Summary

- Sea reported its Q4 and FY 2021 earnings in early March. The stock has dropped substantially since then, bringing it down 75% from its high now.

- We look at the numbers in full detail and look at several insights that we can get from the numbers. Context is extremely important here.

- We also look at the guidance and the future of Garena, Shopee and SeaMoney.

- Sea has a ton of optionality, some obvious, some less obvious.

- I argue why I think the stock has become cheap now from the perspective of a long-term investor.

- I do much more than just articles at Potential Multibaggers: Members get access to model portfolios, regular updates, a chat room, and more.

kokkai/iStock Unreleased via Getty Images

Introduction

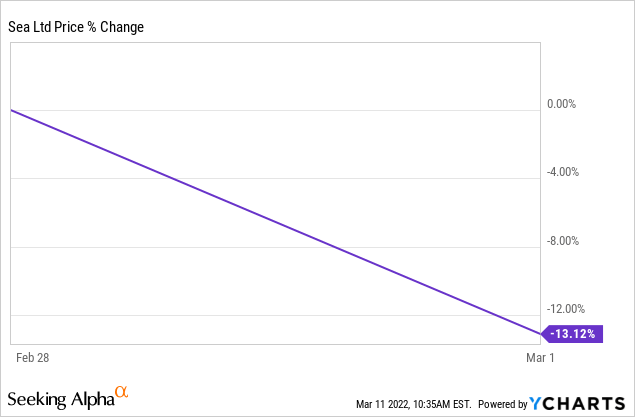

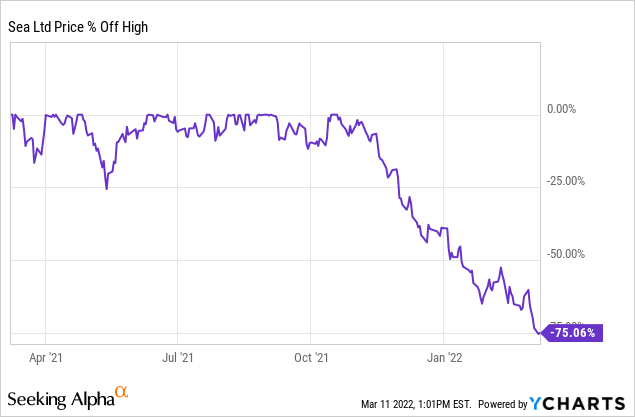

Sea's (SE) stock price has dropped a lot over the last few months and the recent Q4 and FY 2021 earnings results added to that drop, dropping 13% on the day of the earnings.

The stock is now down 75% from its highs just a few months ago. And it is down ~58% year to date.

To put this into a meaningful context, let's dive into the Q4 and FY 2021 earnings first, which were released on March 1. Then look at what worries investors and if to which level that is warranted or not.

The results in numbers

As a group, Sea's revenue was $3.2B inQ4 2021, up 105.7% YoY, another double. Gross profit came in at $1.3B, up 145.6%. That's already important to see and therefore I want to point it out: gross profits are up more than revenue. The company has substantially higher gross profits than revenue growth, which shows that its growth leads to cost advantages, also known as operating leverage.

The EBITDA, though, came in at a loss of $492.1M, while it was a positive $48.7M in Q4 2020, that strange year. We'll come back to this, but let's first look at Sea's different divisions.

Garena

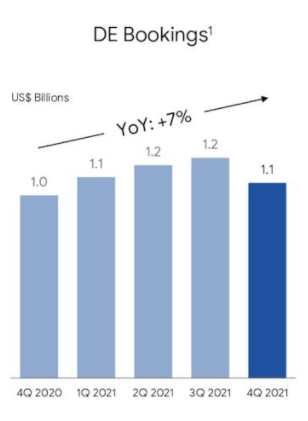

Garena's revenue was $1.4B, up 104.1% YoY. Bookings were $1.1B, up just 6.8% YoY. It's essential to understand the difference between these two. Bookings are the money that gamers have already paid, but that money can only be recognized as revenue when they spend it. If they pay $50 but only spend $10 in Q1 2022, there will be $10 in revenue but $50 in bookings. In that way, bookings give you a window into the future.

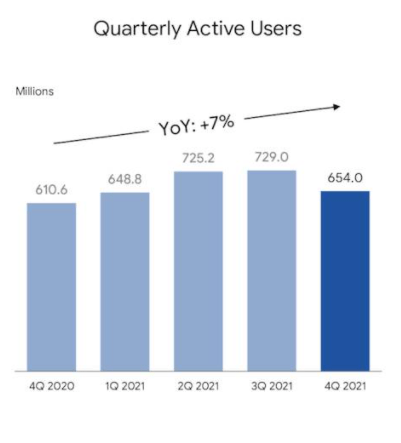

The Garena EBITDA was $602.6M, down 10.11% YoY. That comes entirely from the margins going down from 65.5% to 55.7%. The QAUs or quarterly active users number was up 7.1% YoY. As you can see, this number is close to the 6.8% extra bookings and that's no coincidence as the two are linked closely.

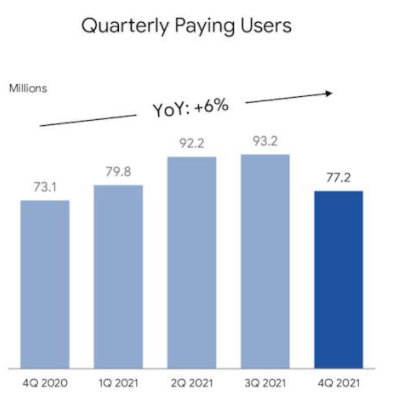

The QPU or quarterly paying users were up 5.6% YoY to 77.2 million. That's 11.8% of all the QUAs, while that was 12% in Q4 2020. Don't forget that Q4 was an exceptional quarter because of the pandemic, so this is still pretty good and above pre-pandemic levels. The average paying user paid $1.70, unchanged from Q4 2020.

Free Fire remained the most downloaded game worldwide (for the third consecutive quarter) and ranked second when it came to monthly active users for all mobile games on Google Play for both the quarter and the full year. In Southeast Asia and Latin America, Free Fire remained the highest-grossing mobile game for the 10th consecutive quarter. Free Fire was the highest-grossing mobile battle royal game in the US for Q4 and FY 2021. All impressive achievements for a company with its first self-developed game.

What these numbers clearly show is that Free Fire, which accounts for about 75% of Garena's revenue, is still (here it comes)firingon all cylinders. It's a hugely successful game, and it keeps doing well, but the difference between Q4 2021 and Q4 2020 is, of course, that kids now have to go to school or college and, therefore, simply have less time to play their favorite game. Free Fire still grows, albeit modestly, which is a substantial accomplishment, although many won't see it like that. Overall, engagement in gaming has declined, as you can also see from the results from other gaming companies and that's not strange, considering the circumstances. We come back to Garena later in this article.

Shopee

Shopee's revenue came in at $1.6B, up 89.4% YoY, a very strong achievement, as this is also on top of a Covid-fueled Q4 2020. $1.3B came from marketplace revenue, up 103.5% YoY, the remaining $300M from product revenue, up 48.1% YoY. Product revenue is revenue from Shopee as 1P, in other words, products the company buys and sells itself, like the original Amazon model. As you can see, the marketplace revenue grows much faster, and of course, margins have the potential to be much higher there as well.

There were two billion gross orders in Q4 2021, resulting in 90.1% YoY growth, and total GMV came in at $18.2B. GMV stands for gross merchandise volume, meaning the total dollar amount of everything sold on the platform in Q4. GMV grew 52.7% YoY.

It's not strange to see this grow less outspoken than gross orders if you know the context. Shopee has launched in quite a few new markets recently (India, Mexico, Argentina...), and in new markets, people always tend to buy lower-priced items to test out the service. That lowers the average ticket price of items sold. With $18.2B and two billion orders, the average item cost is just above $9, relatively low, but you should see that go up over time, as it previously did in other markets.

The EBITDA for Shopee in Q4 was a loss of $877.7 million, more than doubling the EBITDA loss of 427.5M of Q4 2020. Again, this is the consequence of launching in new markets. If it launches,Shopeeinitially takes big losses because of free shipping and an extremely low take-rate (often zero) to onboard merchants. This could be another reason why investors are worried. In these times, interest rates are expected to grow. According to some banks, nine interest rate hikes areexpectedfor 2022 (which I don't see happening). Investors see this and they get scared about the big losses that Shopee brings to Sea. I'll address this worry later in the article.

In Southeast Asia and Taiwan, Shopee's original market, the EBITDA loss per order was $0.15, down from $0.21 in Q4 2020. That also shows that the bigger losses don't come from there, even though orders probably went up quite significantly. Again, the bigger losses came from the new markets Shopee invests in heavily to gain market share. It does that quite successfully, I should add.

SeaMoney

E-commerce platforms are not really that great when it comes to investing in them. The real value for shareholders is in the extra services built on top of them. Amazon launched Prime, MercadoLibre added MercadoPago and those are the real high-margin businesses that are interesting for the long-term investors that we are as Multis.

For Sea, SeaMoney is a great opportunity. Shopee is crucial in the acquisition of customers for SeaMoney. The service is fully integrated with Shopee. While Shopee's results were outstanding, SeaMoney's results were jaw-dropping.

Revenue was up 711.1% YoY to $197.5M in Q4. Of course, this was growing from a small basis, but that growth in just one year is always very impressive to see. At the same time, the EBITDA loss went down from $171.3M in last year's Q4 to $149.8M in Q4 2021. TPV (total payment volume) was up 70.1% YoY to $5B.

In trouble or not?

As you can guess, from the stock price drop, investors saw reasons that worried them. And a stock that is down 70% could indicate a company in trouble, right? Not so here.

1. Garena

Garena is seen as the main cause of the significant stock price drop. What mostly spooked investors was that several key metrics came down QoQ:

Earnings slides

Earnings slides

Earnings slides

(Source:earnings call slides)

Especially the QPUs were down a lot compared to Q3 2021: 20%. QAUs were down 11.5% and bookings, the most important metric as this predicts the future revenue of Garena, 9%.

If you look at Activision Blizzard's (ATVI) resultsas a comparison, you see that Sea has actually done pretty well. Activision Blizzard's bookings were down 18.6% YoY already in Q4. However, it has to be said that Blizzard, the mobile gaming division, did better than the rest of the company's divisions, but still worse than Garena.

So, this is not a bad performance from Garena, but an industry-wide slowdown compared to that exceptional previous year that they had. You could argue that because of its core market in Southeast Asia, Garena's slowdown was slower to kick in as the pandemic restrictions were kept in place for a longer time there.

If you look at FY 2021, Garena's revenue was up 114.3% YoY to $4.3B, while bookings rose 44.3% YoY to $4.6B. For 2022, Sea projects bookings of $2.9B to $3.1B, which means 35% less than in 2021. While the adjusted EBTIDA was 60% of bookings in 2021, the current trend shows that this will probably be more between 50% and 55% going forward.

This was emphasized everywhere: Garena would no longer be a cash cow to fuel Sea's growth in its two other divisions. Some called this a huge problem. I can see the cause of the concerns, but I tend to disagree that this is a thesis-changing outlook if you consider this into a broader context, if you listen carefully to what management says, and especially if you look at the long term. Let me explain.

With $3B in bookings for FY 2022 and 50% EBITDA margins (both are very conservative, in my opinion), Garena would produce $1.5B in EBITDA for Sea. With $4.3B in bookings and 60% EBITDA margins, this was $2.58B in EBITDA in 2021. That's, give and take, a difference of $1.3B for one year, which is quite substantial, of course.

I think in reality, the difference will be smaller, as the company always guides very conservatively and on top of that, it has excluded India for the whole year, while there might be a solution coming, especially now that the Singaporean government has put its weight behind Sea versus the Indian government, asseveral sources have reported.

We still don't know why Free Fire was banned exactly. Did Garena partly use Chinese (Tencent) data centers? Seapointed out:

We do not transfer to, or store any data of our Indian users in, China.

Or was it the company structure, in which Tencent used to have quite some voting rights? Remarkably, Free Fire was banned just two days before Sea's General Meeting, which formalized the changes through which Tencent got less than 10% of the voting power.

Despite some Tencent ownership, Sea is entirely Singaporean and the relations between India and Singapore have been very good for a very long time. They signed the CECA (Comprehensive Economic Cooperation Agreement) in 2005 and Singapore is India's 5th-largest trading partner.

Forrest Li said on the conference call:

We remain extremely focused on developing Garena's global platform, which we see as a key strategic asset in the long run.

And in the press release:

We are working on multiple prototype games across different stages through both self-development and publishing pipelines. In 2022 and beyond, we expect to expand our portfolio with more games across diverse genres such as multiplayer action, role-playing, sandbox and casual games.

An analyst pressed a bit on the conference call, but Sea is not the company to announce long before. It only communicates when it can launch. But they are likely working on something new that can help Free Fire carry the burden of Garena. In 2020, it bought Phoenix Labs, the maker of Dauntless, and in 2021, it made investments in five other gaming companies. So I think they are working on something, but as is typical for the company, they only want to communicate when there is a launch date.

In 2023 (I think at the end of the year, but I haven't found explicit confirmation there), the current deal with Tencent (OTCPK:TCEHY) expires. Because of that deal, signed in 2018, the company has the first right to publish all Tencent games in Southeast Asia. So maybe that deal could be extended, maybe not. In any case, I think Garena needs a second game before that, just to hedge against a less favorable or no deal anymore.

Forrest Li addressed this issue and pointed out that next to developing their own games, Garena could expand their distribution deals beyond Tencent.

Over the long-term, our priority remains sustaining and growing our existing major franchises, while diversifying our games portfolio. Our strong and growing self-development capabilities will be a key component of this diversification effort. Our teams are working on multiple prototype games across different genres and stages.

In due course, we expect to bring more self-developed games to market. We also continue to actively acquire and invest in top talent and game IP to further expand our capabilities of both genre and geographies. Meanwhile, we will keep growing our publishing relationships, leveraging our unique set of strengths across diverse global markets.

Garena is also already working on the metaverse. Forrest Li onthe conference call:

Additionally, we have seen strong engagements with user-generated content through modes like Craftland, our recently introduced map editor feature. Since the launch the most popular Craftland maps have subscribed by close to 40 million users so far.

We will continue to encourage user-generated content by enhancing greater features and accessibility. We believe that a strong user reception to Craftland is a positive indicator of the initial success to encourage user participation in content creation and to build Free Fire into an increasingly open platform and is well aligned with major emerging industry trends such as metaverse.

2. Shopee

With a negative EBITDA of $877M in a quarter, Shopee could be a reason to worry as well, especially now that Garena will be less profitable. Shopee had a negative $0.15 EBITDA per order. With two billion orders in a quarter, that's problematic, you would think. But it's not. Shopee is the number one marketplace now in all of its Southeastern Asian markets, even Indonesia, which was confirmed in the press release (my italics).

InIndonesia, where Shopee is the largest e-commerce platform, gross orders grew by around 88% year-on-year. Shopee also continued to rank first in the Shopping category by average monthly active users and total time spent in-app for the fourth quarter and for the full year of 2021, according todata.ai.

That's very exciting. Indonesia is expected to be one of the top-5 economies in 2050 (after China, the US, and India). Even if that prediction proves to be too optimistic, it's still a huge country with a huge population and huge growth perspectives.

Suppose the Garena projections would be accurate. $1.5B in EBITDA for Sea. That's free money, so to speak, to grow the two other businesses. Mercado Libre (MELI), Shopee's most significant competitor in LatAm, doesn't have that highly profitable division. GoTo, the company formed by Gojek and Tokopedia, the only really powerful competitor in Indonesia, doesn't have that capital either. Lazada, owned by Alibaba, has the firepower, of course, but it has had that for years and still, it lost its dominant position to Shopee over time. Shopee is the number one in all of the countries it launched in originally: Indonesia, the Philippines, Taiwan, Thailand, Malaysia, Singapore and Vietnam.

Being the biggest gives Sea leverage. Would you skip to another platform for $0.15 extra on an order of probably around $15 (as that's probably the current order size in SEA by now)? That's just 1%. I know that I wouldn't.

This is what Forrest Li, Sea's founder and CEO, said on the conference call:

We currently expect Shopee to achieve positive adjusted EBITDA before HQ cost allocation in Southeast Asia and Taiwan by this year.

I'm not sure what 'HQ cost allocation' is precisely and that could have been made clearer. Is it a form of G&A (general and administrative costs)? I like that Sea gives us a lot of insights in their business, much more than, for example, Amazon or Google do, but this should have been made clearer to know the impact.

But for the rest, this is good. In its guidance, Sea expects Shopee's revenue to grow by more than 75% in 2022 to $8.9B to $9.1B. It would be a good development if that can be profitable, or even at just a slight loss (after 'HQ cost allocation') in Shopee's core market. That means that the money that Garena still generates (and about $10B on the balance sheet) can be used to grow Shopee in Brazil and even earlier markets. From thepress release:

In Brazil, where Shopee was launched in late 2019, we have already achieved strong traction with meaningful commercialization and improving efficiency.

As you see, even in Brazil, the efficiency is improving, just barely two years after the launch.

Investors often make projections by drawing lines. From negative EBITDA of $427M to negative $877M, a red alarm goes off in their head, signaling that this is unsustainable. And, of course, it is. But you can't just draw a line from a loss of $427M to $877M to even more losses. Bringing things to the essence is very important in investing, but it is too complicated to make it too simple.

Of course, you should still expect negative EBITDA next year, as Shopee expects to continue investing heavily in Brazil. Forrest Li on the conference call:

Broadly speaking Shopee LatAm and Brazil in particular, as well as R&D will be our top two focus areas for investments. Our investments and the overall impact on the bottom line is likely front-loaded as unit economics and profitability for our businesses generally improve with scale.

Forrest Li has shown that he executes when he talks. It's very rare for him to pound his chest. This time, he did that a bit, though, probably to comfort his shareholders, pointing out that Shopee has already been very successful in seven very diverse markets before. Here you see why I say that he pounds his chest because of Sea's shareholders (my bold):

Of course, it'd be much easier operationally for us to just focus on the seven existing core markets for Shopee. However, we strongly believe that by investing prudently and sustainably in Shopee Lat Am and Brazil in particular,we will generate significant value for our shareholders in the long run.

While we do not underestimate the challenges of any new market expansion, I would also like to highlight that we have an established track record, seven times in seven highly diverse and complex markets of Southeast Asia and Taiwan, where we started in each of those markets in 2015. We have significantly net resources, experience and the know-how and as a result, find a much more formidable competitive landscape that we currently do in our market expansion.

I really like this whole quote, as it shows everything I like about Sea and Forrest Li. They don't take the easy road that would be easiest for the short term; they look at this from a long-term perspective. As a long-term investor, that's music to my ears. Li also doesn't deny that it's hard what Shopee tries, but he shows that Shopee has the experience of seven different countries. Many investors who don't live in Southeast Asia may see the region as one part of the world, but the reality is that all countries are entirely different. For example, Singapore is a wealthy city-state with one of the lowest corruption rates in the world (far better than the US and most European countries). On the other hand, Indonesia is a conglomerate of thousands of islands, which is much earlier in its development and has a ton of internal regional differences. And those are just two of the seven.

Shopee sees big success in Brazil. In Q4 2021, it had 140 million orders, up 400% YoY for $70M of revenue, up 326% YoY. That means that there was just $0.50 of revenue for Shopee per order, and there was a significant loss on every order, of course. The company shared in its press release that the EBITDA loss per order improved by more than 40% YoY, to below $2.00. But that still means an EBITDA loss of $280M in just a quarter. For 2022, you can expect the same thing: improving losses, but still, substantial losses. While that may sound scary, it's part of Shopee's success formula.

In just two years, Shopee Brazil managed to rank first by downloads in the shopping category and total time spent in-app and second by average monthly active users in Brazil. That's simply insane. If you see this, and you can separate yourself from your emotions about the stock price, I think you see that the potential for Sea is vast.

If you look worldwide, Shopee ranked first for downloads in the shopping category both for Q4 and for FY 2021. Shopee also ranked first globally regarding total time spent in-app for shopping on Google Play. The iPhone is primarily a Western story; outside of the US and Western Europe, Google's Android dominates the market by a gigantic market share of probably 90%, so this is very important. Shopee also ranked second worldwide on Google Play when it came to average MAUs (monthly active users) in Q4 and FY 2021.

Shopee is on track to go to nearly $100B in GMV in 2022. That means that whole families depend on the platform, both from the merchant and customer sides. That means that Shopee has pricing power, even if that will always be limited because of the competition. It can add several extra monetizable services for merchants (ads, more insights, gamification, etc.) and it could introduce some sort of Amazon (AMZN) Prime formula in the future, especially if you combine it with its two other current divisions.

3. SeaMoney

SeaMoney is crucial for Sea over the longer term. With revenue growth of 711% in 2021, the comps are of course hard, but Sea sees growth of 155% to $1.2B at the midpoint for the current year on top of that 711% growth. And if history is a guide, it will probably beat that guidance.

The company even expects SeaMoney to be cashflow positive by next year, showing how quickly this can scale. Of course, there are high upfront costs, and the investments will continue, but the relatively higher gross margins and flexibility promise many good things for the future. Once the banking charters Sea has obtained in several countries start to kick in more and more, this will mean even more profitability for SeaMoney.

The operating leverage also shows in the number of users. The QAUs (quarterly average users) went up 89.7%. Do you see the huge difference between user growth and revenue growth (remember 711%)? That's just the start for SeaMoney but it shows the vast potential.

One of the reasons is cross-selling, just like MercadoPago has done and is continuing to do, for example, with MercadoCredito. From Sea'spress release:

In Indonesia, which has the most comprehensive set of products and services among our markets, over 20% of the quarterly active users have used multiple SeaMoney products or services in the fourth quarter. We view this as a highly positive indicator of the strong efficiencies we can leverage in bringing new offerings to our large and fast-growing user base on the Shopee and SeaMoney platforms, which are both highly synergistic with one another and enjoy a strong flywheel effect in the scaling of each platform.

Again, I should add that this is just the start. More and more products will be added in more and more markets. Again from the press release:

We also expanded various products offerings including credit services to consumers and merchants across more markets, started offering services in digital banking and insurtech in Indonesia and obtained a bank license in the Philippines.

That was new for me too. I didn't know that Sea already had a banking license in The Philippines. This is very interesting. The Philippines are another big market that is growing fast. I also didn't know that it started with insurtech in Indonesia. Sea now has banking licenses in Singapore, The Philippines and Indonesia (through the acquisition of Bank BKE) and has applied for one in Malaysia.

Shopee Brazil could launch SeaMoney (usually commercialized as ShopeePay) in a few years and other Latin American countries could follow. So there is still a ton of optionality.

Summary of the outlook

While some things look frightening without context, I think you should focus on what Sea is building over the long term. It has the financial power to continue to expand its reach. Yes, Garena is now back at 2020 levels, but that's not too bad. Shopee and SeaMoney have grown so fast that they can now use their scale advantages more and more. Shopee in Southeast Asia should be EBITDA positive this year already and SeaMoney next year.

Forrest Li on the conference call:

As a result, we currently expect that by 2025 cash generated by Shopee and SeaMoney proactively will enable these two businesses to substantially self-fund their own long-term growth.

We believe that we have the financial resources required to grow the two businesses to the inflection point without having to heavily rely on cash generated from the digital entertainment business. Of course, any additional growth from Garena will further strengthen our position.

I think that this should give investors confidence. After all, Forrest Li has executed outstandingly so far; why not believe him now?

Optionality

The most important thing about Sea is that it still has so much optionality. Opportunities abound. Don't forget that the company has SAIL, which stands for Sea AI Labs. It spends a lot on R&D there. Who knows, it may come up with a version of Upstart's AI for loans? It would definitely make sense. It could give its Shopee shoppers better recommendations, making them buy more. It could offer business software for its merchants to help them to sell better on Shopee. I'm tired of the overhyped term metaverse, but with gaming, AI, shopping and an integrated payment solution, Sea seems to be fully ready when it would take off too. I'm just thinking of some obvious ideas here, but there is a lot more.

There's also ShopeeFood, a food delivery service integrated into Shopee in a few markets. We probably all know that this is another very low-margin business, but if you can combine it with shopping (on Shopee) and grocery deliveries, it can be much more profitable, as Meituan has shown in China or Uber Eats shows for Uber (UBER). Just for the record, I'm not a fan of Uber's business model but if there is anything good about this company its the Uber Eats division, in my opinion.

And those are just two existing divisions of Sea. The company has tried out several things in the past. It tries things out and kills them fast when they don't work. They had a sort of business communication platform at one time, a bit like Slack, but it was shut down after a few months. They launched Shopee in France, they saw it didn't work and they shut it down after just five months. That's at least as important as innovation: knowing when to stop wasting money and Sea has a good track record there as well.

Valuation

This is the P/S ratio of the stock since the IPO:

As you can see, the valuation based on the P/S ratio is now almost at its lowest point ever, despite the fact that Sea is a much better and bigger company now, which means less risk.

If you look at Enterprise value divided by gross profit, it's even more apparent how cheap Sea has become.

If you divide Enterprise Value and Gross Profit, you see that Sea trades at an EV/GP of 12.48.

I recently used a few companies as examples in myTwilio valuation article. These numbers have changed a bit, so I have updated them.

Made by the author

Sea is expected to grow its revenue faster than all of these over the next three years. The consensus stands at 34%. I know that Sea has guided for 'just' 32% growth next year but I think this will prove to be very conservative, as Sea usually sandbags the guidance.

EV/GP shows what a companycouldmake, now or in the future. For the more mature companies, that's now, which means that their growth is slower. For younger companies like Sea, growth is still higher and you should expect profitability to only kick in later, as it's still growing fast. You want them to keep investing, but of course that growth must be sustainable. A company must have the means to fund its growth. With the cash that Garena still makes, the higher emphasis on profitability for Shopee and SeaMoney and Sea's big war chest of more than $10B, I don't think this is a problem. I believe Sea is cheap here.

Some might argue that the stock is still expensive because of the pandemic. But if we look at the pre-pandemic levels and compare to now, you see that the revenue and especially gross profit have gone up a lot more than the market cap.

There is risk in every investment and there is no denying that the uncertainties have grown recently for Sea:

* What about Garena's slowdown? Will that continue in the future?

* What about Free Fire in India?

* What about Shopee in India? Could it be targeted as well?

* What about Sea's relation with Tencent? Will it still be the preferred distributor of Tencent games in Southeast Asia after 2023?

Despite the fact that Sea has grown into my biggest position (I started buying at $54), I shouldn't be too emotional about this and acknowledge that the risks have indeed grown recently. It will probably remain my biggest position and I will keep adding to my position, especially at these low prices, but I just can't ignore the higher risks that have emerged in the last few months. But the path of every fantastic stock ever has been paved with worries. For Sea, this is no different.

Conclusion

Despite a good quarter, Sea's stock price keeps slumping. It's down 75% from its recent highs now. That has made the stock cheap, in my opinion, which, of course, doesn't mean it can't go down more over the short term. I'll keep scaling in slowly over time. I still strongly believe that this company will become a giant over time.

It now has as much chance, or maybe even more, to go 10x from here than when I picked it for my subscribers almost two years ago at $54. As long as it keeps executing, and these earnings again proved that, it will remain a very high conviction stock for the long term for me.

In the meantime, keep growing!