Summary

- Behind Amazon's most recent earnings "disappointment", which the company attributed to commerce returning to a resemblance of "normalcy", remains a steadily growing revenue behemoth.

- Amazon Web Services, a cloud service, should not be overlooked. It has already achieved $59B in annualized revenue run rate and is growing nearly 40% YOY.

- One may reasonably project that Amazon Web Services, as a stand-alone company, will be worth >$1 trillion within a few years.

- Like twenty years ago, Amazon is evolving again, but the market has not yet fully appreciated the company's cloud services revenue growth prospects.

- Amazon's stock has been flat for the past year. Now is a great time to initiate or accumulate a position in Amazon before its valuation reaches, once more, for the skies.

Amazon Is Evolving Again

Amazon's(NASDAQ:AMZN)history, from its beginnings as an online bookstore to it becoming the #1 retail giant, is one to marvel at. But in case you missed out, no worries: it is continuing to happen. Amazon is always evolving. This article will focus on Amazon's next great frontier: the cloud.

A Flat Amazon

Amazon's valuation has been flat now for over a year. The company continues to grow its e-commerce operations internationally, but slipped, most recently, after reporting disappointing Q2 '21 revenue.

The company attributed the miss to life returning to normal.

I think the impact of people getting vaccinated and getting out in the world, not only shopping offline, but also living life and getting out.

It takes away from shopping time. It's good -- it's a good phenomenon and it's great, and we just have to appropriately gauge our run-rate going forward.

Brian Olsavsky

In the grand scheme of things, the ($2B) revenue surprise means nothing to long-term investors. It is merely a grain of sand on a seashore. It certainly doesn't justify a noticeable slice in valuation, yet here we are.

Amazon is a bit unusual in that whilst it has grown into a massive enterprise, it remains very much a growth stock (as evidenced by ~30% YOY revenue growth, seemingly endless optionality, and a higher P/B value).

The beginning of the pandemic saw Amazon's valuation nearly double within just a few months of time, as the inevitable e-commerce tailwinds gusted.

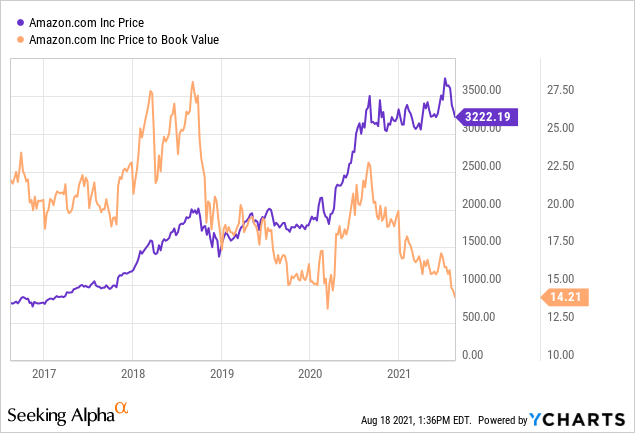

Zoom out and the trajectory, however, which most notably started in 2015, remains very clear:

Over the past five years, Amazon's Price to Book Value has averaged ~20. As of now, it is 14. Assuming Amazon continues to hover around this average, there appears to be a lot of upside from current prices. It is more safe and reasonable, however, to project an increasingly lower P/B value with time, as one would expect a company's growth to slow down. In such event, plenty of opportunity still remains in an Amazon investment.

All in all, things are still, very much, looking up. So, buyer beware: Do not go off chasing the so-called "next Amazon".Amazon is the next Amazon. And like any great company, they are always innovating. Just as Amazon evolved from an online bookstore to an immersive e-commerce giant, it is evolving again: into a cloud.

Enter The Cloud

Jeff Bezos' successor, Andy Jassy (current Amazon CEO), led Amazon's cloud services, known as Amazon Web Services [AWS], since its inception. Jassy succeeding Bezos highlights an obvious impending evolution of Amazon: from focusing primarily on physical goods (via its e-commerce efforts) to the inclusion of digital services (via AWS).

The cloud services market was estimated to be worth $312B in 2020 with the big players, Amazon, Microsoft(NASDAQ:MSFT), and Google(NASDAQ:GOOGL), comfortably eating half the market. The total addressable market is estimated to reach$1T in 2026.

If Amazon is able to retain 20% market share by 2026 (it currently stands ~25%), AWS, alone, can be a $200B revenue business per annum. 30% profit margins implies $60B in profits each year.

Think to yourself: how much would AWS be worth as a stand-alone company in 2026/2027, assuming my reasonable projections come to fruition? I am not going to dive into fancy financial numbers to attempt to come up with a valuation. Let's imagine anything >$1T would be a reasonable valuation. To reiterate: this is just for AWS alone.

Notice, Amazon has done it again. Between 1998 and 2008, Amazon was building something (its e-commerce platform) that would be worth in excess of $1T a few years later. They are doing the same with AWS (between 2006 and 2016). I suspect it will start bearing its fruit very soon.

Where Do You See Amazon Ten Years From Now?

As I am writing, Amazon's market capitalization is $1.64T.

Before considering an investment, one should think to themselves, "Where do I see 'Company X' ten years from now?" This puts things into proper perspective.

Where do you see Amazon ten years from now? Is it still worth $1.6T? Is it less? Is it more?

Amazon's main two revenue segments, e-commerce and cloud services, are still growing strong and expected to continue to benefit from major tailwinds. One, commerce continues its shift online internationally and, two, cloud services are replacing archaic ways of getting work done. It is very likely that Amazon will continue to appreciate in value.

So, where will it be ten years from now? Well, no one knows for sure. We can, however, reasonably project that Amazon will continue to outperform the broader US markets, which return, on average, 8-10% each year. It is also reasonable for Amazon's stock to, again, return 100% over the next 4-6 years.

Key Takeaways

- Amazon's evolution from an online bookstore to the world's largest e-commerce retailer has justified a valuation exceeding $1T.

- While the company continues to grow on its retail front, they are continuing to innovate and evolve. AWS, which began in 2006, is expected to net at least 20% of a $1T market by 2027.

- AWS, as a stand-alone, can reasonably be worth >$1T by 2027.

- The above article neglected to mention other foreseeable opportunities such as digital advertising, which is also likely to soon exceed $100B in annual revenue.

- Ten years from now it is reasonable to believe that Amazon will (1) remain a growing e-commerce giant, (2) retain at least 20% of cloud services, and (3) continue to grow its total revenue at a rate exceeding 20% YOY. These opportunities will likely justify a much higher valuation a decade from now.

- Risks include major competition in e-commerce (e.g. Walmart, Shopify) and cloud services (e.g. Microsoft and Google), regulatory issues, geopolitical issues, management missteps, economic recessions, and the unforeseen ("expect the unexpected").

To conclude, don't go far off looking for the next $1 trillion company. It is right in front of your eyes, within Amazon's cloud.