Summary

- Further uncertainty for Sea Limited's Garena as its QAU did not stabilize as expected. New games were launched in recent months.

- Shopee’s race to profitability has accelerated as shown in the material improvements in unit economics, and they are expected to be profitable by FY23.

- SeaBank's credit business is growing strongly and its overall credit business is profitable and cash flow positive. Its revenue now makes up 10.4% of its overall revenue.

- Execution has been on point in attaining profitability although that resulted in declining growth in FY22. Management believes growth can reaccelerate once it achieves profitability.

- Sea Limited has sufficient cash reserves to pay off the convertible notes.

Investment Thesis

Sea Limited has come under much scrutiny in the past 2 years as the shift in focus from growth to profitability and macro headwinds have led to a massive growth decline across itsShopee and Garena units. While this is unfortunate, management has executed brilliantly so far to turn the company into an increasingly self-sufficient business in the near term.

In this article, I attempt to dive deeper into itsQ3 2022 resultand provide an overall analysis of the earnings. Although I’d like to highlight that the management has explicitly stated that growth can reaccelerate after attaining profitability and that they have a sufficient cash reserve to pay off the convertible notes sitting on the balance sheet.

Garena

SE 10-Q

SE 10-Q

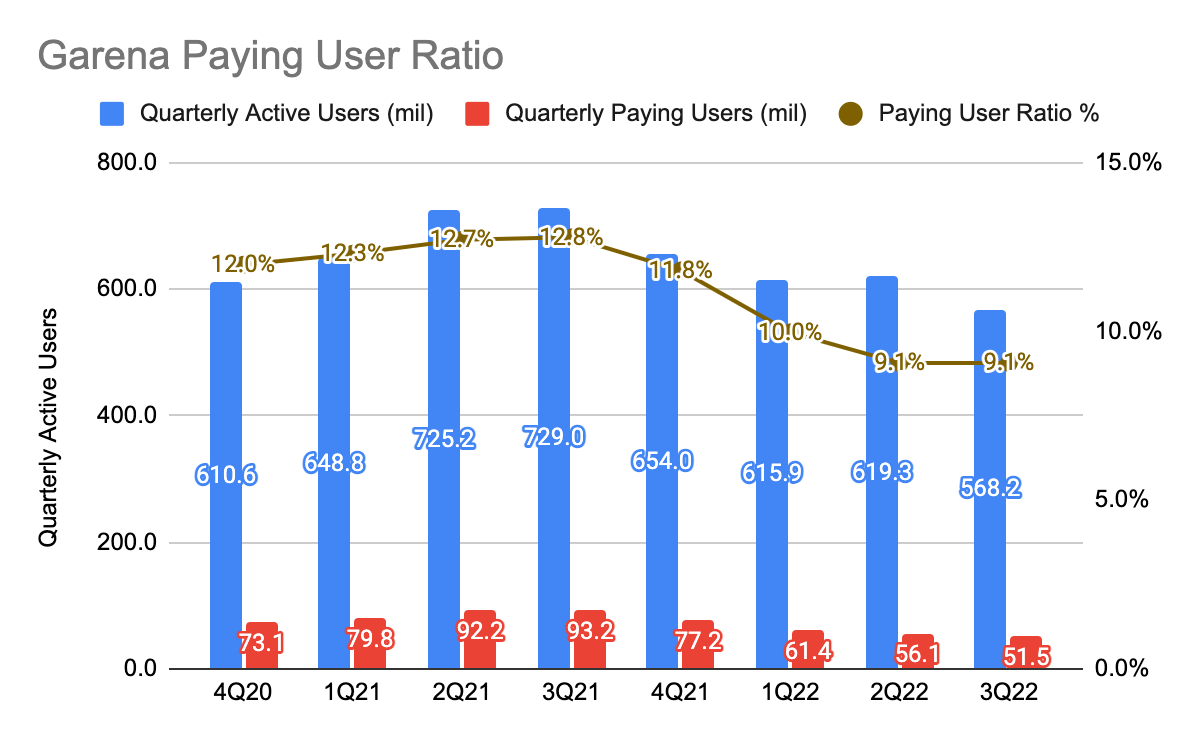

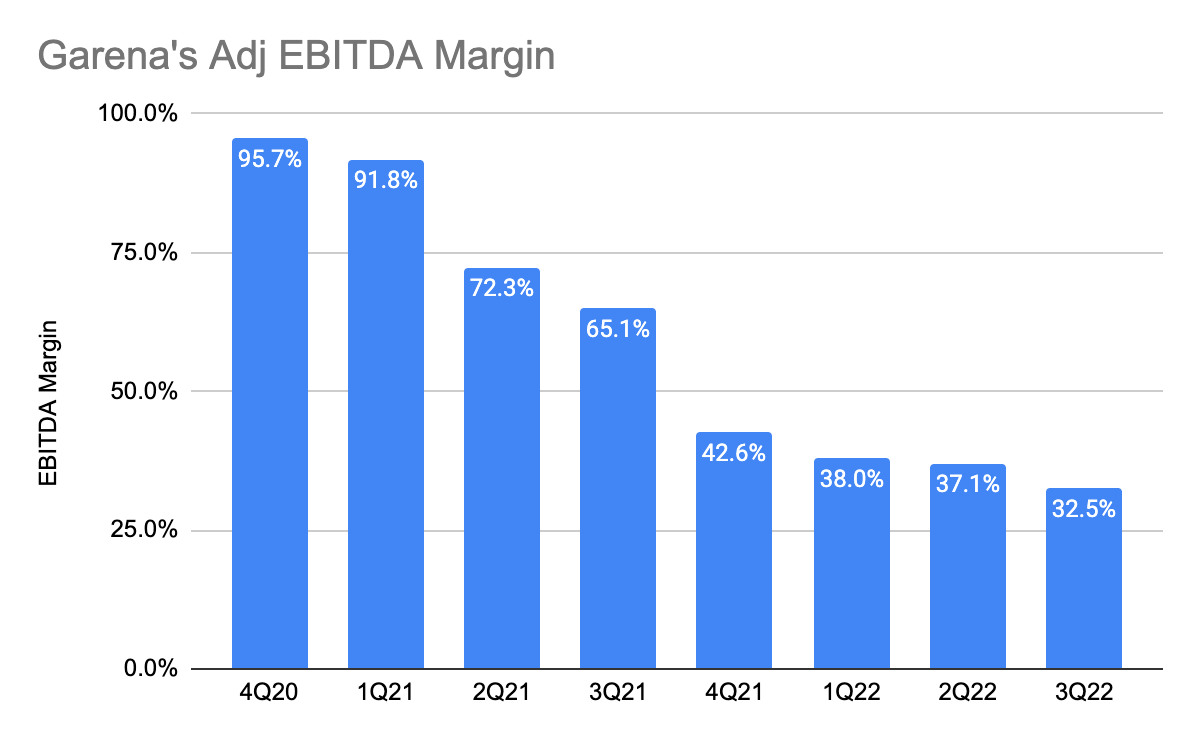

Garena’s QAU and QPU continued to decline sequentially, as the management’s anticipation of its user base stabilizing did not materialize. The macro headwinds continue to be a headache, and it seems that there is more uncertainty lying ahead for Garena Free Fire. The key forward is to focus on launching new games, with games such asPrimitive EraandBlack Clover Mobilelaunching recently. While this indicates that management is working hard to reaccelerate Garena’s growth, it is important to recognize that the success of games is not guaranteed, and this is the bigger uncertainty for the business. As a result, this caused its adjusted EBITDA margin to further decline to 32.5% during the quarter.

Additionally, management states that the expiry of the agreement with Riot Games will have no impact on Garena’s publishing business, and Garena is seeking other top-game developers for their publishing business.

Shopee

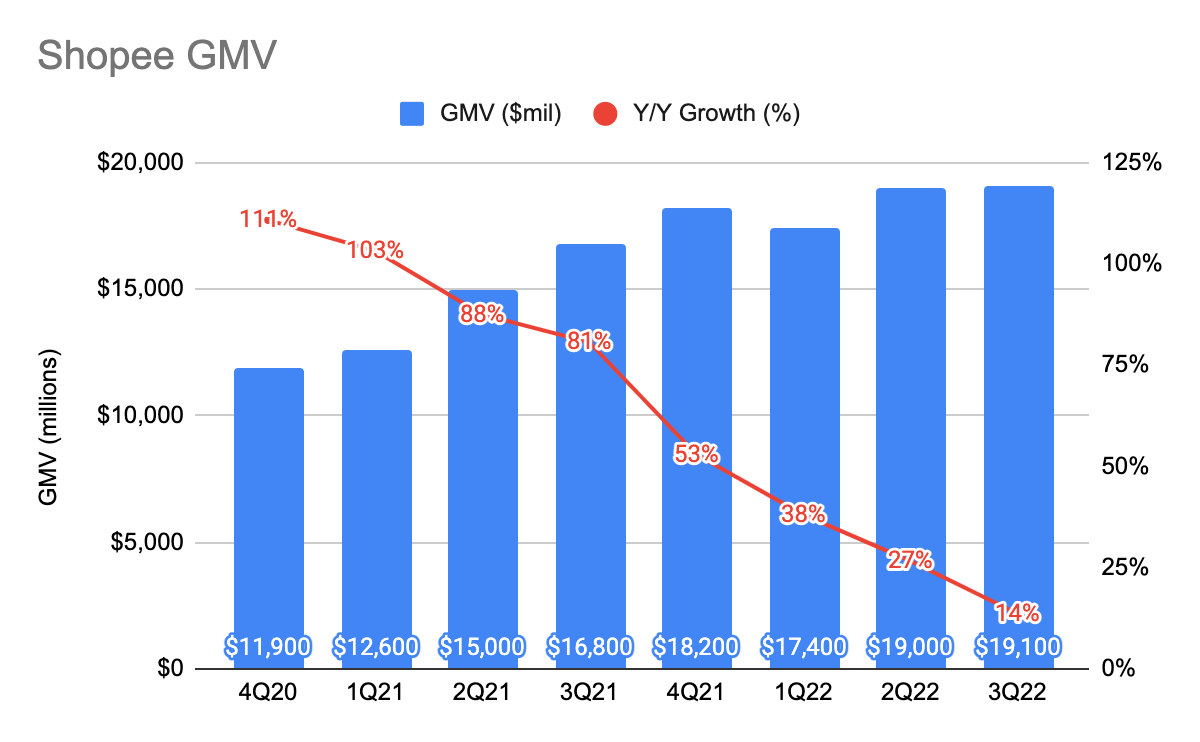

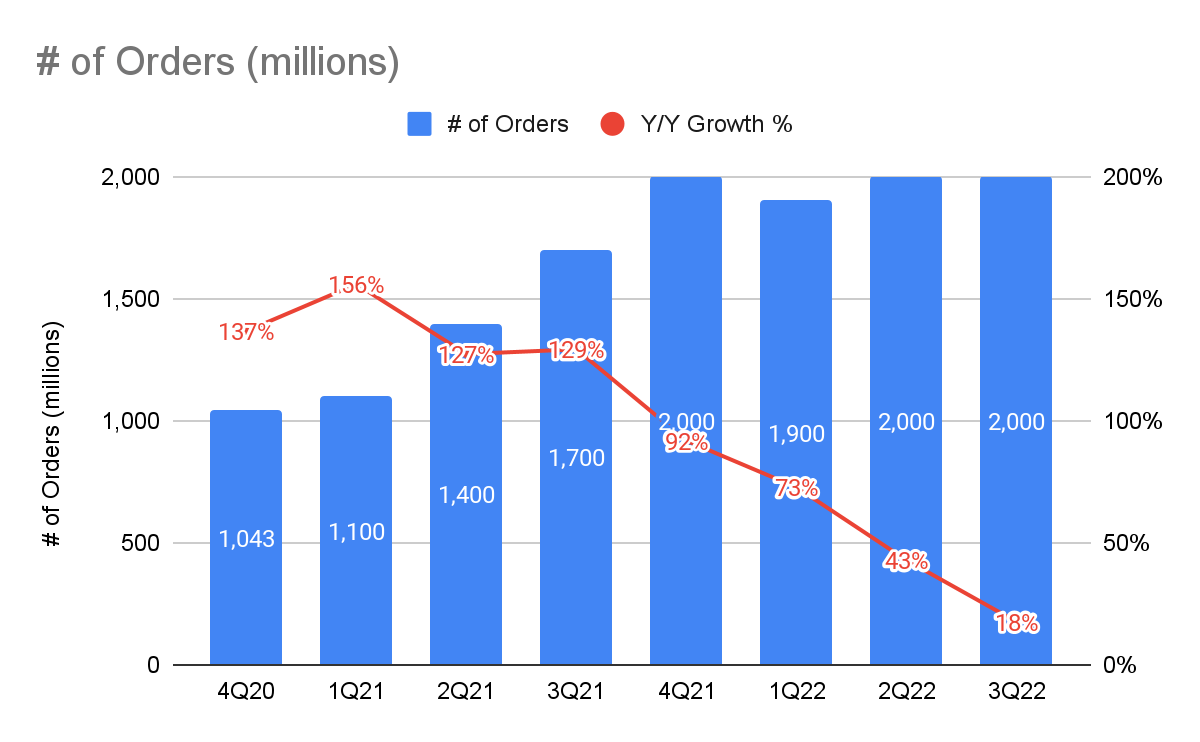

Shopee’s GMV grew 14% Y/Y and the number of orders grew 18% Y/Y, a continuous decline in the past couple of quarters. This is a result of management pulling back on its sales and marketing (“S&M”) expenses, exiting multiple markets, cutting costs aggressively (such as hiring), and lastly, the lower consumer discretionary spending. This is in contrast to Lazada (NYSE: BABA), as the number oforders declined Y/Yand they are also prioritizing profitability through increased monetization.

While this does show that consumers continue to spend on Shopee in SEA, its GMV and number of orders are partially contributed by Shopee Brazil. In a tough macro environment, Shopee experienced a 36% Y/Y growth in the number of brands on the platform, indicating that Shopee is an increasingly important partner in growing its online revenue.

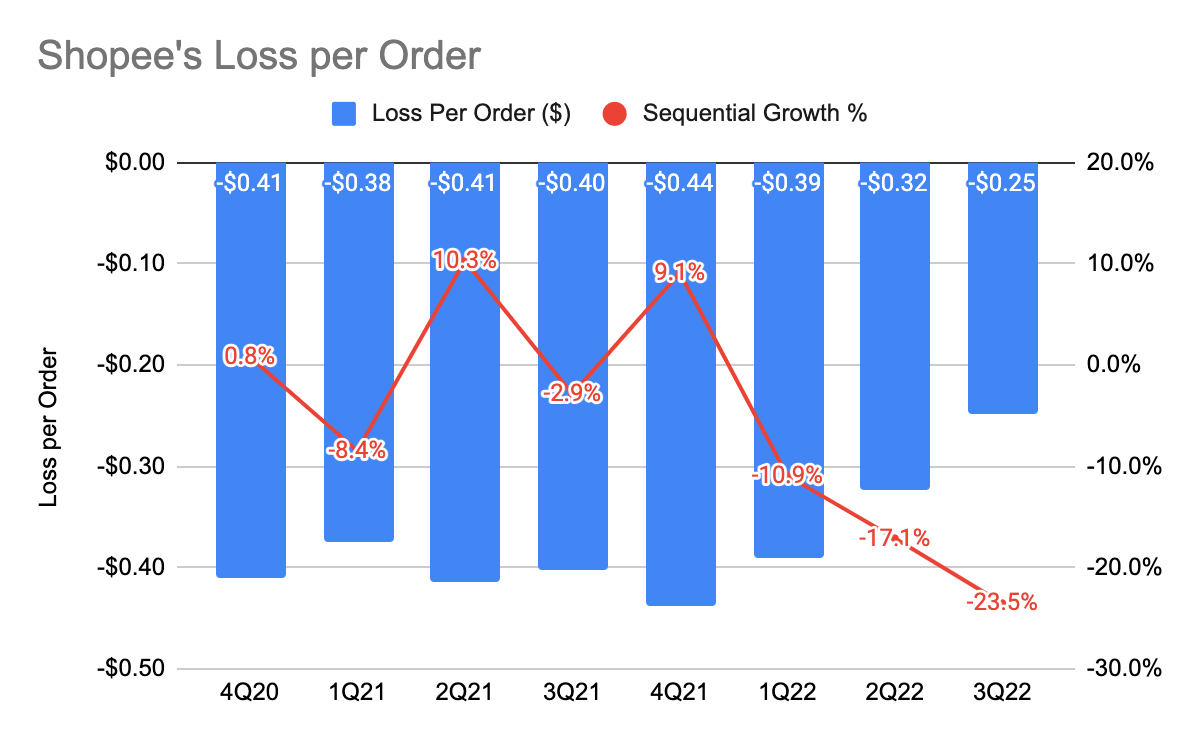

The more important portion is Shopee’s improvement in profitability. Its overall adjusted EBITDA loss per order continues to improve by 23.5% sequentially, and more specifically, Shopee Brazil’s loss per order improved by 27.5% sequentially during the quarter as compared to 6.6% in the last quarter. Moreover, Shopee is expected to attain profitability by FY23 instead of FY25 as previously guided by the management. This goes to show that the management has made great strides in pursuing profitability, which is impressive in my view. Once it attained self-sufficiency, growth can reaccelerate, although, the management is expecting flat or negative growth in certain metrics in the near term.

SeaBank

Note that I will be using “SeaBank” and “SeaMoney” interchangeably.

SE 10-Q

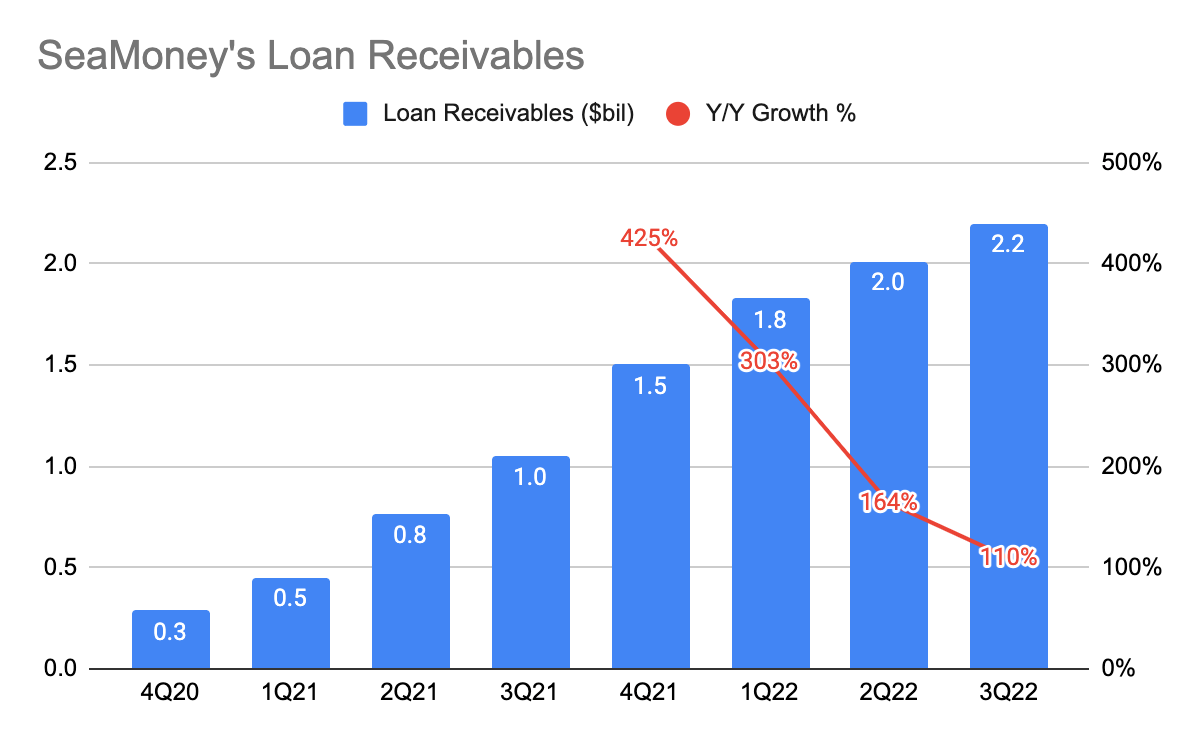

SeaMoney’s loan receivables grew 46% from 4Q21 and 110% from 3Q21 to $2.2 billion. These are loans provided to customers whereby SeaMoney generates revenue by charging interest rates, and it has been growing quickly. In myprevious article, I showed that in Sep 2022, SeaBank Indonesia grew its loans and customer deposits by 111% Y/Y and 147% Y/Y, respectively, and the launch of ShopeePay in Brazil. During the earnings call, management stated that the credit business is profitable and cash flow positive, and it will be focusing on growing this business in Southeast Asia (“SEA”) and Brazil.

Additionally, they have also said to diversify their source of funding for the credit business, which I believe is to seek third-party financing partners to reduce the capital required for the business and at the same time, reduce credit risk. Similar to Bank Jago (IDX: ARTO), SeaBank may utilize the data of its partners to help improve the non-performing loans and scale its lending. Readers who are unaware of SeaBank’s business model can head to mydeep diveinto the company.

SE 10-Q

SE 10-Q

SE 10-Q

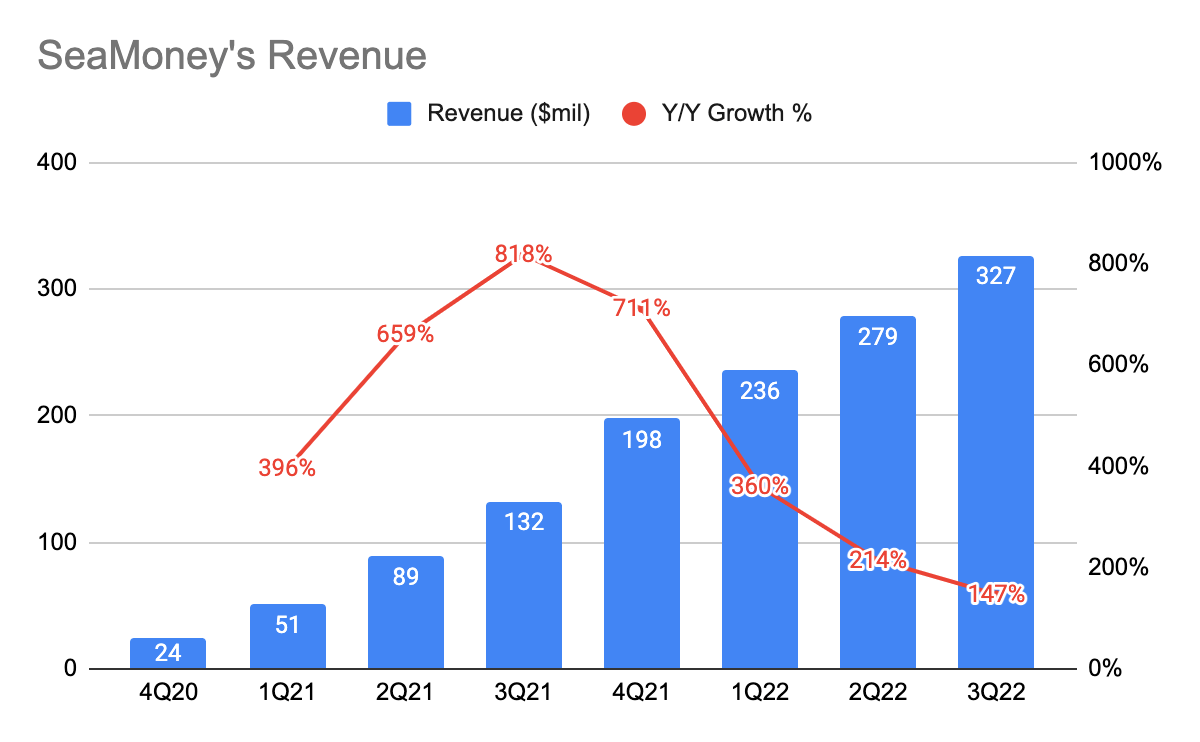

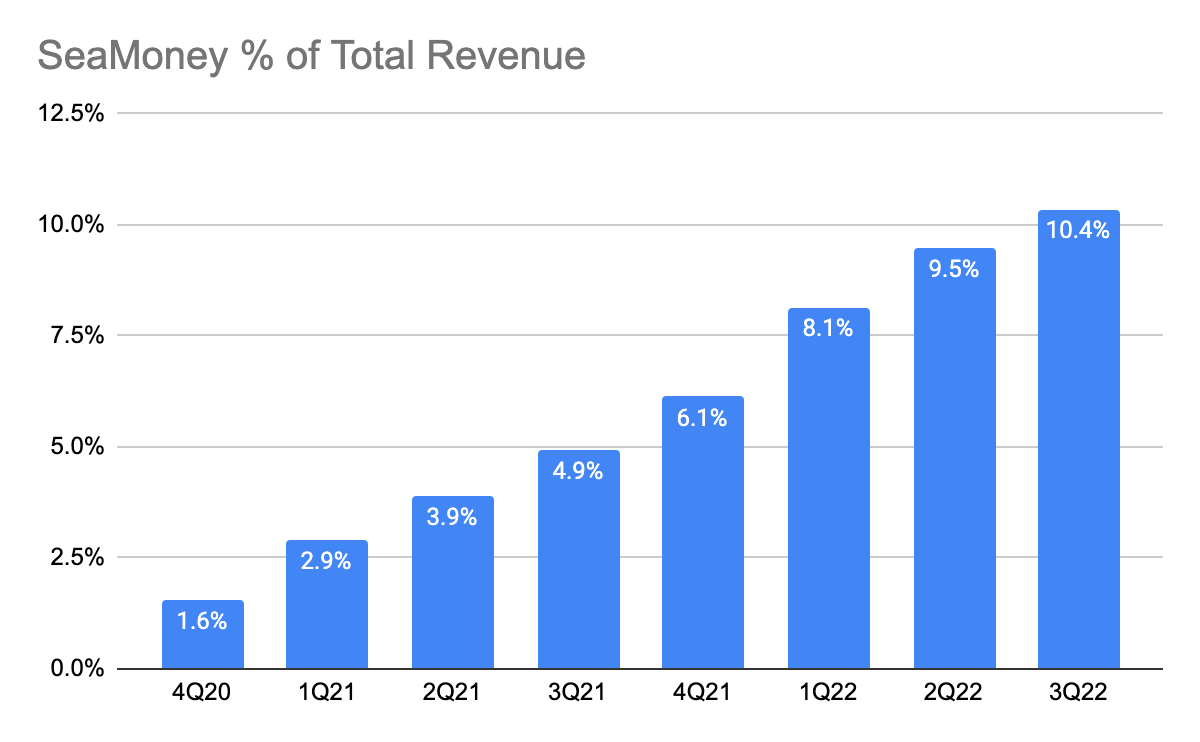

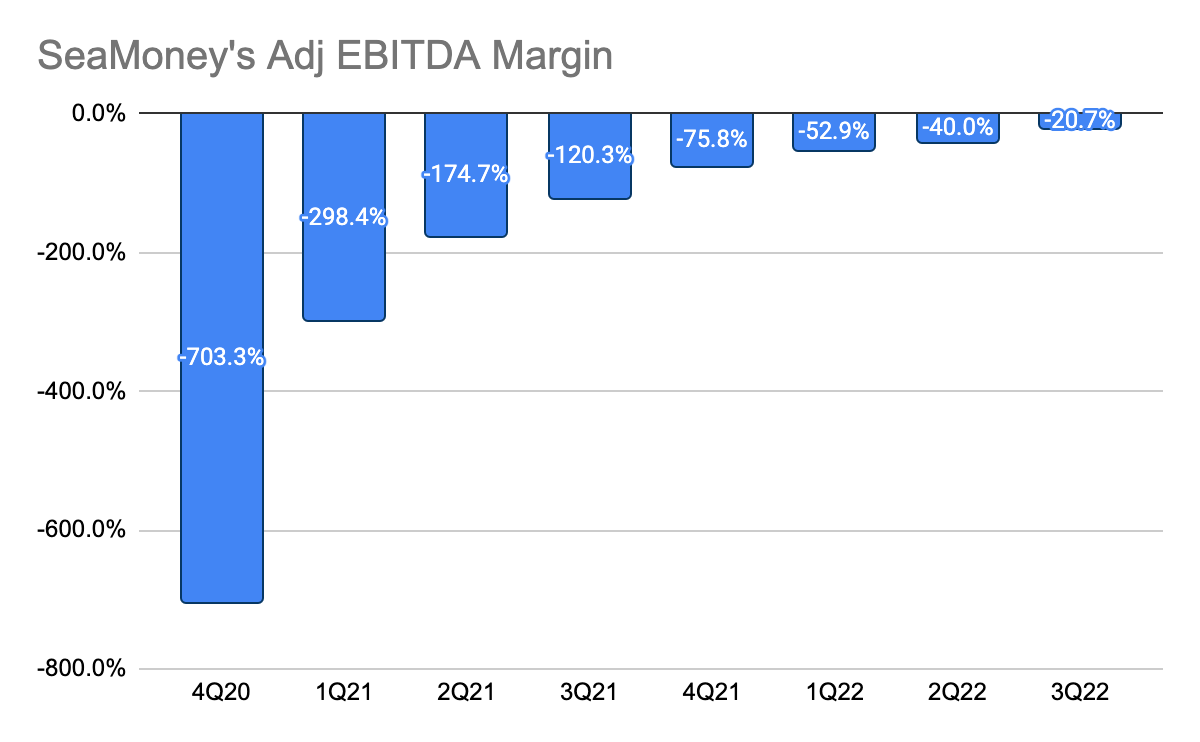

As a result of its growing deposits and loan books, its Q3 2022 revenue grew 147% Y/Y, and it has been increasingly making up a bigger portion of its overall revenue at 10.4% this quarter. Management had also been deliberate in cutting down on S&M expenses and combined with its acceleration revenue growth, its adjusted EBITDA margin has improved massively to -20.7% during the quarter. This is compared to -40% in 2Q22 and -120.3% a year ago.

Sufficient Cash Reserves To Pay off Convertible Notes

SE 10-Q

One of the biggest concerns about Sea Limited for investors is the cash burn rate, as they fear that the company does not have enough sufficient cash reserves to pay off convertible notes maturing in 2026. However, not only did the cash outflow slow in Q3 2022, but the management has also hinted that there are sufficient cash reserves to pay off the convertible notes:

“We aim to continue to maintain a net cash position, after budgeting for the full retirement in cash of outstanding convertible bonds and assuming no external funding.”

Conclusion

Overall, this was a pretty decent quarter for Sea Limited, as we could see that they had made huge improvements on the road to profitability, particularly for Shopee. While that comes at a growth trade-off, management has indicated that Shopee can reaccelerate its growth after attaining profitability in FY23, which is pulled forward from FY25 as guided previously.

Garena's results continue to be a concern as macro seems to have a longer-than-expected impact on its user base and its profitability as a result has been trending downwards over the past couple of quarters. Management has been working hard on its gaming pipelines, although the uncertainty lies in the successes of these new games and whether they could reaccelerate their growth in the future.

SeaBank has been growing its top line really quickly and huge improvements were made on the bottom line as well. Furthermore, the overall credit business is profitable and is generating positive cash flow, and has been increasingly making up a larger proportion of its total revenue. I continue to believe that this can be a potential growth driver for Sea Limited.