Summary

- NIO’s Q2’21 earnings card was impressive with revenues and deliveries growing by more than 100% during the pandemic.

- NIO’s losses are decreasing rapidly. The EV maker is expected to be profitable in FY 2023.

- NIO raised its outlook, now expects to deliver up to 25,000 vehicles in Q3'21.

- Beijing’s hardening crackdown on Chinese companies may affect the market’s confidence in EV makers like NIO.

Despite surging revenues, narrowing losses and a strong outlook for Q3'21, shares of electric vehicle start-up NIO(NYSE:NIO)dropped after earnings. NIO's business is gaining momentum and the EV maker does a great job executing on its business plan.

NIO continued to grow rapidly in Q2'21

Competition in the Chinese market is increasing and EV makers continue to ramp up production and deliveries. NIO,XPeng(NYSE:XPEV)and Li Auto(NASDAQ:LI) saw record deliveries for the month of July and all three companies are now delivering about 8,000 vehicles each month. NIO's delivery growth was not as strong as the growth rates of its direct rivals, but a 124.5% Y/Y delivery growth rate in July is hard to criticize.

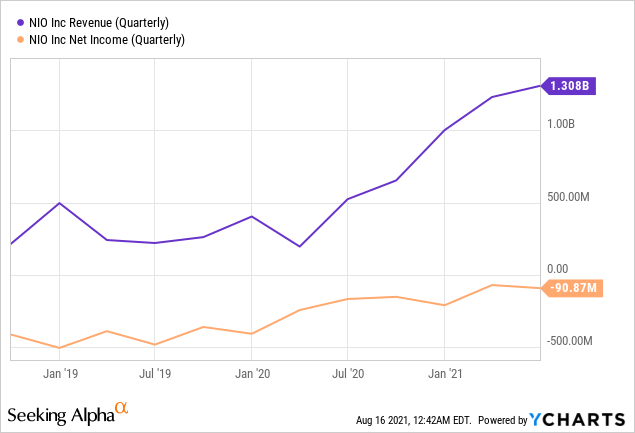

NIO is even harder to criticize after it revealed its Q2'21 earnings card last week… which showed soaring revenues and narrowing losses. NIO's second-quarter showed 127.2% revenue growth over last year as the company recorded 8.45B Chinese Yuan in Q2'21 revenues ($1.31B). NIO's revenue surge is linked to the production ramp up of its various sport utility vehicles, soaring delivery growth rates despite challenges posed by the Coronavirus pandemic, and a denser product mix.

In Q2'21, NIO delivered 21,896 vehicles of which 9,935 were ES6s, 7,528 were EC6s and 4,433 were ES8s. Total deliveries in Q2'21 surpassed Q2'20 deliveries by 111.9% as NIO was able to grow production despite a semiconductor supply shortage that limited factory output in the first six months of the year. NIO also revealed that it had a gross profit of 1.57B Chinese Yuan ($243.8 million) in Q2'21, showing 402.7% growth Y/Y. NIO executed its business plan very well over the last year and the growth in revenues, deliveries and gross profit is impressive.

However, NIO is still not profitable. But since the EV maker is still in the ramp up stage and prepared to enter the sedan market in 2022 with its new P7 sedan model, NIO perhaps should not be expected to make a profit yet. Factory output and delivery growth are two metrics that are far more important for NIO and other EV makers than net profits.

NIO's Q2'21 net loss was 587.2 million Chinese Yuan (US$90.9 million), but losses declined by 50% compared to last year's second-quarter. The loss per American Depositary Share/ADS was 0.42 Chinese Yuan which is the equivalent of 7 cents. NIO had a loss per ADS share of 1.15 Chinese Yuan (16 cents) in Q2'20. Estimates called for an 8 cent per ADS share loss on $1.28B in sales, meaning NIO's actual revenues were higher and losses were lower than expected.

NIO's revenues keep increasing while losses keep narrowing...

Outlook

NIO expects continual strength in its business as demand for electric SUVs remains high. For the third quarter, NIO expects to deliver between 23,000 and 25,000 vehicles as factory output increases and semiconductors start to see a better flow again. NIO's delivery range implies a minimum of 5% Q/Q growth in deliveries. I believe NIO could outperform its own delivery guidance if the semiconductor supply shortage eases and production choke points in Q3'21 are removed. Third-quarter revenues are expected to fall into a range of 8.91B Chinese Yuan ($1.38B) and 9.63B Chinese Yuan ($1.49B). NIO's guidance implies at least 96.9% Y/Y and 5.5% Q/Q growth in its top line.

The outlook is very strong, considering that competition in the EV market is increasing and that automobile production is still hampered by the semiconductor supply shortage. NIO may not be growing as fast asXPeng or Li Auto in the short term, but NIO's business results and outlook are impressive in many ways: Doubling revenues and deliveries during the pandemic year is an achievement in itself and NIO is on a clear path to profitability... if it continues to execute its business plan well.

NIO: It's all about growth

NIO is not profitable, and despite narrowing losses, profits should not be expected in the short term. NIO is estimated to reach profitability in 2023, which is beforeXPeng (2024) and after Li Auto (2022). Purely from a sales growth perspective, Li Auto may be the best as the EV maker has a much lower price-to-sales ratio thanXPeng and NIO.

XPeng is now more expensive than NIO, likely becauseXPeng is growing deliveries faster than NIO. However, NIO's battery-as-a-service subscription model and large investments in the expansion of its battery charging and replacement station network are set to boost NIO's revenue growth significantly this decade.

BaaS-related revenues could result in an additional $500M or more in revenues annually for NIO by 2025. NIO's battery subscription model is a key differentiating factor.

Market Cap |

FY 2021 Est. Revenues |

P-S Ratio |

FY 2021 Est. EPS |

P-E Ratio |

Est. Year of Reaching Profitability |

|

NIO |

$67.22 |

$5.41 |

12.43 |

-$0.54 |

- |

2023 |

XPeng |

$34.20 |

$2.32 |

14.74 |

-$0.72 |

- |

2024 |

Li Auto |

$25.94 |

$3.10 |

8.37 |

-$0.10 |

- |

2022 |

(Source: Author)

Risks with NIO

Despite strong business performance in Q2'21 and record deliveries, shares of NIO have retreated lately as the market adopted a 'wait-and-see' approach regarding China-based companies. This is because the Chinese government is increasingly assertive and has started to crack down on various sectors of the economy, specifically the E-Commerce, technology and social media sectors.

This accelerating government intervention is reducing the appeal of Chinese companies for US investors… although the risk of regulatory intervention in the electric vehicle market is low. Beijing promotes the adoption of EVs heavily and targets a 20% share of EVs by 2025… which makes it unlikely that the electric vehicle sector experiences the same crackdown as other sectors. However, Beijing getting more involved in the economy is not exactly helping the image of Chinese stocks in the US.

Additionally, companies that list on an American exchange indirectly through American Depositary Shares - like NIO - don't have to submit audited financial statements to a US regulator. This means that the market depends on unaudited financial statements and a good amount of trust when it comes to investing in China-based electric vehicle companies.

An interventionist Chinese government and the fact that China-based companies don't go through a rigorous process that makes sure that financial statements can be relied upon, are two big issues that may weigh on shares of NIO going forward. A de-listing of Chinese EV makers would be the worst outcome. In the case of a de-listing of China-based companies from US exchanges, NIO would become uninvestable. Right now, this is not the case and the risk of a complete de-listing is not high. However, if US-China relations deteriorate, NIO could face headwinds.

Final thoughts

NIO had a great second-quarter that saw soaring revenues during the pandemic, narrower losses and a strong outlook for Q3'21… with potential upside in factory output as the semiconductor shortage eases.

Losses are narrowing rapidly which means NIO could be profitable in FY 2023. Business performance is supported by strong execution and NIO will continue to grow rapidly. NIO's shares are a buy!