Morgan Stanley lowered its price target on Tesla to $320 from $345 on Wednesday as the firm reacted to the deceleration in electric vehicle demand, despite the recent price cuts in the sector.

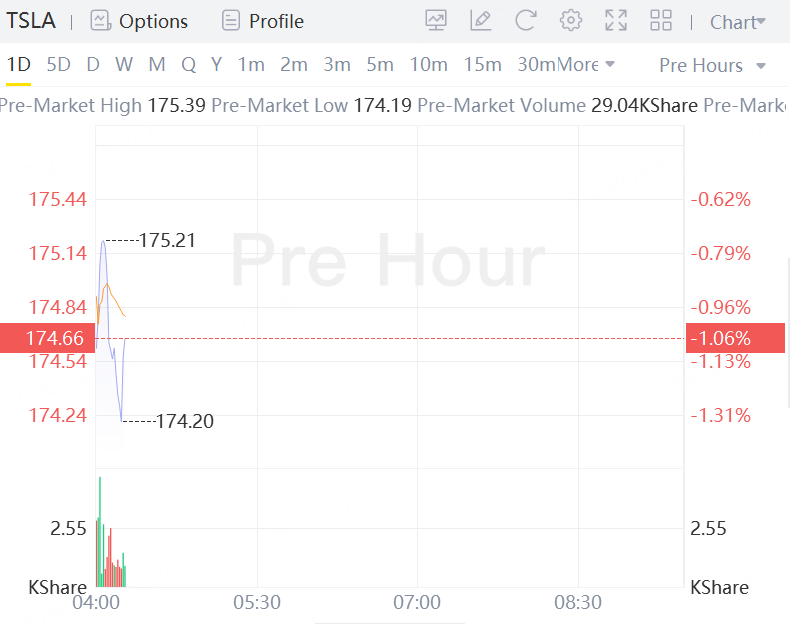

Shares of Tesla fell 1.06% in premarket trading on Thursday.

Adam Jonas warned that fleets are dumping EV plans and hybrids are competing for the marginal EV buyer. He also raises the possibility that Tesla posts a negative GAAP EBIT in the auto business this year. "We expect Tesla’s 1H24 results to come in below expectations on profitability, with GAAP OP margins in the 2-3% range, implying underlying EV manufacturing margins (ex downstream retail and ZEV credits) to be potentially in the red," he updated.

While Morgan Stanley expects Tesla to pull back on price cuts to defend margins and cash flow, FY24 automotive gross margin is seen falling to 11.4% for FY24 including a single-digit margin rate for Q2. The firm's FY24 EPS estimate was cut to $0.99 vs. $1.54 previously. The non-GAAP EPS estimate was lowered to $1.51 vs. $2.04 previously.

Despite the lowered expectations for Tesla, Morgan Stanley stuck with an Overweight rating on the EV stock.

TSLA breakdown: "We believe Tesla has significant attributes to be valued as an AI beneficiary, but the company must see a stabilization in the negative earnings revisions within the auto business first. We do not believe Tesla will get credit as an AI company as long as core auto earnings are being revised down. This process may take a few more quarters to see through, over which time our $100 bear case may be in play."