Banks on the line for deposit flows and margin pressure in Q1 updates as they reel from banking crisis. Furthermore, Provisions are expected to continue climbing in 2023, which will weigh on profits.

After the holiday weekend, Q1 earnings season kicks off in earnest with reports from some of America's largest banks. Bank earnings will offer clues as to the state of the banking system and the economy after the March episode of banking unrest.

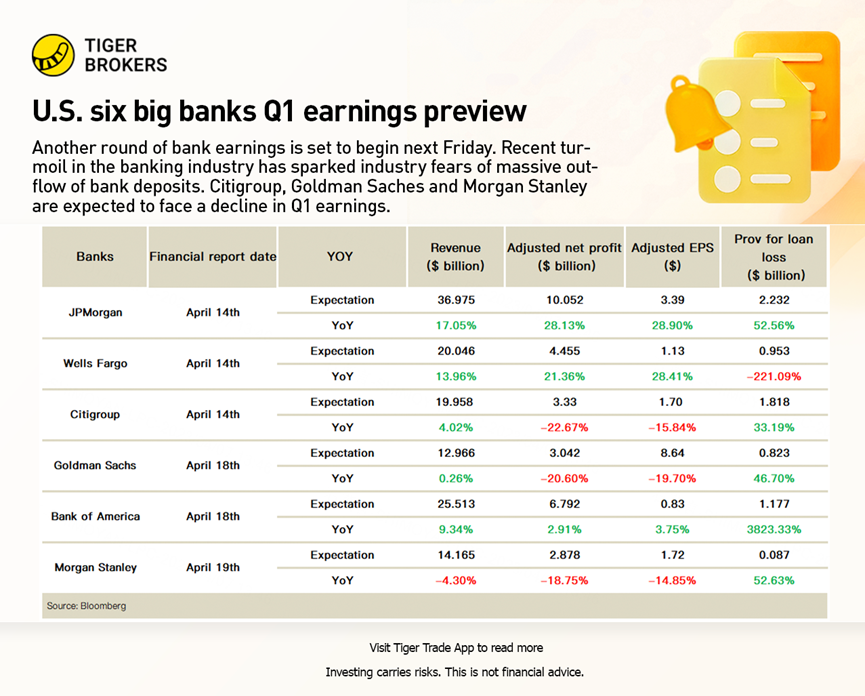

U.S. six big banks Q1 earnings preview

This is a critical earnings season for US banks. Nerves remain frayed following the crisis of confidence in regional banks sparked off by last month’s collapse of Silicon Valley Bank. Citigroup, Goldman Sachs and Morgan Stanley are expected to show an decline in adjusted net profit. While provisions are expected to fly higher except for Wells Farggo. JPMorgan, Bank of America, Wells Fargo, Citigroup, Morgan Stanley and Goldman Sachs are forecast to collectively put $7.09 billion aside in the first quarter.

Fears of contagion are easing for now, but traders and investors are still waking up in fear of hearing another domino has fallen, and the need to fix the cracks that have emerged in the banking system has still dramatically changed the outlook for bank stocks even if we are lucky not to see any more massive failures.

Though some bigger names saw deposits swell in the flight to safety following the regional banking turmoil, more money is flowing out of deposits into money-market funds. According to Bloomberg estimates, JPMorgan, Citigroup and Wells Fargo could have seen deposits shrink sequentially by a total of $63 billion for the quarter, a decline of 1.4% on average. Deposits at the largest 25 commercial banks fell by $90 billion in late March, according to Bloomberg Intelligence, and banks are likely to have to raise rates to compete.

Managements from JPMorgan, Citigroup and Wells Fargo could also give a more comprehensive picture of how empty downtown office buildings are hitting real estate lenders and investors.

What to watch in Q1 2023

Deposits and balance sheet strength

When US banks start reporting fiscal first-quarter results next week, what their executives say about deposit levels and liquidity will arguably be of greater interest to investors than any full-year profit guidance.

Regional banks faced a rush of withdrawals after the first bank failures since the last financial crash and markets are eager to know whether they are still seeing outflows of deposits or whether the situation is showing signs of stabilizing.

So, where did all those deposits go? There were reports that the largest banks saw an influx of deposits as clients moved their money into more financially-secure institutions, but it will be interesting to see just how much they attracted considering we have seen large sums flow into alternatives.

Ultimately, this earnings season will inform markets how strong, or fragile, the balance sheet of each individual bank is following the tumultuous events over the past month. Those that have stressed they can weather whatever storm is brewing have so far failed to convince the markets. Deposits, and the ability to cope with large-scale withdrawals, will be under the spotlight.

Loan loss provisions

Banks have already been building provisions that are set aside in case there is a rise in defaults on loans and the recent cracks in the system will only encourage them to build reserves at a faster pace now that talk of a recession has returned and because of tighter credit conditions and a more conservative attitude.

JPMorgan, Bank of America, Wells Fargo, Citigroup, Morgan Stanley and Goldman Sachs are forecast to collectively put $6.8 billion aside in the first quarter compared to just $2.8 billion the year before. Provisions are expected to continue climbing in 2023, which will weigh on profits.

Commercial real estate exposure

There has been much talk about the threat that the commercial real estate market poses to the banking sector. The outlook for many parts of the sector remains chellenging. Office demand is being tested amid the shift to hybrid and remote work. Demand for shop space is being confronted by businesses moving online, and even the boom for warehouses is waning. This, alongside the state of the wider economy, is testing property valuations.

With that in mind, there are fears that landlords and businesses will struggle to refinance their commercial property loans over the coming years. Interest rates are higher and will make the cost more expensive at a time when rental revenues are under pressure and banks are set to tighten their credit availability. The fact around 68% of all commercial property loans are held by the smaller regional banks rather than their larger peers only exacerbates the situation. Ultimately, it looks set to become more difficult and expensive. That raises the risk of default and of a meltdown in the sector causing havoc on the wider economy.