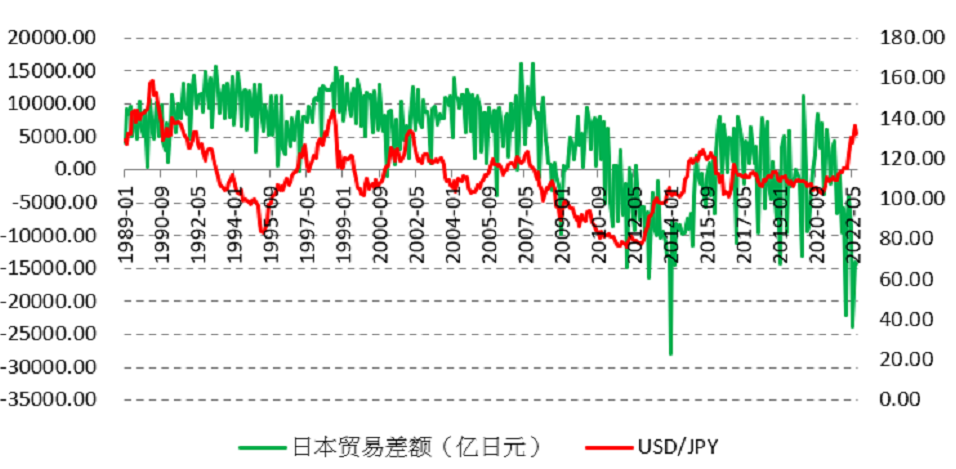

The narrowing of the balance of payments also depresses the yen

The trend of a country's exchange rate is caused by many factors, among which the balance of payments has a very direct impact on the exchange rate. As a resource-deficient country, Japan's energy is heavily dependent on imports. The soaring global prices of energy and raw materials have caused Japan's import costs to rise sharply. Coupled with the impact of falling external demand, Japan's international trade gap continues to be negative, was-140 million yen in July and reached-240 million yen in May.

According to common sense, the depreciation of local currency is beneficial to exports, but for net resource importers, the depreciation of Japanese yen is more likely to worsen their balance of payments, because the sharp rise in international energy prices leads to the growth rate of imports exceeding the growth rate of exports caused by exchange rate depreciation. The energy crisis may not only impact the European economy, but also drag down Japan. The shale oil revolution in the United States from 2016 to 2017 has brought energy independence, which means that the impact of rising energy prices on the United States is far less than that of Japan.

Although Japan and the United States have jointly intervened in the exchange rate in history, such as the Asian gold in 1998Financial crisis, but under the current macro environment, the United States is unlikely to intervene in the exchange rate. At present, the United States is committed to fighting inflation, and it is unable to intervene in energy prices, and it is difficult to achieve good results in intervening in international capital flows. Therefore, judging from various factors, the depreciation of the yen may not be over yet.

$E-mini Nasdaq 100 - main 2209(NQmain)$ $E-mini S&P 500 - main 2209(ESmain)$ $E-mini Dow Jones - main 2209(YMmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2210(CLmain)$

Comments