Alibaba stock surged nearly 5% in premarket trading after its shares closing up 3.4% in Hong Kong.

- Suspended Ant Group IPO, Jack Ma's disappearance, and regulatory concerns have forced Alibaba’s stock price ~-30% off highs.

- I believe Alibaba is trading at massive discounts on a relative basis.

- Future growth runways coupled with discounted buying opportunities could create a valuable investment opportunity.

Intro

Currently, in a market full of elevated asset prices it can be difficult for investors to find underappreciated securities on a valuation basis. After months of negative headlines and regulatory issues, I believe Alibaba (BABA) is being underappreciated through the lens of both valuation and growth potential. While investors may be fearful of regulatory risks, management stability, and financial legitimacy, BABA’s growth runway coupled with discounted prices could potentially produce a valuable investment opportunity.

Why I Think it is Cheap

After Chinese regulators suspended the highly anticipated IPO of Ant Group due to issues surrounding changes in the financial regulatory environment and how the company was not meeting disclosure requirements, BABA’s share price began seeing initial selling pressure. BABA saw an -8.13% dip in share price after the IPO was delayed. Given that BABA has a 33% equity interestin the company, the canceled listing of Ant Group caused obvious headwinds. Shortly after the canceled IPO, Jack Ma publicly denounced China’s financial regulators on stage at a conference in Shanghai. Adding to the mountain of negative headlines, the outspoken founder went missing shortly after this stint which was followed by a further decline in share price. Weeks after Ma’s criticisms regarding China’s regulators, China came crashing down hard on Alibaba with an antitrust investigation based on monopolistic concerns. BABA’s share price began to see deep selling pressure in late December with the U.S.-listed ADR falling over -13% on Christmas Eve.

After a slew of negative press, financial and regulatory headwinds, BABA has fallen ~-30% from ATH where it currently sits just over $210 a share. With share price declining and earnings continuing to grow rapidly, Alibaba has seen valuation multiples contract to levels not seen since shortly after their NYSE listing in 2015.

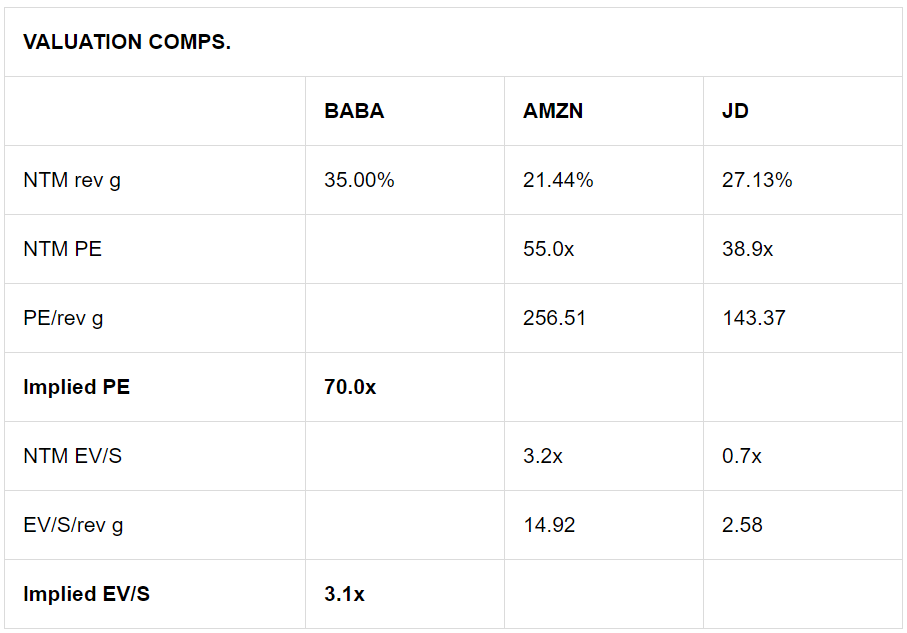

How Cheap is it on a Relative Basis?

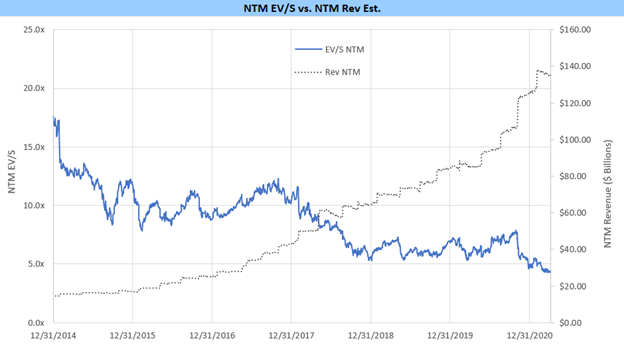

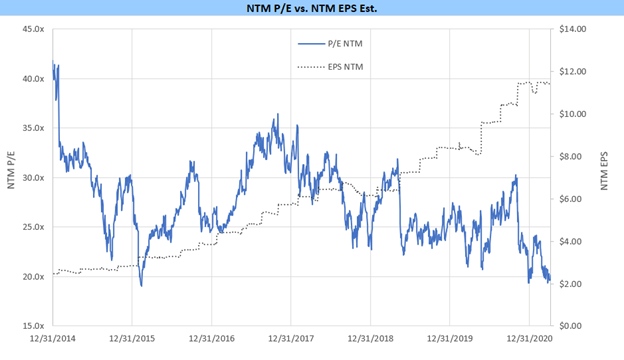

Using the next twelve months forward earnings estimates, "NTM," we begin to quantify how discounted BABA is through valuation multiples. Below are two charts showing BABA at the very bottom of its EV/S and P/E channels. Each chart compares the NTM multiple relative to the earnings denominator (NTM Revs & NTM EPS respectively).

Since BABA listed on the NYSE, their EV/S multiple has contracted over time as revenue growth has progressed rapidly; P/E typically has traded in a range of 20x – 35x NTM EPS estimates. Due to hyper EPS growth in the last few years, coupled with the short-term price downturn; Alibaba’s NTM P/E multiple has contracted to the very bottom of its historical channel (~20x NTM P/E).

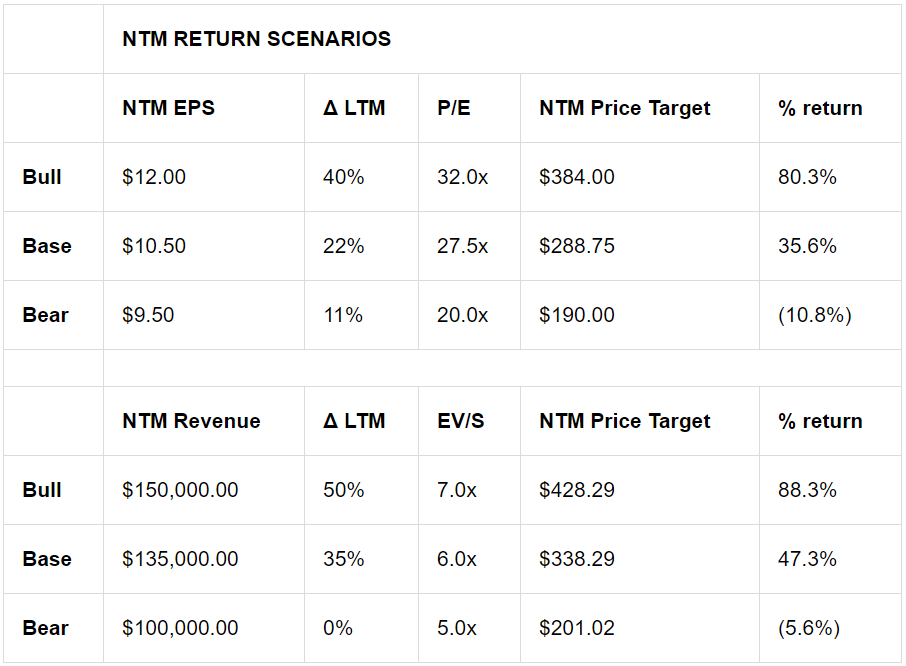

Next, I used NTM forecasts for both revenue and EPS, coupled with bull, bear, and base case NTM multiples to derive my case-specific price targets. Price targets using EPS and P/E were calculated by multiplying expected NTM EPS by expected NTM P/E. Price targets using revenue and EV/S were calculated by multiplying expected NTM rev by expected NTM EV/S, subtracting trailing twelve months "TTM" net debt (-$52,797.3M) and dividing by TTM diluted shares outstanding (2,750M).

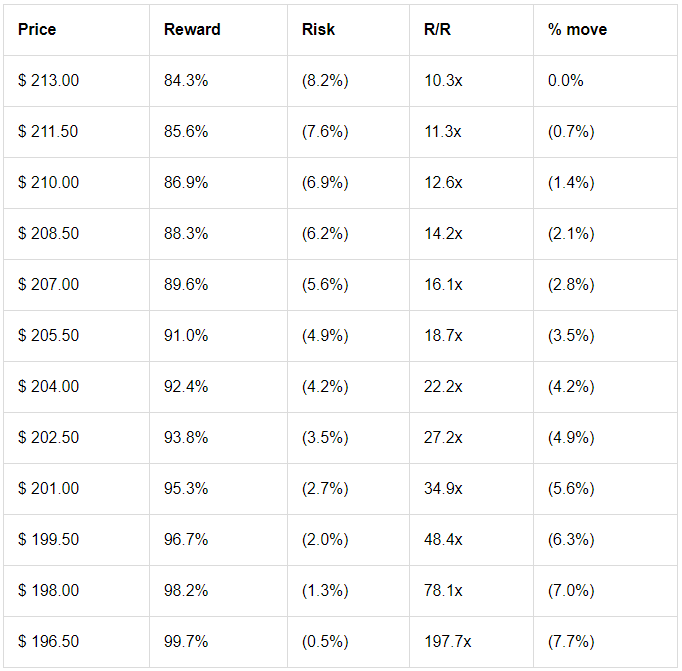

After taking the median bull and bear price targets, I created a tactical risk/reward chart to determine BABA’s margin of safety at current price levels. I used the median to calculate official price targets to gain exposure from both BABA's top and bottom-line.

Given a market price of $213, BABA implies a 10.3x risk/reward level based on my forecasts. After comparing my multiple expectations to competitors, there is the risk of further contraction in EV/S over time but BABA appears very discounted relative to competition on a P/E basis.

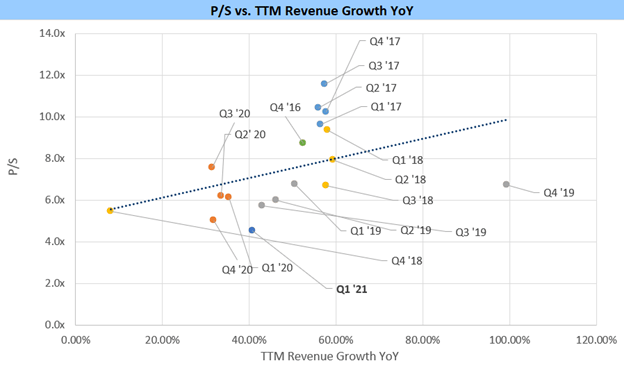

Next, I wanted to measure BABA’s discounted valuation relative to TTM revenue growth. To do this I created a scatter plot, charting P/S on a TTM basis on the y-axis and TTM revenue growth YoY on the x-axis. Points charted under the dashed line are deemed undervalued and any points above the line are deemed overvalued.

Based on TTM revenue growth through Q1 ’21, it’s clear to see the major discount BABA also has adjusted for top-line growth. Lastly, I wanted to throw in a price action chart with a long-term trendline pointing to BABA’s discounted price factor:

Growth Runway

To capture excellent investment gains, valuation is not enough, Alibaba will have to continue executing its growth strategy. While the stock seems to be cheap on a relative basis, I also believe growth on the top and bottom lines is imminent.

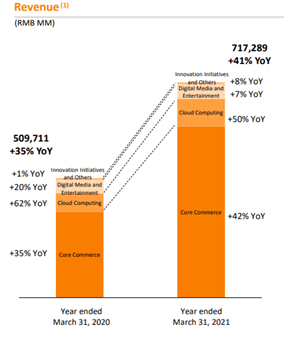

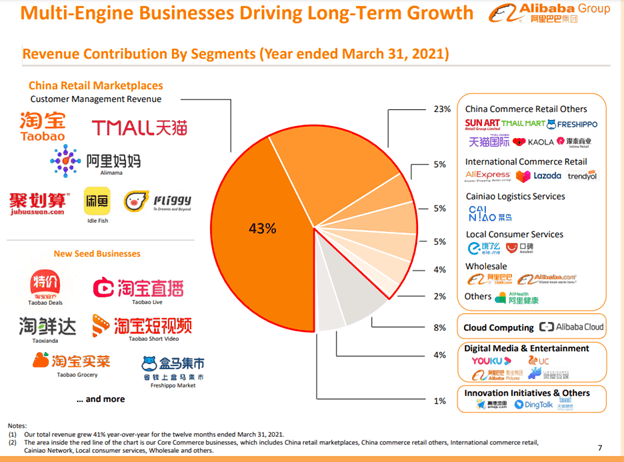

After their Q1 release, BABA reported 41% YoY growth on the top-line driven by their leading core commerce segment alongside the fast-growing cloud segment. Coming off 35% YoY growth in 2020, being able to deliver a 41% topline increase is incredible for the year following. Given the fact COVID-19related online growth was reflected in early 2020 results, I find it very feasiblefor core commerce tailwinds to continue as growth persisted, and expanded, the following year.

Alongside general e-commerce tailwinds, China’s middle-class growth could support sales for a mega-cap commerce player like Alibaba. “China already makes up the largest middle-class consumption market segment in the world” asChinese middle-class consumers were on track to spend over $7.3 Trillion in 2020, roughly 55% higher than the United States middle-class at $4.7 Trillion. At current levels, less than one-third of China’s total population lies within their middle-class, containing roughly 400 million people. Population expectations for the Chinese middle-class are expected to be 1.2 Billion people in 2027, a 17% CAGR. Coupling the sheer class population growth with a forecasted income CAGR of 3% stacked on top, BABA is potentially looking at a 20% built-in core commerce CAGR over the next 7 years based on these estimates.

Lastly, I believe the digital transformation acceleration happening around the globewill be an excellent growth catalyst for the company moving forward. Like Amazon, Alibaba constructed its cloud base on logistical support for the commerce/delivery giant. Now that the infrastructure is built, they can grow the cloud as an operating segment, separate from core commerce, and outsource to major customers.

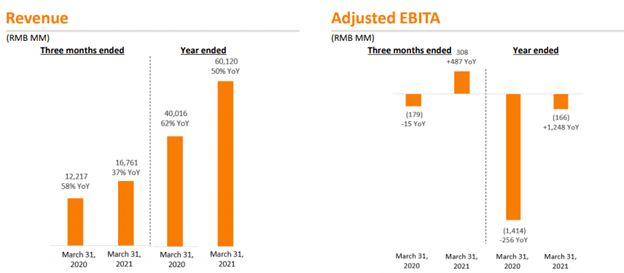

Below you can see previous YoY growth on three months ended and annual basis.

While Alibaba Cloud only makes up 8% of total revenues, in the future I believe this segment will be a larger contributor to the total top-line as domestic and international adoption grows. Couple the cloud with core commerce expansion propelled forward by a rapidly increasing middle-class and BABA's growth runway is seemingly attractive for short and long-term investors.

Risks

The reason this opportunity exists isn't because of a systematic drawdown or a major global catalyst suppressing stock prices, there are clear idiosyncratic risks to investing in Alibaba. The major risks of a BABA investment were highlighted clearly over the past 7 months. Starting with the Ant IPO suspension, BABA investors became concerned not just with the fin-tech company exposure, but also began questioning the financial legitimacy of BABA itself. To make things worse, the outspoken billionaire founder denounced the Chinese regulators in a very public fashion. Obviously, China didn't like this and launched the full-fledged antitrust investigation into Alibaba. The regulatory risk is my biggest concern while investing in BABA. At the end of the day, I've only ever lived in the United States and am no expert on Chinese foreign policy. I want to make clear these regulatory risks are very real for any mega-cap company but potentially more so for those internationally. As an investor, it's very important to run through all the potential risks to a company before investing and only allocate capital if you believe the potential reward outweighs the risks accounted for.

Summary

In a short-term view, Alibaba has an excellent catalyst with the 6.18 sale. It is their first major sale since COVID, and it lasts from May 24th – June 20th. While sales like these are common annually and may have an extremely minimal effect on stock price, the positive sentiment generated could be a good turning point for BABA. Based on a long-term approach, I believe Alibaba will continue to be a massive global leader and continue to dominate Chinese e-commerce even in the wake of regulatory risk. With a rapidly growing middle-class and a digital transformation acceleration, I think core commerce and Alibaba cloud will continue driving growth for the company. After paying off the fine imposed I think much of the regulatory risk is behind them now. As future earnings growth has the potential to outweigh any regulatory concerns, BABA is in the making be an excellent investment opportunity, especially at deeply discounted valuations.