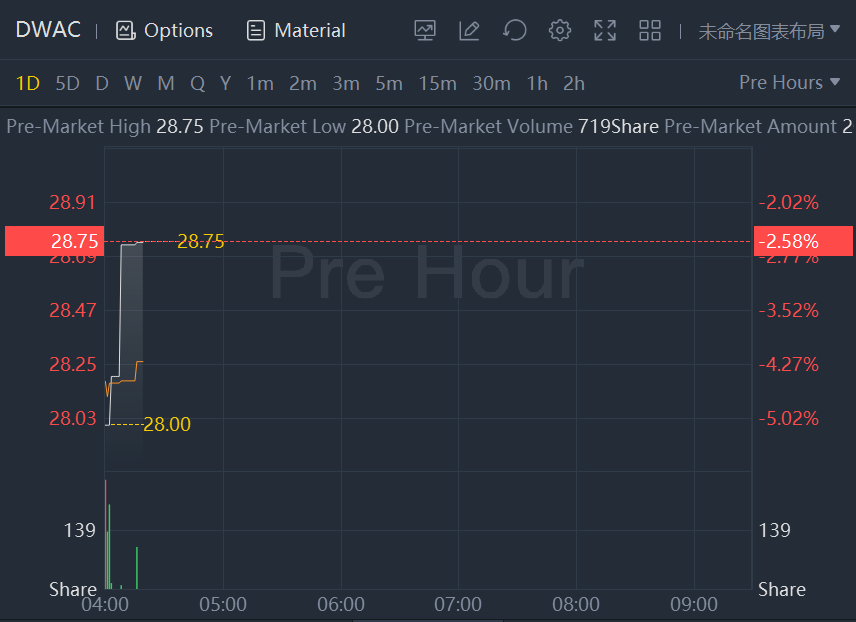

DWAC stock slid more than 2% in premarket trading as word of Trump media deal was said to have leaked months in advance, according to the New York Times.

Months before former President Donald J. Trump’s social media company unveiled an agreement to raise hundreds of millions of dollars last fall, word of the deal leaked to an obscure Miami investment firm, whose executives began plotting ways to make money off the imminent transaction, according to people familiar with the discussions.

The deal — in which a so-called special purpose acquisition company, or SPAC, would merge with Mr. Trump’s fledgling media business — was announced in October. It sent shares of the SPAC soaring.

Employees at the Miami investment firm, Rocket One Capital, had learned of the pending deal over the summer, long before it was announced, according to three people familiar with the firm’s internal discussions. Two of the people said that Rocket One officials at the time talked about ways to profit off the soon-to-be-announced transaction with Trump Media & Technology Group by investing in the SPAC, Digital World Acquisition Corporation.

A top Rocket One executive, Bruce Garelick, was on the board of Digital World until he resigned in recent weeks.

In the days before the Trump Media deal became public, there was a surge in trading in a type of security known as warrants, which entitled investors to buy shares of Digital World at a preset price in the future.

Federal prosecutors and regulators are now investigating the merger between Digital World and Trump Media, including the frenzied trading in the SPAC’s warrants, according to people familiar with the investigation and public disclosures. Digital World said in a recent regulatory filing that a federal grand jury in Manhattan had issued subpoenas seeking information about Rocket One, among other things.

The exact scope of the federal investigations remains unclear. Authorities have not accused anyone of wrongdoing, and representatives of Mr. Garelick and others denied doing anything improper.

A lawyer for Rocket One and its founder, Michael Shvartsman, denied that they had any advance knowledge of the merger between Digital World and Trump Media. He added that “any assertion otherwise is untrue.”

A lawyer for Patrick Orlando, who runs Digital World, declined to comment, as did representatives for the Securities and Exchange Commission and the U.S. attorney’s office in Manhattan.

Representatives for Mr. Trump and Trump Media did not respond to requests for comment. The company said in a recent news release that neither Mr. Trump nor Devin Nunes, the former California congressman who is the company’s chief executive, received grand jury subpoenas. (The release identified the men only by their job titles.)

The investigation into unusual trading in Digital World securities is the latest blow to Mr. Trump’s social media venture, which has struggled with technological problems and slow user growth.

Federal authorities are also investigating whether Digital World’s disclosures about the merger talks with Trump Media violated rules governing SPACs. And the Securities and Exchange Commission is considering whether to block the merger, according to regulatory filings by Digital World. If the deal doesn’t go through, it would deprive Trump Media of $1.3 billion.

There is scant public information about Rocket One, which has fewer than 10 employees and has made about 20 early-stage investments over the past decade, according to a review of archived web pages and an analysis by PitchBook, a data company. Rocket One disabled its website soon after its name appeared in a Digital World regulatory filing.

Two of the people familiar with Rocket One’s internal discussions said Mr. Garelick, a former Boston hedge fund manager who is now Rocket One’s chief strategy officer, mentioned the possible deal with Trump Media to some employees last summer. Around that time, a Rocket One employee was told to conduct a financial analysis of Digital World, including its warrants, one of the people said.

Carl Schoeppl, a lawyer representing Mr. Garelick, declined to comment. “We expressly reserve any and all rights to assert claims for defamation for any article that states, suggests, and/or otherwise implies that Bruce J. Garelick committed insider trading or any violation of the law,” Mr. Schoeppl said in an email.

Federal prosecutors and securities regulators are trying to determine why traders snapped up millions of warrants issued by Digital World days before the Oct. 20 announcement of the merger with Trump Media. Shares and warrants of Digital World surged the next day, with the stock rising 350 percent and the warrants soaring nearly 1,300 percent.

Digital World shares closed Monday at $29.51, well off the stock’s $97 high set in March, but well above its $10 I.P.O. price.

By merging with Digital World, Trump Media would gain access to about $300 million that Digital World had raised in its September I.P.O. The companies secured commitments from other investors to kick in an additional $1 billion if the merger is completed.

Trump Media’s sole product is Truth Social, a Twitter-like social media platform. Over the past several weeks, it has become the primary means for Mr. Trump to communicate directly with his supporters. Among other things, he has used Truth Social to blast the congressional committee that is investigating the Jan. 6, 2021, attack on the U.S. Capitol. With Mr. Trump banned by Twitter, the platform could grow in importance as the former president considers another White House bid.

In addition to the investigation into the unusual trading, federal authorities are continuing to investigate whether the leaders of Digital World and Trump Media started negotiating a potential merger before Digital World sold shares through an initial public offering in September. At the time of Digital World’s initial public offering, the company said in public filings that it had not yet identified a merger target. But The New York Times previously reported that talks between Mr. Orlando and Trump Media officials were already underway.

If Digital World didn’t disclose ongoing merger talks to investors, that would have violated S.E.C. rules.

The issuance of grand jury subpoenas usually is an indication that prosecutors are conducting a criminal investigation.

Among those who received subpoenas from the grand jury in late June were Wes Moss and Andy Litinsky (also known as Andy Dean), two former contestants on “The Apprentice,” the reality TV show that Mr. Trump hosted, according to people briefed on the matter.

Shortly after Mr. Trump left office, Mr. Moss and Mr. Litinsky pitched the idea of a Trump-branded social media company to the former president. The Times previously reported that they were involved in some of the early talks with Mr. Orlando.

Mr. Moss and Mr. Litinsky, who at one time were senior executives with Trump Media, didn’t respond to requests for comment. Mr. Litinsky no longer works for Trump Media; Mr. Moss’s job status is unclear.

Securities regulators also have asked for information from Digital World about the role played by the SPAC’s financial adviser, Shanghai-based ARC Group, according to regulatory filings. Federal regulators previously have reprimanded ARC. In 2017, the S.E.C. stopped ARC’s executives from listing shares of three companies, citing “material misstatements” in their securities filings and a lack of cooperation from the executives.