Morgan Stanley has signaled that the U.S. stock market correction is drawing to a close, yet the final hurdle may prove tough to clear.

On Sunday, April 12, Mike Wilson, Morgan Stanley’s Chief U.S. Equity Strategist, stated in his latest weekly note that the ongoing market correction has run deeper than most investors perceive. The S&P 500 is in the process of bottoming out, but the market remains at risk of retesting lows until issues surrounding interest rates and bond volatility are fully resolved.

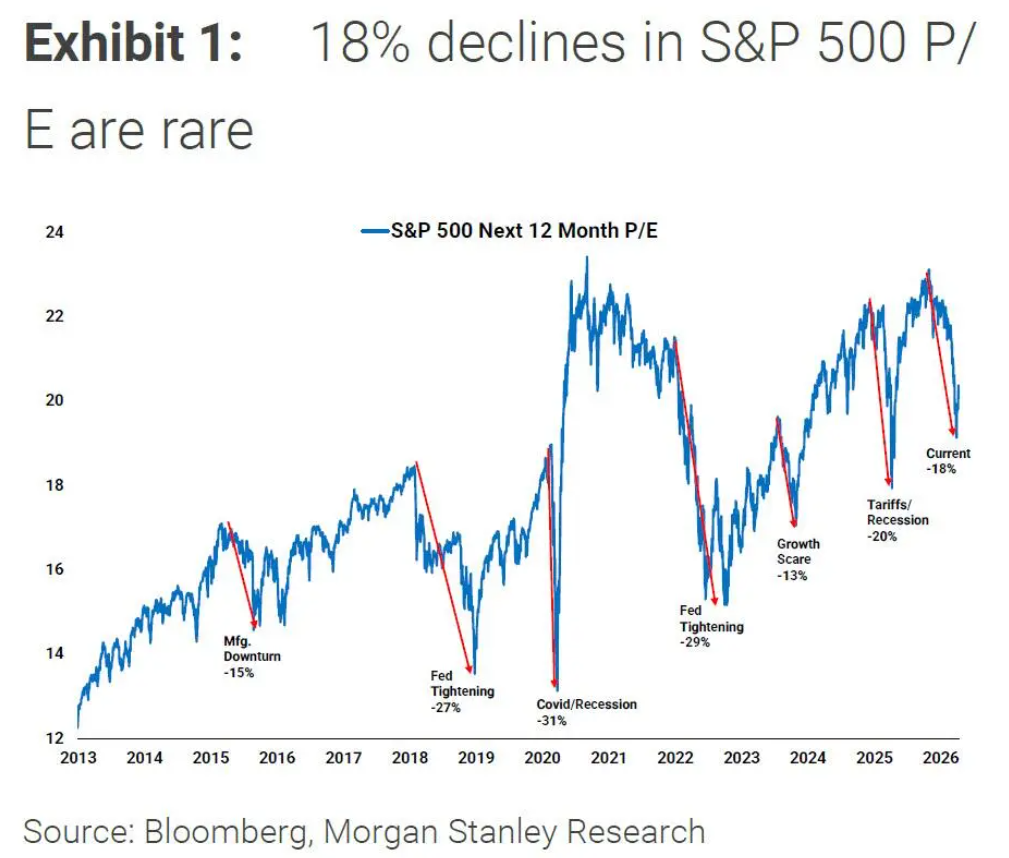

Wilson believes market sentiment remains fragile. He clarified that the current correction began last October, with the S&P 500’s forward price-to-earnings ratio falling 18% from its peak — a decline historically seen only during economic recessions or active Fed tightening cycles. “Neither scenario is in our base case,” he noted.

A Bull Market Correction, Not a Bear Market

Wilson maintains that this is a normal correction within a new bull market that started in April last year, following the bottoming of a rolling recession from 2022 to 2025, rather than a trend reversal.

The key justification lies in earnings. The S&P 500 has fallen less than 10% in price, while more than half of stocks in the Russell 3000 have dropped over 20%. Wilson interprets this not as market complacency, but as the market having reasonably priced in risks.

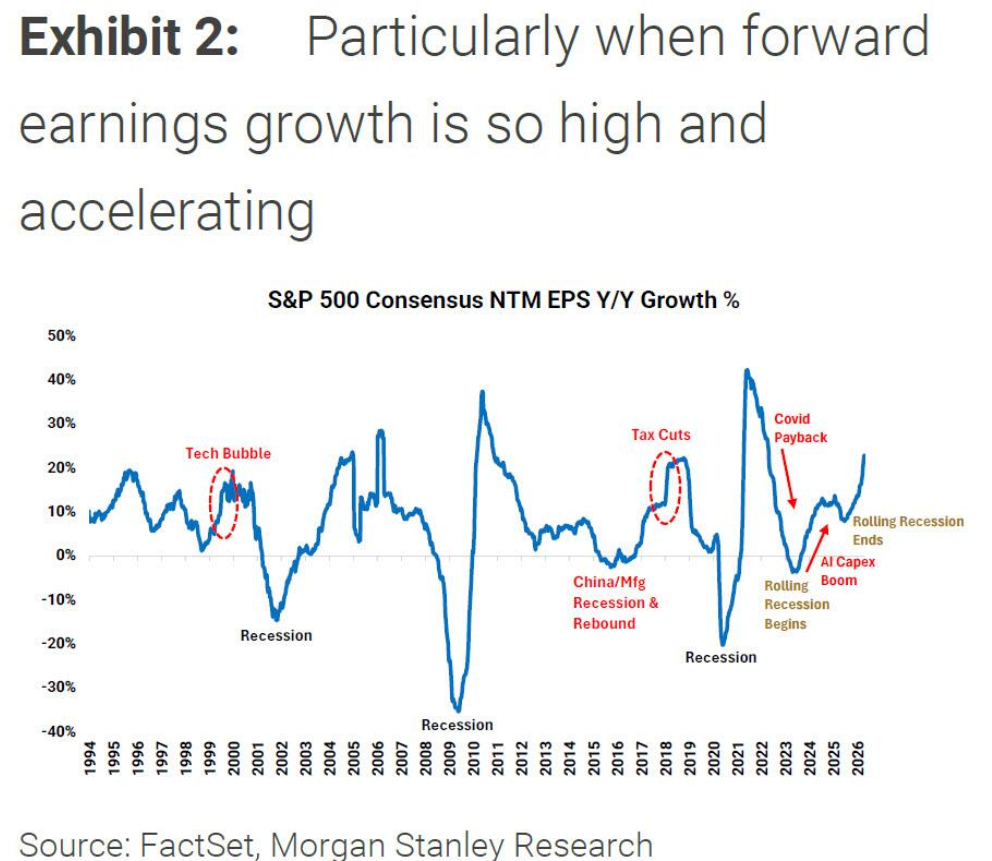

Supporting this view is a core data point: median company EPS growth is now in double digits, the fastest pace since 2021.

“Falling valuation multiples paired with improving earnings growth — this is a classic hallmark of a bull market correction, not a bear market,” Wilson wrote.

He also drew a contrast with historical oil shock episodes, when earnings were already deteriorating. Today, earnings continue to accelerate from high levels, and the rise in oil prices in real terms has been relatively modest.

Other Risks: Private Credit and AI Dislocation

Wilson also directly addressed two other major market concerns.

On private credit, he cited the view of his colleague Vishy Tirupattur: “Risks in private credit are material but not systemic.” Private credit has been tightening, yet direct exposure at most banks is limited, which may instead drive business back to traditional lenders.

On AI dislocation, Wilson argued that the narrative has outpaced reality. “Corporate adoption is still in early stages, and in the near term, AI is more likely to support profit margins than compress them,” he added. AI also gives companies justification to restrain hiring, creating upside surprises in operating leverage — one factor behind the current acceleration in EPS growth.

Final Hurdle: Interest Rates and the Federal Reserve

Wilson made clear that the biggest source of uncertainty for markets is interest rates and monetary policy, not geopolitics or credit risk.

The stock-bond correlation has turned sharply negative again, meaning rising interest rates have re-emerged as a headwind to valuations. He characterized the central bank’s hawkish pivot — driven largely by commodity inflation expectations — as “the final hurdle the equity market needs to clear.”

Last week’s partial rebound coincided with Federal Reserve Chair Jerome Powell adopting a more neutral tone and a decline in bond volatility.

“The final phase of a correction is never easy,” Wilson wrote. “Should interest rates or bond volatility rebound, the market may need to retest lows once more.”

Yet he emphasized that such volatility is part of the bottoming process, not the start of a new bear market. “Markets typically do not give investors multiple chances, which is why we advocate positioning ahead of time.”

Strategy Preference: Barbell Positioning

On tactical allocation, Wilson maintains a barbell framework:

One side consists of cyclical stocks with resilient earnings and compressed valuations, including financials, industrials, and consumer durables. The other comprises high-quality growth stocks — namely hyperscalers — where sentiment and valuations have reset to healthy levels.

His final verdict: “Most of the pricing adjustment for geopolitical risks, private credit concerns, and AI dislocation has already occurred. What remains is largely an interest rate and policy issue, which should be resolved as the Fed leadership transition is completed.”

“Markets always move ahead of the news, and investors should too.”