The RMB exchange rate remains generally strong despite mild corrections in the past two trading sessions. On April 20, the onshore USD/CNY settled at 6.8198. The pair hit a high of 6.8156 on April 14, marking the strongest level since March 2023.

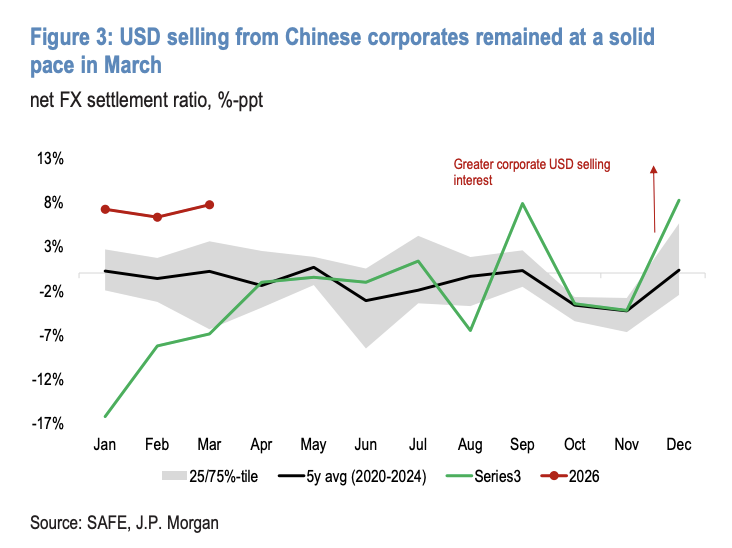

JPMorgan points out that robust corporate foreign exchange settlement serves as a key pillar for the RMB’s mid-term appreciation. Corporate USD selling has stayed resilient even after the seasonal Spring Festival impact faded. In March, the overall foreign exchange settlement ratio and net settlement ratio both hit the highest reading for the same period since 2020. Notably, exporters are converting not only incremental USD revenues but also unwinding massive USD savings accumulated over recent years.

Meanwhile, the RMB’s safe-haven appeal has strengthened. Amid the Middle East geopolitical conflicts, USD/CNH has stayed firmly below the 7.0 key level. The RMB’s relative resilience, coupled with the fragmentation of the petrodollar system and a rising share of RMB invoicing and settlement in energy trade, has further solidified its safe-haven credentials.

With bullish fundamentals intensifying, JPMorgan has upgraded its RMB forecasts and revised down its USD/CNY projections, expecting the currency pair to test the 6.70 level in the coming quarters. The counter-cyclical factor has been reactivated recently, signalling the central bank’s renewed willingness to fine-tune the exchange rate. Nevertheless, JPMorgan expects the PBOC to prioritize orderly appreciation via measured pace control, rather than enforcing rigid curbs on RMB gains.

Corporate USD Selling Sustains RMB Upside on Solid Settlement Momentum

Structural forces supporting the RMB’s mid-term strength continue to build, with persistent corporate USD disposals acting as a core driving factor.

Data from the State Administration of Foreign Exchange (SAFE) shows March saw exceptionally strong settlement momentum, outpacing typical seasonal patterns. The aggregate foreign exchange settlement and sales ratio stood at 71.0%, while the net settlement ratio reached 7.7 percentage points, both hitting multi-year highs since 2020. Against heightened geopolitical risks and elevated FX volatility, enterprises show strong willingness to convert USD proceeds into RMB.

More notably, corporate net USD sales have exceeded the theoretical ceiling of incremental trade income settlement. Merchandise trade-related net USD outflows stood at USD 60 billion in March, unchanged from February, amid a narrowing trade surplus. Per SAFE estimates, exporters generated around USD 50 billion in new trade income last month, of which roughly 30% was denominated in RMB, leaving an estimated USD 35 billion eligible for regular settlement. Actual settlement volumes far exceeded this estimate, confirming broad liquidation of historical offshore USD deposits.

JPMorgan estimates Chinese firms accumulated USD 600 billion to USD 900 billion in overseas dollar deposits between 2022 and 2025. This massive stockpile provides lasting settlement potential and will underpin RMB appreciation over the medium to long term.

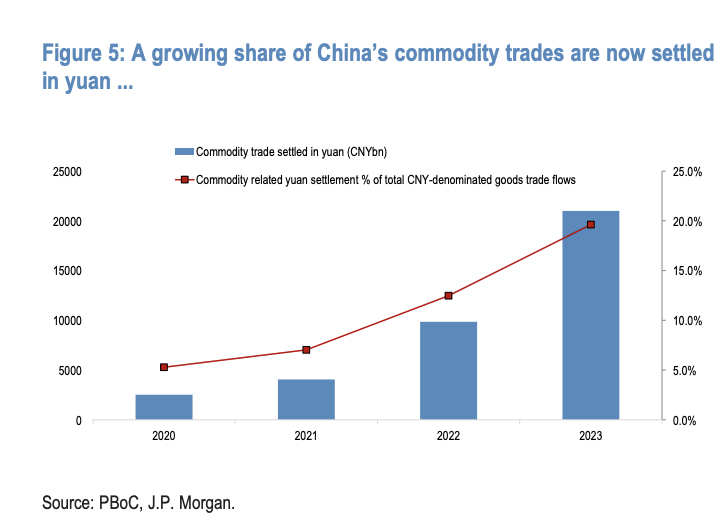

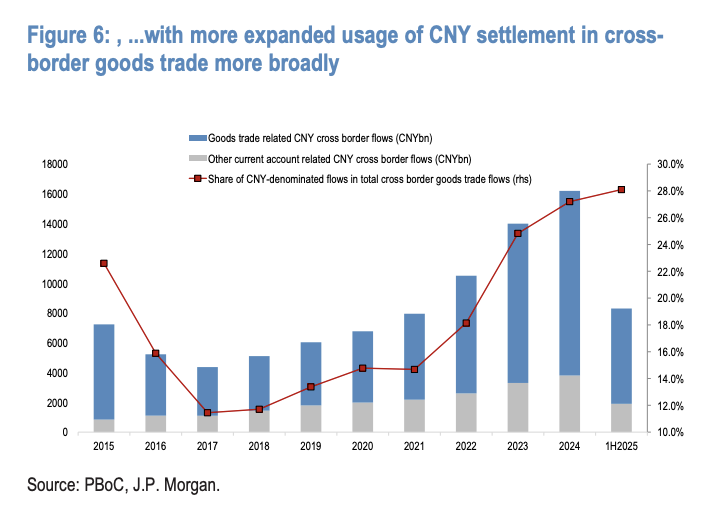

Rising Safe-Haven Status: Soaring RMB Settlement in Commodity Trade

Beyond corporate settlement, the RMB’s growing status as a global trade currency offers additional upside catalysts.

During the Middle East crisis, USD/CNH held steadily below 7.0, cementing the narrative of the RMB as a stable safe-haven alternative. Discussions over petrodollar fragmentation and greater RMB adoption in energy transactions have also gathered traction.

Official data validates this structural shift. The RMB-settled volume of commodity trade as a share of total RMB-denominated goods trade has climbed from approximately 5% in 2020 to 20% in 2023. The RMB’s overall share in cross-border merchandise trade settlement has neared 30%, a sharp increase from 12% in 2018. Zhou Xiaochuan, former Governor of the People’s Bank of China, recently stated that RMB internationalization has entered a “golden era”, supported by weakening global confidence in the US dollar and China’s persistent trade surplus.

RMB Target Raised to 6.70, PBOC to Focus on Gradual Regulation

Building on its constructive mid-term outlook, JPMorgan has further upgraded RMB prospects and cut its USD/CNY forecasts across time horizons.

The bank revised its quarterly USD/CNY targets downward from a flat 6.85 to 6.80 (Q2 2026), 6.75 (Q3 2026), 6.70 (Q4 2026) and 6.70 (Q1 2027). The 6.70 target reflects a directional assessment of RMB appreciation rather than a precise near-term path, with actual adjustments set to remain volatile and non-linear.

On policy, the PBOC has stepped up counter-cyclical adjustments with the reactivation of the counter-cyclical factor. Instead of imposing rigid price limits to halt appreciation, the authority is likely to manage appreciation gradually and avoid disrupting the underlying upward trend.

On the trading front, wide deviations between spot rates and official daily fixings keep JPMorgan neutral on USD/CNY in the near term. That said, the bank favours adding short USD positions on technical rebounds, rather than chasing long dollar exposure at current levels.