Summary

- NIO’s delivery growth continued to decelerate in May.

- While no longer negative, the delivery growth rate was just 4.7%, a disappointment.

- Due to continual supply chain problems, I am adjusting my prediction for NIO’s FY 2022 delivery possibilities.

With NIO (NYSE:NIO)'s delivery growth continuing to decelerate in May, shares of the electric vehicle company are going to have a harder time defending recent recovery gains. Although ET7 deliveries ramped up nicely inMay and ES6 production also rebounded, NIO's delivery results for May also presented further proof that the firm's rivals in the Chinese electric vehicle industry are executing better than NIO. I am also adjusting, for the second time, my outlook for NIO's delivery possibilities as my standing prediction of140 thousand units is no longer feasible!

Delivery growth continued to slow in May

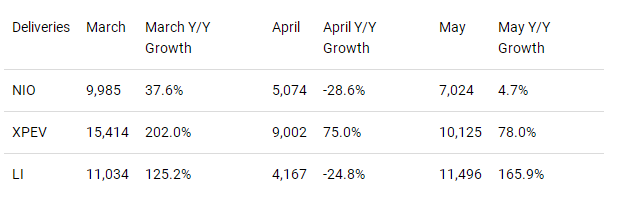

After NIO reported a 28.6% decline in its year over year delivery growth rate in April, NIO's delivery card for the month of May was better, but not by much. While delivery growth was positive, NIO's rivals executed once again much better than NIO and displayed much stronger delivery growth.

NIOdelivered7,024 electric vehicles in May, showing just 4.7% year over year growth. NIO delivered 2,936 ES6s, 1,635 EC6s and 746 ES8s, all of which are sport utility vehicles. Additionally, NIO delivered 1,707 ET7s, the company's new sedan model for which deliveries started only in March. In April, NIO delivered 1,878 ES6s and 693 ET7s, meaning delivery rates have ramped up 56.3% and 146.3% month over month. NIO's ET7 sedan deliveries now already exceed those of the EC6 which has seen deliveries commence in September 2020.

NIO's ES6 is NIO's best-selling electric vehicle product and it has been responsible for 40% of deliveries lately. Because NIO has now moved into the sedan market with its flagship ET7 electric vehicle and customer demand is strong, I expect sedan sales to account for an increasingly large revenue share going forward. Based on May delivery volumes, NIO's sedans accounted for a delivery share of 24.3% which is impressive considering that NIO started sedan deliveries only a little more than two months ago. The sedan share of deliveries was just 13.7% in April. Longer term, I see NIO growing its delivery share of sedan models to 40-50%, with the company's ET5 product launch later this year potentially accelerating this shift.

NIO's delivery card for May compared against rivals

NIO being outclassed by its rivals regarding delivery growth is a concerning problem and it could potentially result in shares of NIO underperforming its rivals going forward. Investors tend to purchase shares of those electric vehicle companies with the most attractive short term delivery prospects, and like I argued about a month ago, these companies are now XPeng (XPEV) and Li Auto (LI), but not NIO.

XPeng was the only electric vehicle company of the Top Three -- NIO, XPeng and Li Auto -- that had positive delivery growth in April while NIO and Li Auto saw their delivery growth rates go negative. In May, this picture improved, but chiefly for XPeng and Li Auto. While XPeng once again delivered impressive year over year delivery growth of 78.0% in May, Li Auto saw its deliveries soar 165.9% due to decreased production constraints.

NIO, unfortunately, delivered only about two thousand electric vehicles more than in the previous month, which calculates to a depressingly low delivery growth rate of 4.7% year over year. With the exception of Li Auto, XPeng and NIO's May deliveries were below those of March, the month in which production roared back after Chinese holidays earlier this year.

Calculating delivery estimates for companies like NIO which go through a volatile production ramp of different models at the same time is not an easy task. Just last month, I lowered my estimate for NIO's delivery possibilities in FY 2022 due to COVID-19 factory lockdowns that limited the availability of automotive parts and forced manufacturers to curtail production.

My previous estimate called for 140 thousand electric vehicle deliveries. Given the worrisome slowdown in NIO's delivery growth in May, there is no way the electric vehicle company can achieve anything near 140 thousand in deliveries. NIO delivered just 37,866 electric vehicles year to date which calculates to a 27% share of my previous FY 2022 delivery target.

Even when making generous assumptions about the current ET7 ramp and the estimated ET5 production start in September 2022, the April and May delivery cards have shown that NIO will likely deliver materially less than 140 thousand EVs this year. Due to continual supply chain issues and part shortages that are more severe than initially expected, I now expect NIO to deliver only 115-120 thousand electric vehicles, implying a 14-18% decline compared to my previous prediction.

Risks to refreshed FY 2022 delivery guidance

NIO doesn't give delivery guidance for the full year, and there are a lot of good reasons for that. Many variables affect delivery ramps that are outside of a manufacturer's control, so any guidance that goes just beyond the next quarter represents an unwarranted risk and subjects the stock to volatility. NIO will submit its first-quarter earnings card next week and delivery estimates for Q2'22 are likely to be weak. An additional delivery slowdown or problems with the sedan ramps could further hold back NIO's shares in 2022.

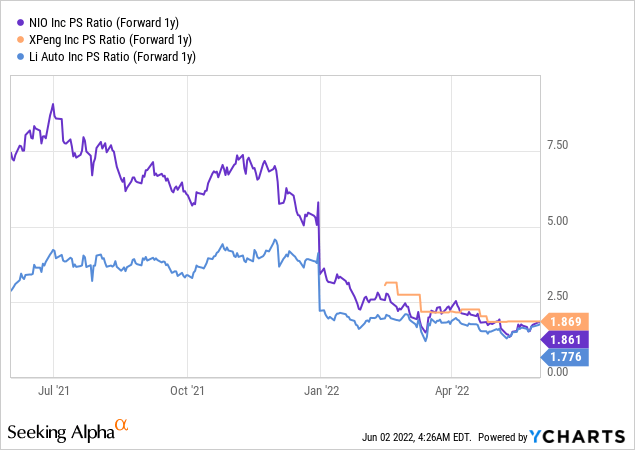

Cheap for a reason

NIO's shares are now trading at a much lower sales multiplier factor than last year and the reason is likely the massive change in NIO's short term delivery prospects. Other factors may also impact NIO's pricing, such as surging consumer prices and the conflict in Europe. Given a deteriorating delivery outlook, I believe shares of NIO will have a hard time moving higher, especially if NIO's Q2'22 delivery guidance disappoints next week. NIO, with a P-S ratio of 1.9 X, is now about as cheap as XPeng and Li Auto.