Summary

- Shares of Splunk crashed more than 30% since the start of November, a reflection of weakening investor sentiment towards growth.

- The company's Q3 earnings results came in well above expectations.

- In particular, Splunk continued a healthy pace of ARR growth as the company continues to make progress on its subscription transition.

- Valuation looks attractive at ~6.7x FY23 revenue, considering historical averages in the low teens and a current ~40% y/y pace of growth in ARR.

When the markets are running for the hills, intrepid and opportunistic investors should take a deeper look and see if there's a bargain to be had. Such is the case with Splunk (SPLK), a one-time Wall Street darling and a machine-data intelligence software company that has fallen sharply from favor over the past few months, alongside other growth stock peers.

Splunk, as many investors are aware, has long been one of the core big data plays in the enterprise software arena. Its technology helps businesses track and analyze machine-generated data - in other words, information generated automatically by devices on a network. Investors loved the big-data angle up until the pandemic began: at which point, Splunk decided to pivot its business to a subscription model, making near-term financials murky. With investors piling into remote-work and e-commerce stocks in 2020 and 2021, Splunk got left in the dust.

Recently, a new spate of weakness has kicked in: since the start of November, shares of Splunk have fallen ~30%, which matches the stock's 2021 performance - a huge underperformance versus the S&P 500's ~27% gain.

Dissecting the recent drop; the bull case remains vibrant

Broadly speaking, the decline in Splunk shares were driven by two factors:

- Q4 guidance for revenue came in at $740-790 million (representing -1% to +6% y/y growth), well below Wall Street's $834 million (+12% y/y) expectations

- CEO transition: Doug Merritt, who had led the company since 2015, stepped down suddenly, with no replacement named yet to date. Graham Smith, the company's board chairman, is filling in temporarily as CEO

Let's address the first issue first: recall that Splunk is heavy in the midst of a subscription transition. For investors who are unfamiliar with the mechanics of how this works, the simple way to understand this is that deals that were previously structured as one-time, upfront license fees are now being split over longer periods of time. Even though Splunk will derive greaterlifetimerevenue from these new subscription contracts, near-term revenue will suffer. In fact, the more customers Splunk can switch to cloud, the worse revenue will be in the short term. As we'll discuss in the next section, Splunk's cloud mix has spiked tremendously in the third quarter, leading to a cut in the near-term revenue forecast for Q4. In other words, it's primarily subscription strength, and not go-to-market weakness, that is eating into near-term revenue estimates.

On the CEO front: while I'll acknowledge that the departure of Merritt, who was a growth and sales-oriented leader who previously led field operations before being promoted to CEO in 2015, is a loss for the company, leadership shuffles tend to get resolved relatively quickly and produce a stock price bump when they do. I'd argue that the ~30% decline in Splunk's shares since the start of November is quite enough of a discount to compensate for any added risk that comes with the leadership transition.

In my view, I consider the bullish case for Splunk to be very much alive. Here's a refresher on the key points that investors should be aware of:

- The use cases for Splunk are infinite.In its early days, Splunk's machine data-mining capabilities were often used for security purposes to flag and respond to anomalies within corporate systems. But as Splunk has evolved, the company's machine data capabilities are applicable across virtually any industry and across many functions.

- Usage-based pricing.Some of the most successful software stocks are usage-based, meaning that revenue climbs proportionally to a customer's usage of the product. Splunk's platform is charged on a data volumes/computing power basis. As data volumes continue to explode and companies continue to push the boundaries of how they integrate data into operations and decision-making, Splunk has a tremendous opportunity to derive growth from within its install base.

- Splunk isn't without competitors, but the company's focus on machine data is unique. It's also the largest company in the space.The company's closest large/public peers are the monitoring companies like Datadog (NASDAQ:DDOG) and New Relic (NYSE:NEWR), which primarily focus on monitoring the performance and uptime of applications and infrastructure. Splunk focuses on visualizing and analyzing machine data (information passively generated by computers, phones, and other endpoints within networks). We note as well that Splunk's ~$2.5 billion annual revenue scale makes it nearly three times larger than its next-closest competitor, Datadog.

- Industrywide recognition.More to the point above, it's fine to have competition when Splunk also is widely considered the best-in-breed vendor for machine data analytics. Gartner, the software industry's leading analyst and reviewer, has bestowed the "Leader" designation to Gartner in the security information and event management space, and also named it as the vendor with the highest ability to execute. These commendations don't come lightly to IT buyers when making a purchase decision.

- Significant international expansion opportunity.Splunk has become a global brand name, and it's time for Splunk to chase more opportunities overseas. Currently, only about ~35% of its revenue base comes from international markets (and an even smaller ~20% slice of the cloud business is overseas). I see significant opportunity for Splunk to expand its presence outside of the U.S.

The bottom line:I'm remaining bullish on Splunk, and the recent slice-down in the company's share price makes me even more confident in a near-term rebound. I think a continuation of strong ARR growth will help to overturn the "weak Q4 guidance" narrative, while a near-term CEO resolution should also drive a relief rally. Stay long here and buy the dip if you're not already invested in Splunk.

Q3 download

Let's now go through Splunk's latest third-quarter results to demonstrate that fundamentally, the company hasn't committed any major faux-pas. The Q3 earnings summary is shown below:

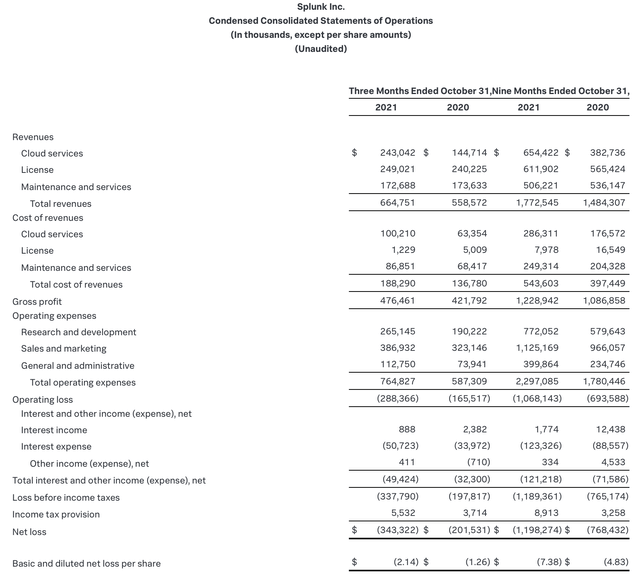

Figure 1. Splunk Q3 results

Splunk's total revenue in Q3 grew 19% y/y to $664.8 million, beating Wall Street's expectations of $646.6 million (+16% y/y) by a three-point margin. As previously mentioned, however, revenue growth is an incredibly shaky metric to rely on when Splunk is in the middle of a multi-year business transformation to favor subscription and cloud deals.

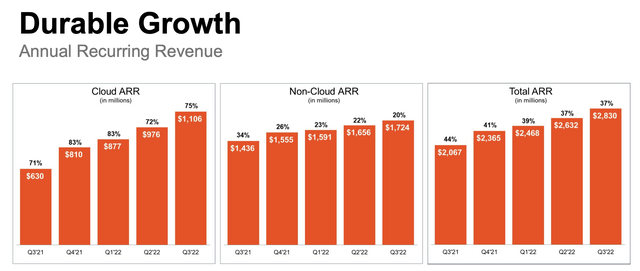

Instead, investors should look primarily to how Splunk's ARR, or annualized recurring revenue, is shaping up. We note that on a total basis, in Q3 Splunk added roughly ~$200 million of net-new ARR (the biggest sequential increase in ARR since the prior Q4, which tends to be a big quarter for software deal signings in the industry). Total ARR grew 37% y/y, and we note that the $2.83 billion in ARR that Splunk currently has already covers the overwhelming majority of Wall Street's current $3.01 billion revenue consensus for FY23 (in other words, revenue outlooks may be poised to shoot higher over the course of this year). Cloud-based ARR, meanwhile, soared 65% y/y to $1.11 billion:

Figure 2. Splunk ARR trends

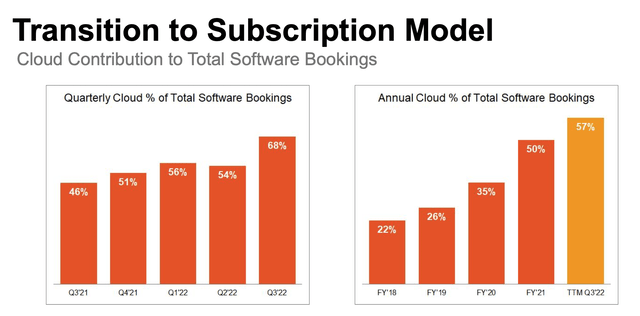

Also as regards the cloud: note that in Q3, Splunk's contribution of cloud to total software bookingsspiked to 68% of bookings,up sharply from a mid-50s contribution over the past several quarters. This is the driving reason why Splunk lowered its revenue outlook for the year: a greater mix of cloud versus traditional bookings means near-term revenue will decline.

Figure 3. Cloud bookings mix

CFO Jason Child's prepared remarks during the Q3 earnings call regarding the Q4 guidance further substantiates that cloud strength is the primary driver behind the outlook (key points highlighted):

Turning to guidance.The demand environment remains strong, and customer engagement is excellent, especially for existing customers planning their hybrid deployments, as you can see in our higher cloud mix. We believe cloud momentum will continue, and we're now expecting approximately 70% mix in Q4, higher than we previously expected. Based on this, we're increasing our cloud ARR target to between $1.325 billion and $1.35 billion at year-end, while our total ARR target remains in the $3.085 billion to $3.135 billion range.

On the income statement, the cloud transition continues to drive variability in our revenue and operating margin results.With significantly higher anticipated cloud mix in Q4, revenue growth will be tempered, just as we've seen in several prior quarters."

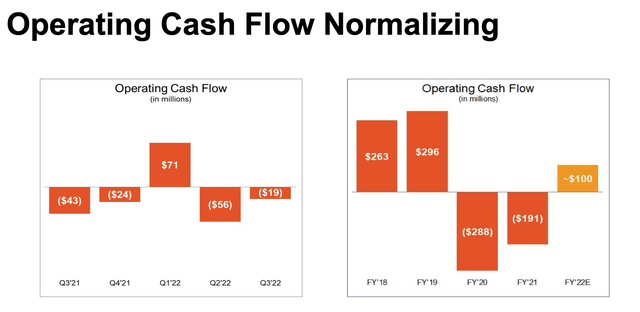

One other positive highlight to note: now two years into Splunk's cloud transition, cash flow is also beginning to normalize (switching to a subscription business model also hits cash flow, as deals that were normally paid for upfront get deferred over longer periods of time; in the end, however, this transition should help Splunk drive more consistent and less lumpy cash flows). The company is expecting to generate $100 million of positive OCF this year, after two straight years of cash flow burn:

Figure 4. Splunk OCF trends

Valuation and key takeaways

At current share prices near $116, Splunk trades at a market cap of $18.66 billion. After we net off the $1.65 billion of cash and $3.10 billion of debt on Splunk's most recent balance sheet, the company's resulting enterprise value is $20.10 billion.

For next fiscal year FY23 (the year ending in January 2023), Wall Street analysts expect Splunk to generate $3.01 billion in revenue, representing 18% y/y growth (note also that by year-end, Splunk has guided to $3.9 billion in ARR, though it has not yet guided to revenue). Versus Wall Street's revenue target, Splunk trades at just 6.7x EV/FY23 revenue- which, considering Splunk's massively applicable product and its wide-open market opportunity, its ~40% ARR growth, and successful ongoing cloud transition, is quite a bargain.

Stay long here and buy the dip.