After the Jackson Hole annual meeting and non-farm payrolls data were released, market expectations did not change.

But what many may not have noticed is that a riskier event than the annual central bank meeting is quietly brewing-- A storm of central bank rate hikes sweeping the world. And this biggest risk of the week will gradually change the course of global stock markets starting Tuesday.

And the center of the storm is the European Central Bank rate meeting to be announced this Thursday.

Before that, the central banks of Canada, Australia, Chile and other countries will also announce the results of their interest rate meetings this week. At least five major economies will be involved in the biggest interest rate hike storm across Asia and Europe in the coming week.

US Treasury yields, the pricing basis for global assets, have been climbing in the last two weeks, creating insurmountable short-term pressure on US stocks and global equity indices.

Will the wave of global rate hikes make stocks worse? Of course.

The starting point for this week's rate hike storm is the Federal Reserve. In the first two weeks, Powell dispelled market expectations of a rate cut early next year and reconfirmed lower inflation as the Fed's focus.

More central banks will be forced to choose to follow the market trend and raise interest rates for fear that the spread between interest rates and US treasury will widen too much and lead to foreign capital outflows.

1. Global Interest Rate Hike Wave This Week

(1) Australia

The Reserve Bank of Australia may choose to raise interest rates again on Tuesday by 0.5 percentage points, which will impose more interest burden on the country's household account liabilities.

Australia is already one of the world's largest countries in terms of total household debt as a percentage of GDP.

(2) Asia

Malaysia's central bank is scheduled to introduce interest rates on Thursday, with Bloomberg forecasting a 25 basis point increase.

(3) South America

Chile's central bank is also expected to extend its record tightening cycle, raising its key interest rate for the 10th consecutive time to at least more than 1,000 basis points.

Peru, which will likely raise its benchmark rate by 0.5 percentage points to 7% on Sept. 8

(4) Europe

The ECB will raise rates on Thursday. There is no unified expectation of an ECB rate hike, which makes the ECB meeting a more important risk event than last week's non-farm payrolls or even the annual Jackson meeting.

Other European countries, such as the Danish central bank, will also follow the ECB rate hike this week, and Poland and Serbia will also decide to raise the benchmark market rate at the same time.

We expect the probability of Thursday's rate hike to be 75 bps. 50 bps is less likely; 25 bps or 0 bps is impossible.

2. Challenges faced by Chairman Lagarde

Why ECB should raise interest rates sharply? Let's look at the challenges currently faced by Chairman Lagarde.

1) Weak euro

The euro fell again by 0.7 percentage points at the opening of trading this Monday.

As of now, the euro has fallen to its lowest position against the dollar since 2002. And the Euro 50 index also fell 3.3 percentage points after the opening bell.

We do not yet see any signs of a reversal.

2)Energy crisis

The energy crisis in Europe may have reached an unprecedented level of severity with Russia shutting down the Nord Stream pipeline of natural gas into Europe.

Russia is using natural gas as its energy weapon - using inflation as a bargaining chip to gain more political balance.

Although Europe has taken some measures to control gas prices, short-term sentiment will not change the long-term trend.

Unless Russia backs down, there is no solution to imported inflation in Europe.

The continued deterioration of the trade balance will continue to undermine the flow of funds to European currencies. Soaring treasuary yields will also continue to reduce the discounted value of future corporate cash flows, which will trigger another round of stock market declines.

Goldman Sachs' strategy team believes that if Russia cuts gas flows further and longer, the euro is likely to fall to $0.95 in the coming months.

3) Less support from US

As the crisis in Europe deepens, the relationship between the European and American alliances is becoming more delicate.

- If the US sacrifices its energy reserves to balance the energy inflation in Europe, it will inevitably increase the Fed's difficulty in lowering inflation while maintaining a stable economy;

- if let European inflation uncheck, the US will face a recession in the European market.

But otherwise, it seems to be good for the United States.

When a recession is approaching, US treasury is more anti-inflation than European treasury. More companies and foreign capital will also return to the US.

Fed's upcoming tapering in September will cap the amount twice as much as before, and trillions of assets are about to be sold off by the Fed, so overseas buying of US treasury becomes critical.

So a fire in Freeport blocked US gas exports to Europe and so far we haven't seen any signs of recovery. The natural gas price differential between Europe and the US is being widened.

4) Energy crisis is turning into a political crisis

The Czech Republic can no longer stand the high gas prices and more than 100,000 people have taken to the streets and started marching!

In Argentina, South America, Vice President Cristina was shot in the head by a robber last week, but survived the gun jamming.

This may just be the beginning of a democratic crisis.

5) conclusion

So the dilemma in the face of Lagarde is more difficult than Powell.

It will be difficult to put restrictive pressure on prices without adding 75 basis points, and prices may rise even more in the future;

if ECB increased 75 basis points, higher European treasury yields will damage the present value of future corporate cash flows over a longer cycle, reducing economic dynamism and triggering a recession.

3. More Risks For Overseas Market

(1) High inflation

After Turkey cut interest rates against the trend, prices appeared almost hyperinflationary in degree.

At a time when prices are soaring across the board, almost no country dares to let loose against the tide of easing. Look at Colombia, Mexico and Brazil's price index trend:

(2) Collapse of fixed assets

And more frightening than the rate hike is the precursor to the collapse of fixed asset prices. The news has already reported on weakening U.S. home prices, but you may not know that Sweden is on the verge of a bottom-breaking collapse:

So it may be easier for us to understand from this point why the overseas debt market, which is now dominated by mortgage bonds, is so critical.

(3) Will the pressure on US treasury continue to increase in the near term? Most likely

The 2-year US treasury real yield (excluding inflation) has jumped to a two-year high, while the 5-year and 10-year real yields have also reached multi-year highs. U.S. bond yields are not under pressure at all as the ECB meeting approaches.

Since the Jackson meeting, US 10y and 5y real rates have risen about 30 and 38 basis points, respectively, while the tech-dominated $NASDAQ 100(NDX)$ has plunged 8%.

In the short term the only thing likely to provide pressure on surging US treasury yields is the ECB rate meeting, with the euro almost the biggest counterparty to the dollar.

(4) Hedge funds remain bearish

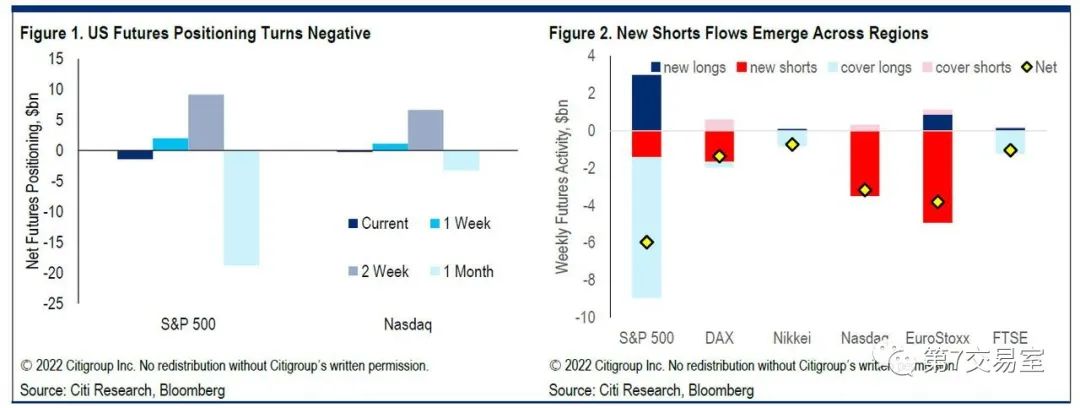

However, looking at the current movement of institutional money in futures positions, bearishness still prevails.

Net notional futures positions reversed in the most recent week, with the S&P 500 position falling to -$1.4 billion; Nasdaq futures fell less notionally (-$200 million), but both are now negative on a normalized basis.

The net notional futures position in the S&P 500 fell by nearly $3.5 billion, primarily due to a large number of long closures ($7.5 billion), while short flows in the Nasdaq increased moderately.

Bottom Line

The greater the likelihood of recession, the higher the future investment value of treasury.

In order to attract the global flow of hot money, the ECB will choose to reduce the spread between Europe and the US treasury interest rate.

But if the ECB chooses a 75 basis point rate hike, will the Fed will respond with a more hawkish measures?

What do you think of the U. stock market performance this week?

Share your thoughts in the comment section~

$E-mini Nasdaq 100 - main 2209(NQmain)$ $E-mini Dow Jones - main 2209(YMmain)$ $E-mini S&P 500 - main 2209(ESmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2210(CLmain)$

Comments