- US equity index futures fell and the dollar rose.

- Cryptocurrency-exposed stocks rise.

- Alibaba lost 1.9% in early trading.

(Aug 16) U.S. stock-index futures fell and the dollar rose as weak Chinese data and the spread of the coronavirus delta variant sparked worries the global economic rebound is faltering.

Contracts on the S&P 500 Index declined 0.3% after the underlying gauge notched up another record high on Friday. Commodities declined after Chinese retail sales and industrial outputdatashowed activity slowed. Alibaba Group Holding slid in premarket trading after China’s state media criticized the online-game industry.

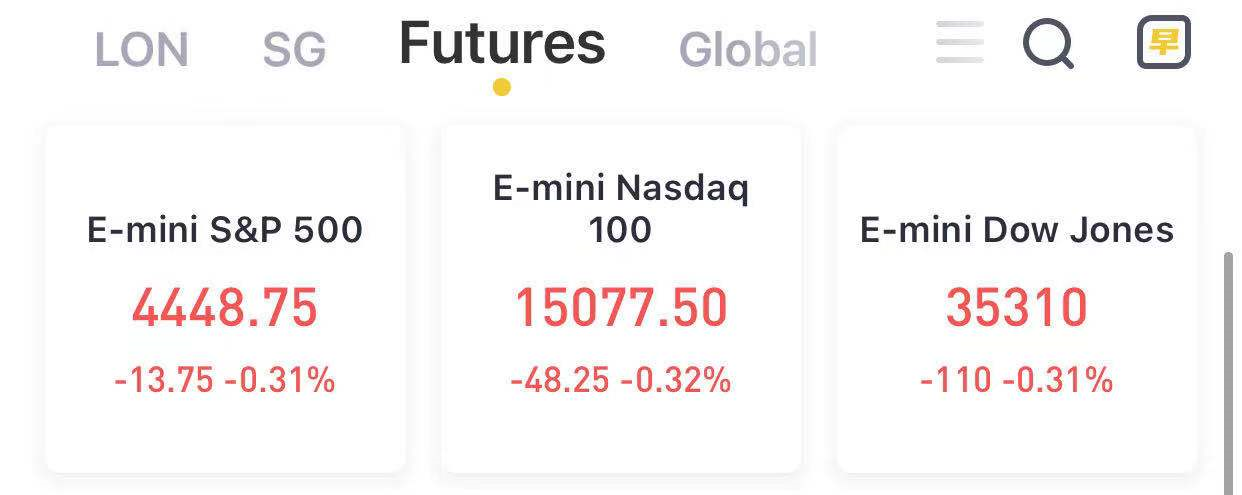

At 7:51 a.m. ET, Dow E-minis were down 110 points, or 0.31%, S&P 500 E-minis were down 13.75 points, or 0.31% and Nasdaq 100 E-minis were down 48.25 points, or 0.32%.

Stocks making the biggest moves in the premarket:

Sonos(SONO) – Sonos shares surged 10.6% in the premarket after an International Trade Commission judge ruled thatAlphabet’s(GOOGL) Google unit had infringed on some of the high-end speaker company’s audio technology patents. The ruling could eventually lead to an import ban for some Pixel smartphones and Nest audio speakers.

BHP(BHP) – The world’s biggest mining company said it is in talks to sell its petroleum business to Australian oil and natural gas producer Woodside Petroleum, with BHP also considering other options for the unit. Its shares fell 1.8% premarket.

T-Mobile US(TMUS) – The wireless carrier said it is investigating claims in an online forum of a data breach that involves the personal data of over 100 million users. The post itself doesn’t mention T-Mobile but Vice Media quotes the purported hacker as saying the data came from T-Mobile servers.

Chipotle Mexican Grill(CMG) – Raymond James lowered its rating on the restaurant chain’s shares to “outperform” from “strong buy.” The firm said the ratings cut is based entirely on valuation after a 37% jump in the stock over the past six weeks.

Hyatt Hotels(H) – Hyatt is buying resort operator Apple Leisure Group from private-equity firmsKKR(KKR) and KSL Capital Partners for $2.7 billion. Apple Leisure is the operator of the Secrets, Dreams and Breathless Resorts & Spa chains.

Coinbase(COIN) – The cryptocurrency exchange operator's shares rose 1.6% in the premarket as the recent crypto rally rolls on. The rally is also helping shares of business analytics companyMicroStrategy(MSTR), which has billions in bitcoin holdings on its balance sheets. MicroStrategy added 2.2% in premarket trading.

The Honest Company(HNST) – The maker of personal care products was upgraded to “buy” from “neutral” at Guggenheim Securities, citing valuation after a more than 28% tumble for the stock on Friday. That followed a quarterly report for the company that showed a wider-than-expected loss.

Tencent Music Entertainment(TME) – The music streaming service plans to halt its planned $5 billion initial public offering amid the ongoing regulatory crackdown by the Chinese government, according to Japan’s Nikkei news service. Tencent shares slid 1.3% in premarket action.

Seagate Technology(STX) – The hard disk drive maker’s shares added 1.3% in premarket trading after UBS upgraded the stock to “buy” from “neutral,” citing positive cyclical and structural dynamics in the industry.

Oatly(OTLY) – The oat milk producer reported a quarterly loss of 11 cents per share, one cent a share wider than expected. Revenue came in slightly below Wall Street forecasts. Oatly said it was able to overcome both Covid and manufacturing-related headwinds during the quarter, and that it is successfully executing its planned expansion of manufacturing capacity. Oatly shares rose 1% in the premarket.

In FX, the Bloomberg Dollar Spot Index inched higher and the yen and the Swiss franc led an advance among Group-of-10 peers while resource-based currencies such as the Australian dollar and Norwegian krone weakened.The Swiss National Bank appears to have intervened in the currency market to weaken the franc, with the amount of cash commercial lenders hold at the institution increasing by more than a billion francs for a second week running.Australia’s bonds gained and the Aussie dollar slid toward an almost one-month low after surging Covid cases led the NSW government to put the entire state into a weeklong lockdown; offshore sentiment was further weighed down by falling stocks and commodity prices. Japan’s sovereign bonds gained with the yen as a slump in U.S. consumer sentiment and weaker-than-expected Chinese data clouded the global economic outlook. The euro inched lower to around $1.1780 after rallying to a one-week high Friday; options traders are betting volatility in the euro will stay low and ranges will tighten further into year-end even amid the possibility of monetary policy divergence materializing between the Federal Reserve and the European Central Bank. The pound traded little changed against the dollar and the euro ahead of inflation, labor market and retail sales releases later this week; leveraged funds increased bullish bets on the British currency, according to data from the Commodity Futures Trading Commission for the week through Aug. 10

In rates, treasuries were little changed in early U.S. trading after erasing gains that sent yields to lowest levels in at least a week, tracking similar reversals in German and U.K. yields, and rebounding U.S. equity index futures. Yields were mixed across the curve, within 1bp of Friday’s closing levels, the10-year was flat at 1.277% after erasing a 3.2bp drop to 1.245%, lowest since Aug. 6.Coupon auctions ahead this week include $27b 20-year new issue Wednesday, $8b 30Y TIPS reopening Thursday.

Bitcoin traded around $47,400. Its second-day gain helped crypto stocks to rise in premarket deals. Riot Blockchain added 2.5%. Crude oil dropped for a third day as the resurgent pandemic hurt prospects for global demand.

There is little on today's calendar with the Empire Manufacturing Fed due at 830am, and the latest TIC data after the close.