Summary

- Alibaba and Amazon have both seen a significant slowdown in top line growth post-pandemic.

- Near-term revenue outlook favors Amazon. Amazon Web Services outperforms Alibaba Cloud.

- Based off of valuation, however, Alibaba appears to present investors with more upside.

In this article, I am going to compare the growth prospects, risks and valuations of the two largest e-Commerce companies on the planet: Alibaba (NYSE:BABA) and Amazon (AMZN). The shares of both e-Commerce companies have under-performed this year, in large part because of a post-pandemic slowdown in global economic growth and soaring inflation, which is impacting consumer spending. Both factors have created considerable uncertainty for the e-Commerce sector. With Alibaba's and Amazon's shares repricing 31% and 29% lower year to date, both companies have pros and cons. While Amazon has a couple of advantages, I believe Alibaba may be the better deal!

Top line growth is slowing

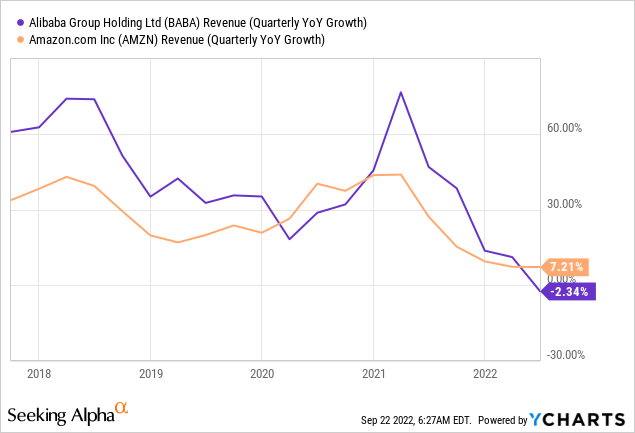

Both Alibaba and Amazon have seen a significant slowdown in top line growth in the last quarter as inflation headwinds and weaker economic growth after the pandemic impacted their businesses. Alibaba's revenue growth slowed to 0% (Alibaba's China commerce business actually declined 1% in FQ1'23), the worst performance on record for Alibaba, while Amazon's top line growth slowed to just 7% year over year in Q2'22, reflecting a 20-year low point for Amazon.

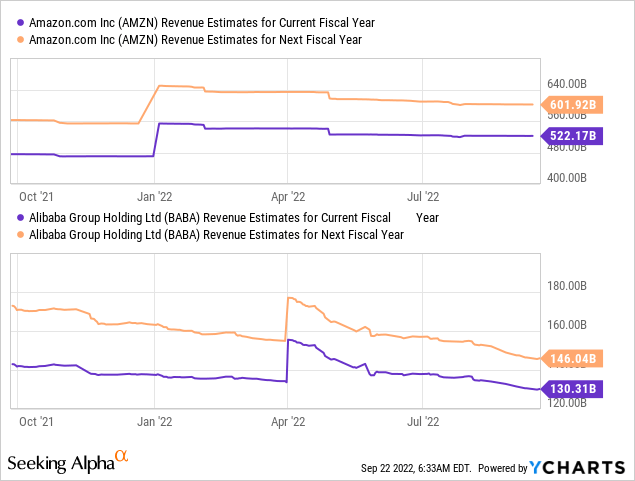

Regarding forward annual estimates, Amazon is expected to do better than Alibaba. Consensus forecasts call for Amazon to see revenue growth of 11% this year and 15% next year... while Alibaba is projected to grow its top line at rates of 2% and 13%. Estimates have also dropped more for Alibaba, indicating that the market is a bit more pessimistic about BABA than AMZN...

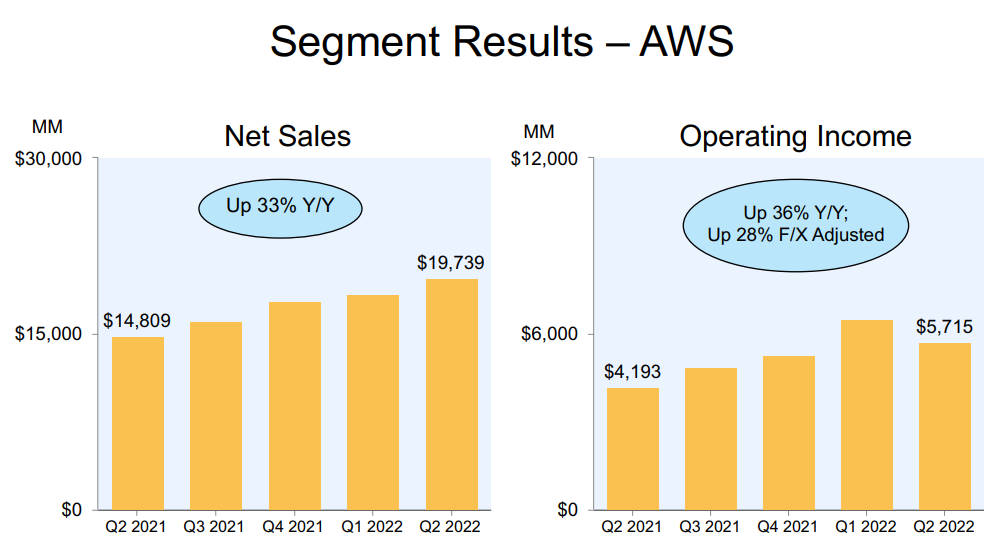

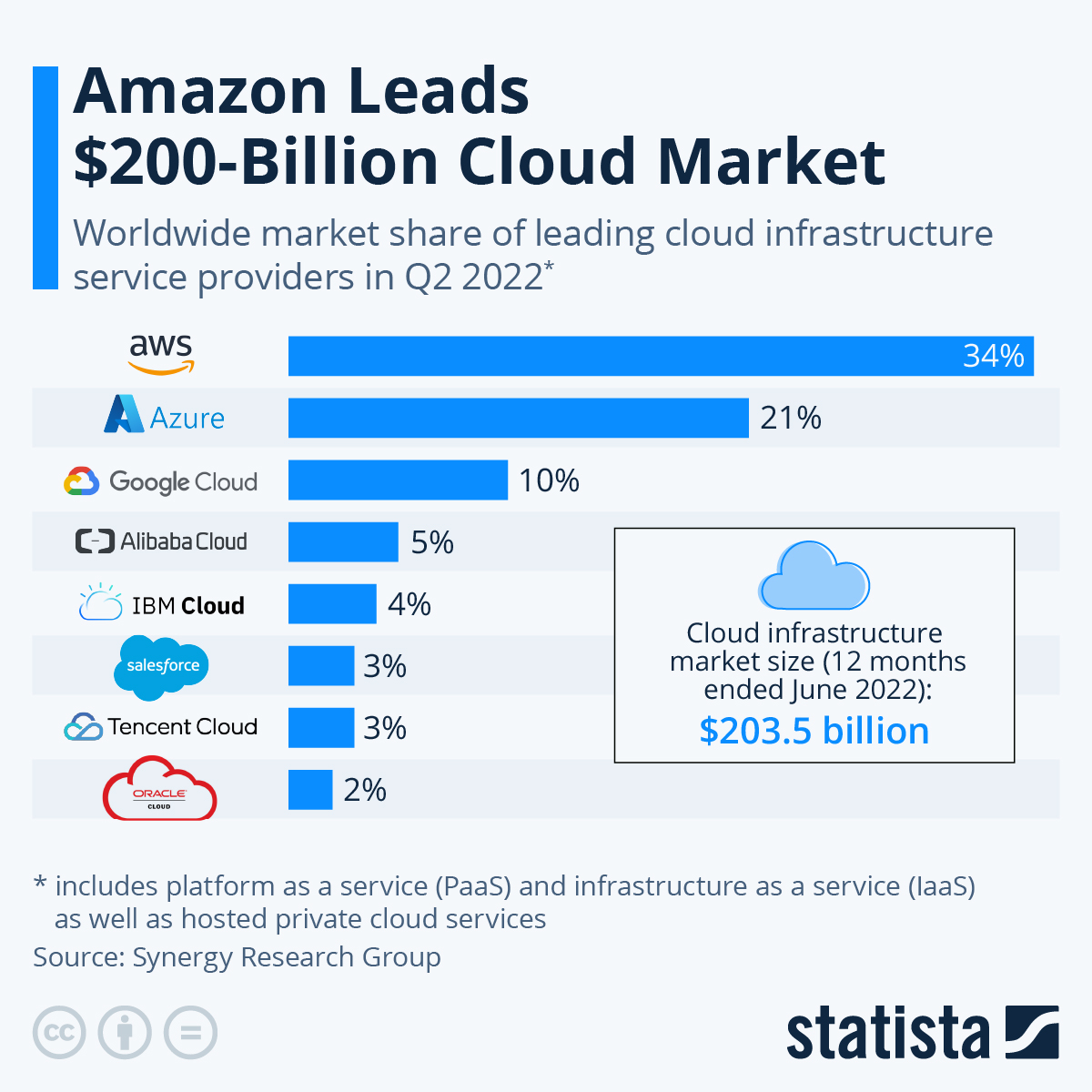

So not only is Amazon's Cloud business responsible for most of Amazon's top line growth, but AWS is also growing more than three times faster than Alibaba's Cloud segment. On top of that, Amazon has a significant advantage regarding market share in the Cloud market, with AWS ranking #1 and capturing a third of the global Cloud market. Alibaba was ranked a fairly distant fourth with a market share of 5%.

Amazon and Alibaba have both been highly valued during the pandemic because online retailers faced super attractive growth prospects at a time when the physical competition was all but taken out of the game by health authorities. The post-pandemic normalization of e-Commerce growth and the resulting re-rating of Amazon and Alibaba, however, have changed things up a bit.

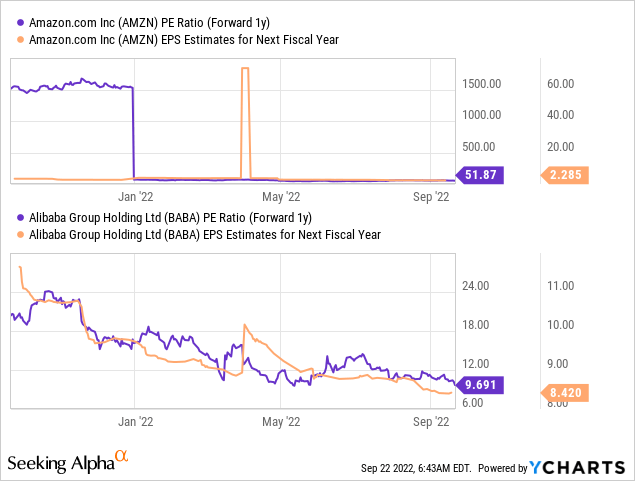

Amazon and Alibaba are both profitable and are expected to remain profitable. But a key difference has emerged regarding the firms' valuations. While Amazon is still expensive relative to its earnings potential (52 X P-E ratio), Alibaba is trading at a rock-bottom P-E ratio of 10 X... which represents stronger potential for an upside revaluation.

Risks with Alibaba and Amazon

Risks with Alibaba and Amazon

Both companies are facing deteriorating prospects in their core e-Commerce operations due to high inflation, which is impacting consumer spending. Amazon and Alibaba are both highly dependent on consumer spending, and both companies continue to be dominated by their e-Commerce operations (Alibaba's commerce share is 76% while Amazon's is 84%).

Besides top line risks which both companies share, there are other more company-specific risks that matter: Amazon is generating a large number of sales outside the US, meaning the retailer has exposure to the appreciating US Dollar. A strong US Dollar hurts currency conversions, which is a headwind for Amazon.

For Alibaba, there are regulatory and delisting risks that are affecting the pricing of its shares. I believe that a delisting of Alibaba's ADR from a US stock exchange is highly unlikely to occur because the firm secured a primary listing status for its shares in Hong Kong, which gives US investors an alternative marketplace to buy shares. Due to the primary listing status, Alibaba's shares are also available for mainland Chinese investors through the Hong Kong stock connect program.

Final thoughts

When comparing Alibaba and Amazon, there are many factors that must be considered. Both companies obviously are going through a post-pandemic adjustment period of slowing growth. Both companies are investing in the Cloud market and are facing challenges in their core segments.

Amazon has a stronger short term revenue outlook than Alibaba as it projects 13-17% revenue growth in the third-quarter, while Alibaba may actually see negative revenue growth in FQ2'23. Estimate trends favor Amazon as well. From a valuation perspective, I believe Alibaba wins the comparison, however, because the Chinese company trades at a fraction of Amazon's P-E ratio. The risk profile for Alibaba's shares is therefore much more skewed to the upside than Amazon's!