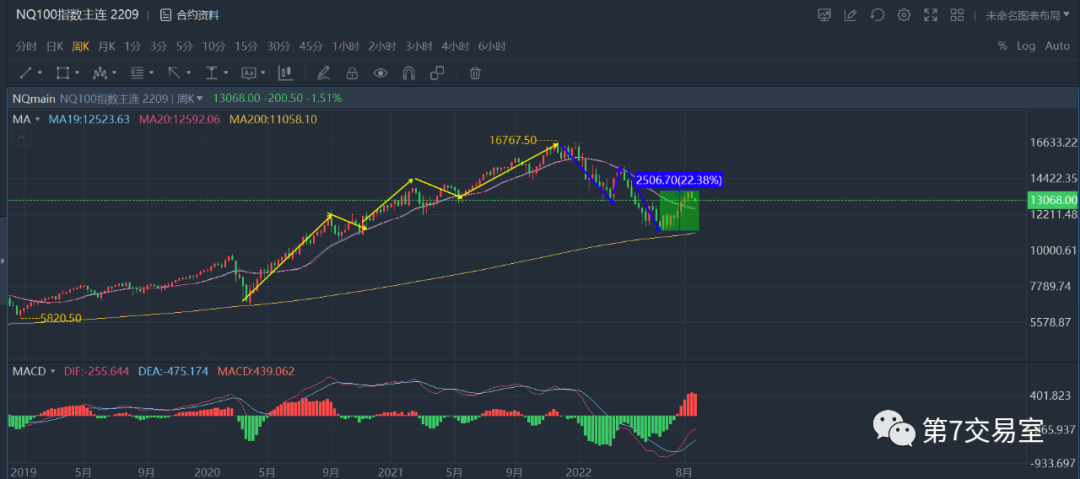

With the daily K of Nasdaq futures completely falling below the 20-day moving average, the bear market rebound, which started in mid-June and exceeded 20%, finally came to an end.

From the medium-term K-line chart, the Nasdaq weekly line has gone out of a typical Eliot 8-wave cycle.

So what's next?

The retracement of US stocks may have just begun, and with a high probability, there will be a bottoming time lasting for several weeks. However, it is difficult to refresh the previous low of the Nasdaq in June,

All the reversals began in the bond market

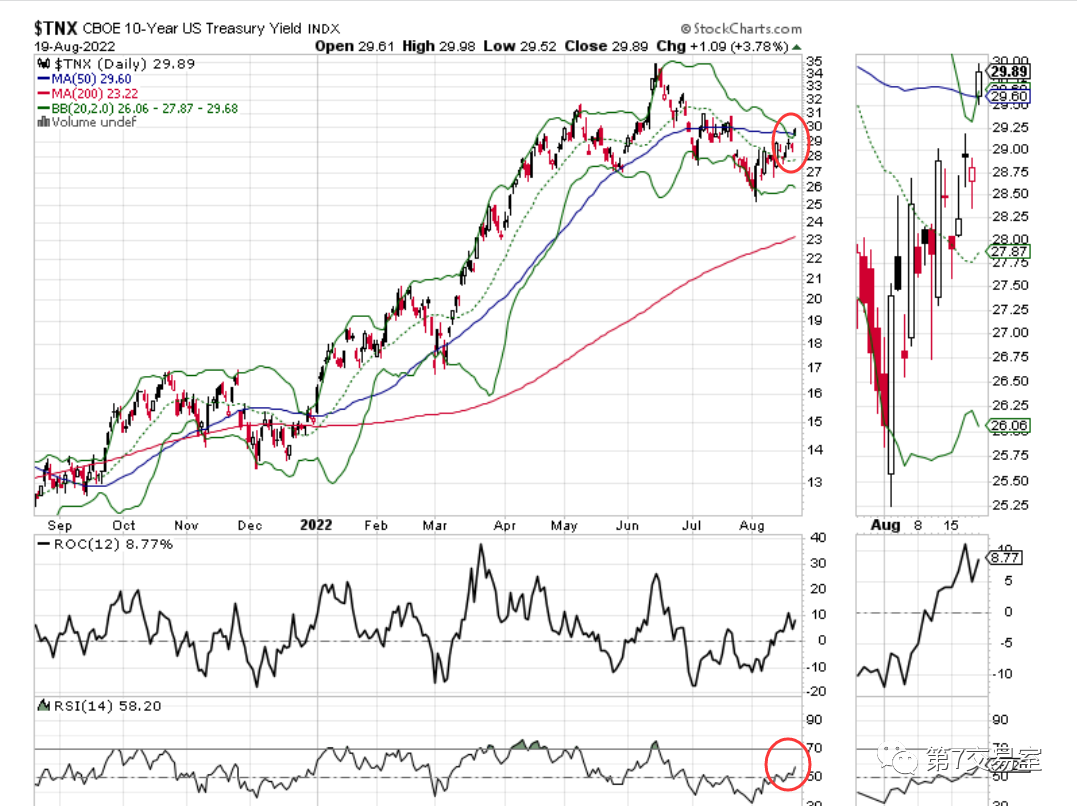

I don't know if you have noticed it. Just last week, when the US stock market came out of the peak reversal, the yield of the bond market has quietly risen continuously for more than a week. Even after the CPI showed signs of peaking, the probability of the Fed raising interest rates dropped sharply, which did not affect the trend

10-year US bond yields have risen sharply:

In the past 10 years, the yield of US bond has risen above the 50-day moving average, the RSI index has broken the position strongly, and the upward trend of the market is very strong.

In the past two years, the yield of US bonds also broke through the previous consolidation range, trying to test the high level of 3.2%.

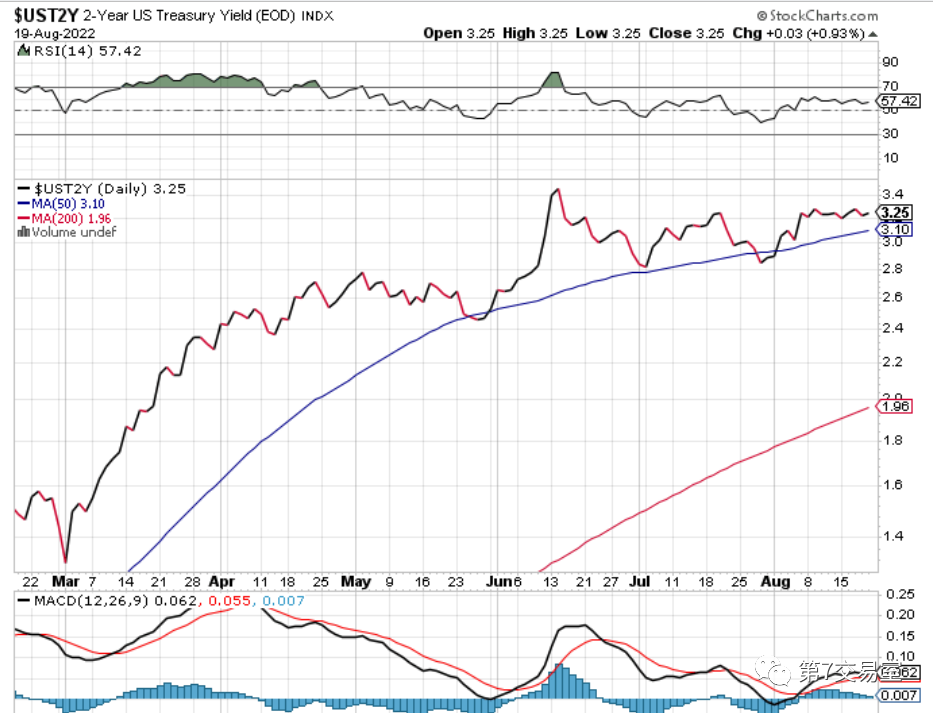

With the rise of US bond yields, the US dollar index also quickly bottomed out and rebounded

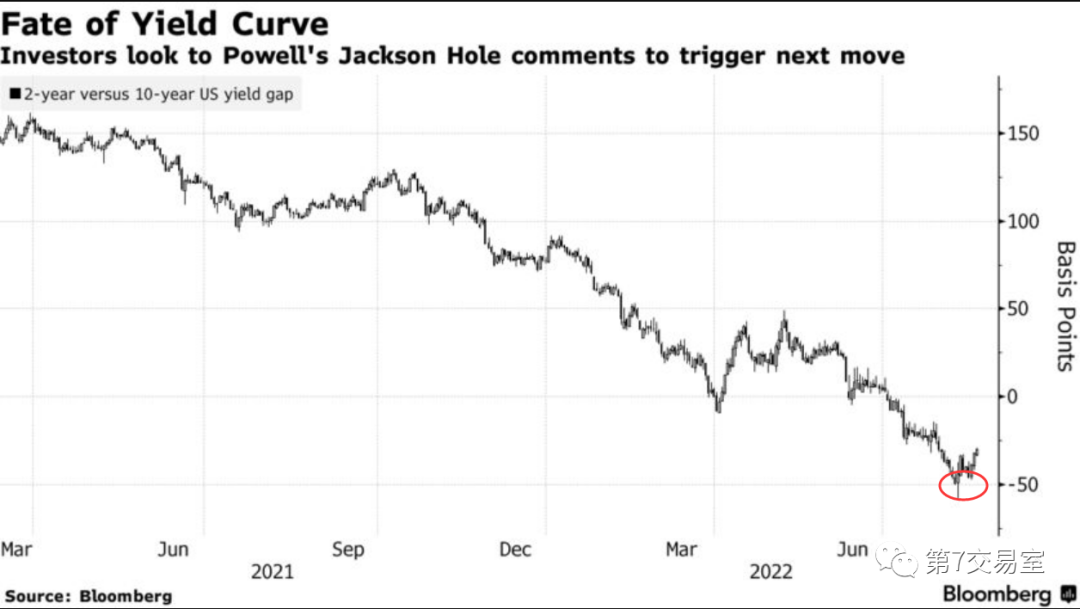

Previously, the two-year US bond yield rose due to the Fed's expectation of raising interest rates, while the long-term 10-year US bond yield fell due to the expectation of recession. Therefore, the market will have the upside-down phenomenon that the short-term interest rate is higher than the long-term interest rate, which will become the leading indicator to predict the coming of recession.

But have you noticed that the upside-down degree of 2-year and 10-year US bond yields began to rebound after bottoming out in June, which is surprisingly consistent with the bottoming time of US stocks

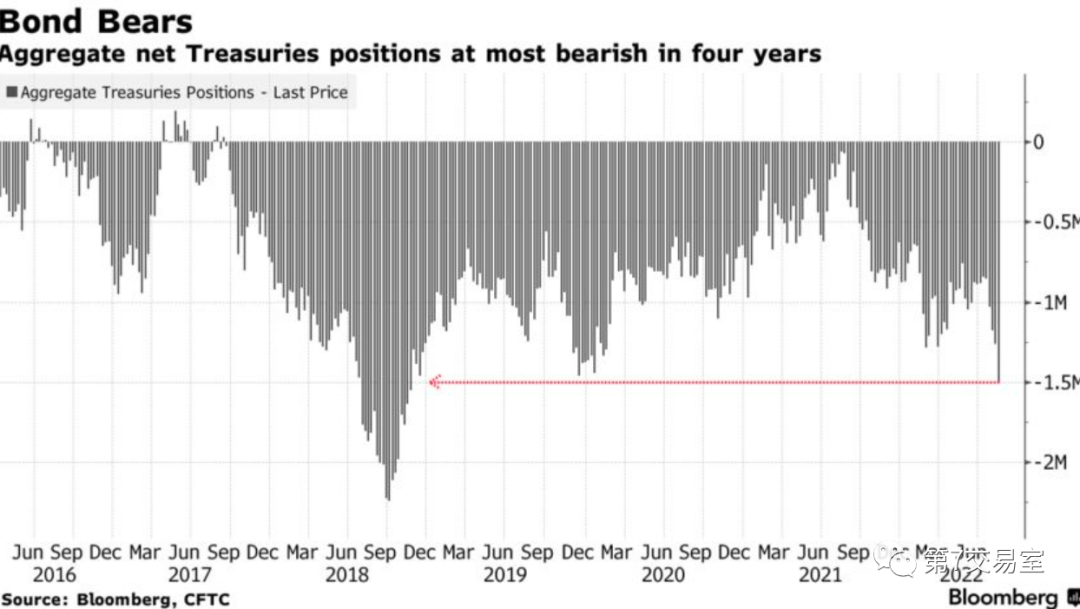

However, judging from the short position of US debt on CFTC, the bottoming out of US debt price is not over.

At present, there is such a tight balance in the US bond market: on the one hand, the QT process must continue, but at the same time, more returning funds need to be bought into US bonds.

If it wants more money to return to US debt, the Fed may have no other way at present, except to promise to raise interest rates and keep them high for a longer period of time.

It is very likely that at this Jackson Hole annual meeting, Powell will begin to dispel the market expectation of cutting interest rates in 2023, so in the Eurodollar interest rate futures market, the possibility of cutting interest rates next year, which has already started pricing, is rapidly decreasing:

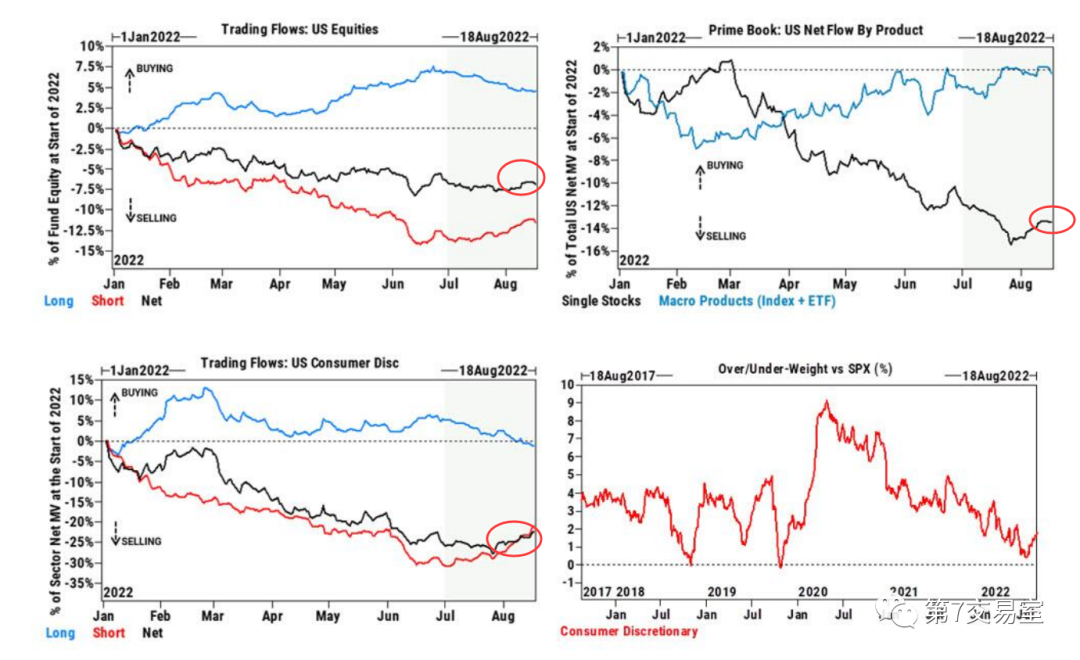

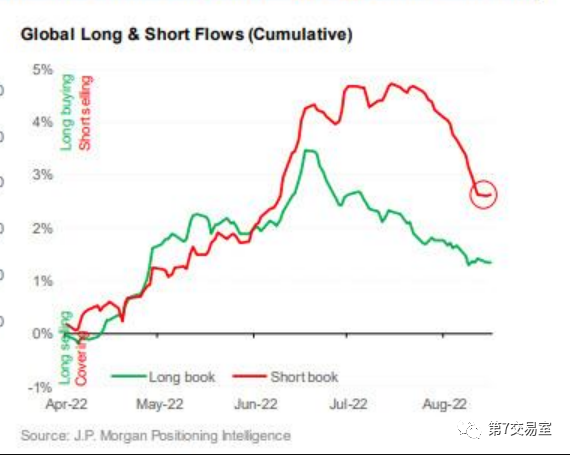

Short covering of US stocks stagnated

Withdrawal will be on the verge

With the complicated logic above, if Powell at this annual Jackson Hole meeting really leads the market to dispel the expectation of cutting interest rates next year as we predicted. It is even more likely that US stocks will fall in stages. The opportunity to short Tesla, Amazon and other high-power technology stocks may be right now.

The short positions of various stocks in the US stocks we track have slowed down to varying degrees in the recent replenishment

The selling of US stocks put bullish bets, and there was also a sideways stagnation

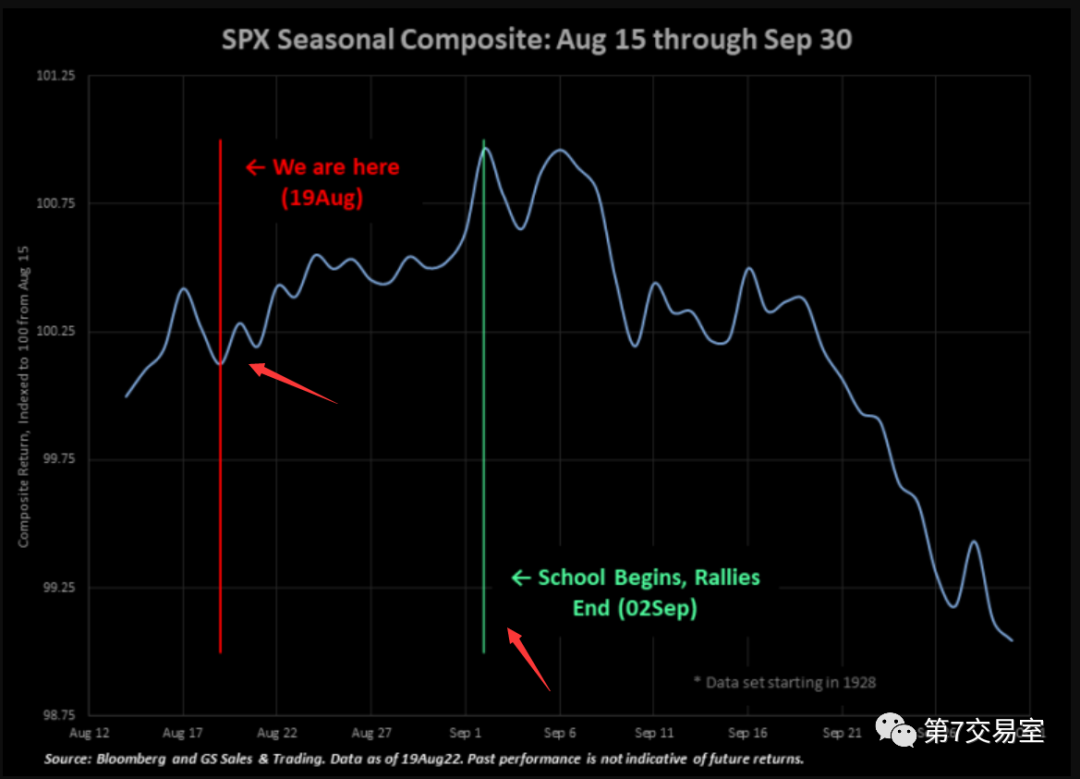

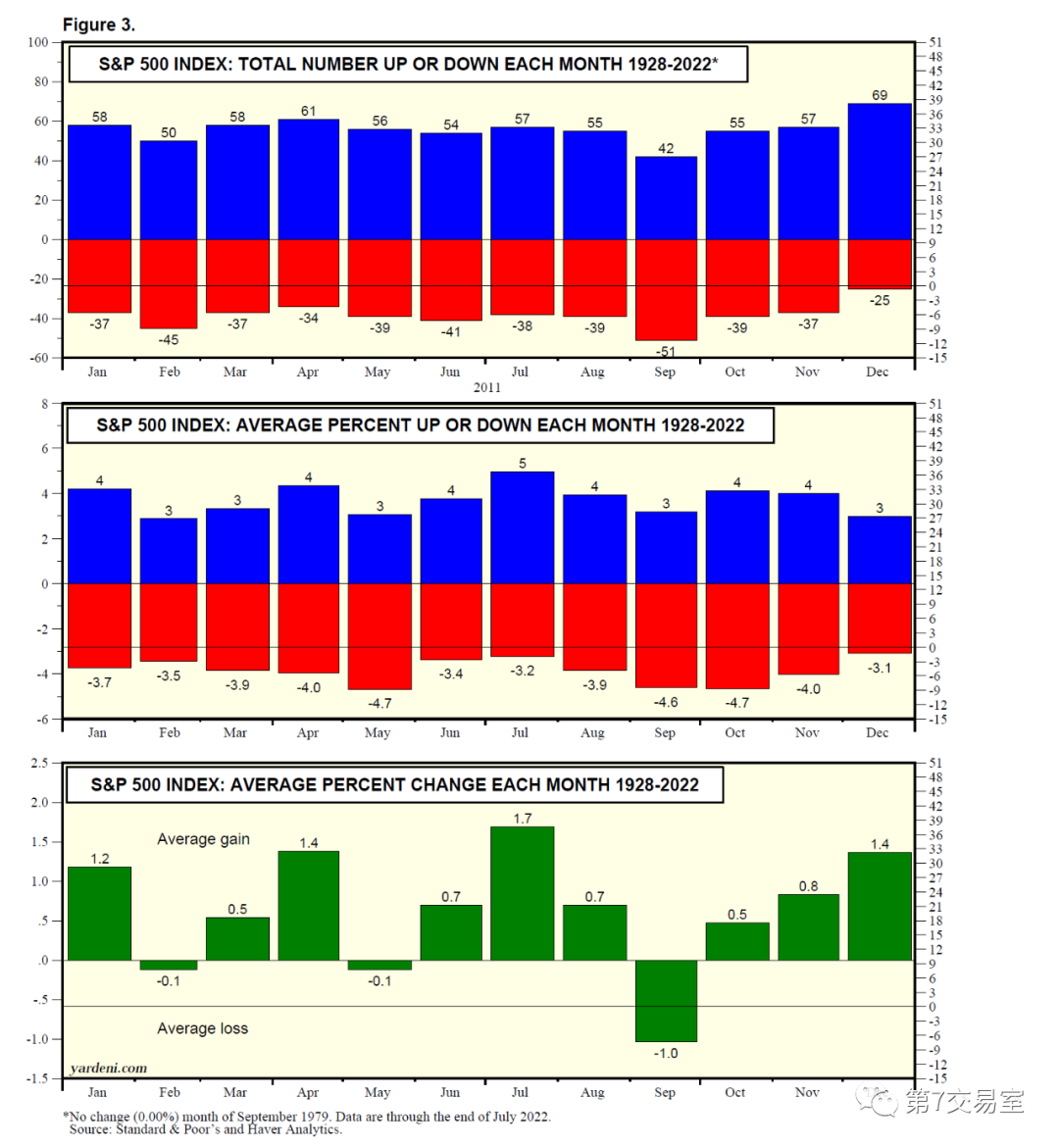

Looking at the quarterly chart, we are now at the end of the rally since the data on U.S. stocks were recorded, and in September, it is usually a high probability to peak and fall

The following statistical chart is more detailed:

So, get ready for a US stock market trembling in the long-term high interest rate market.

$E-mini Nasdaq 100 - main 2209(NQmain)$ $E-mini S&P 500 - main 2209(ESmain)$ $E-mini Dow Jones - main 2209(YMmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2210(CLmain)$

Comments

Finally, skill is the key