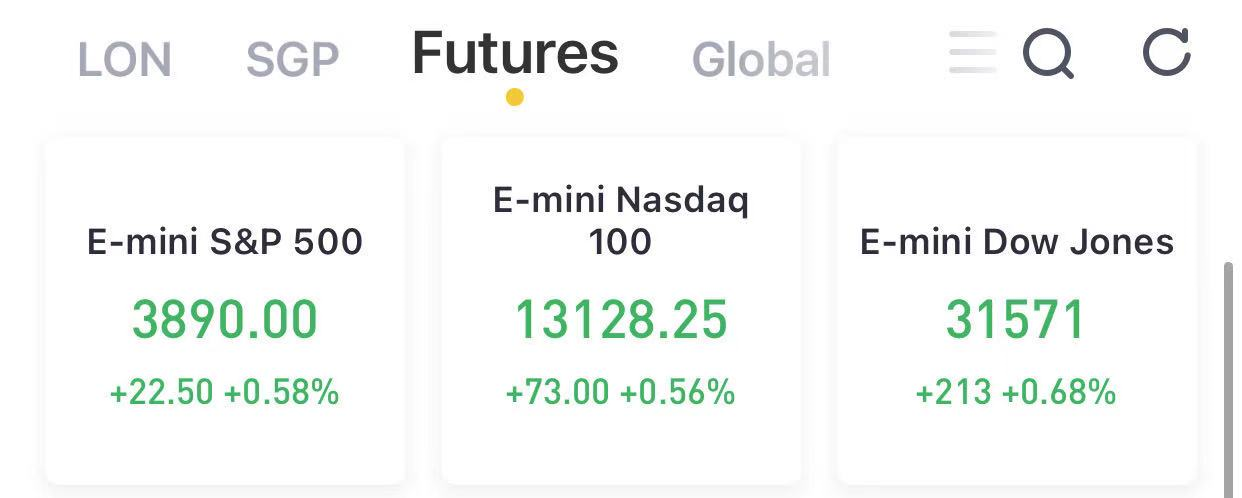

(March 3) U.S. stock index futures rose on Wednesday as a swift global roll out of vaccines and a new round of stimulus bolstered bets on a quick economic rebound, with investors also focusing on private employment and service sector reports.

Futures for the Dow Jones Industrial Average climbed 213 points to 31,571.00 while the Standard & Poor’s 500 index futures rose 22.50 points at 3,890.00. Futures for the Nasdaq 100 index rose 73 points to 13,128.25.

The Senate is expected to start debateas soon as Wednesdayon its version of the House-passed, $1.9 trillion Covid relief bill. However, it excludes a federal minimum wage boost to $15 per hour. PresidentJoe Bidenon Tuesday urged Democrats to stand united and approve the measure, even as some party moderates sought to dial back parts of the package. Democrats, with the slimmest of margins in the Senate, are using special rules that would allow them to pass the bill without GOP support.

U.S. Market Yesterday

Wall Street ended lower on Tuesday.The S&P 500 technology sector index dropped 1.6%, extending a pullback from late last month after a selloff in the U.S. bond market sparked fears over highly valued stocks. The consumer discretionary index dipped 1.3%, with Amazon falling 1.6%.

The Dow Jones Industrial Average fell 0.46% to end at 31,391.52 points, while the S&P 500 lost 0.81% to 3,870.29. The Nasdaq Composite dropped 1.69% to 13,358.79.

Latest News

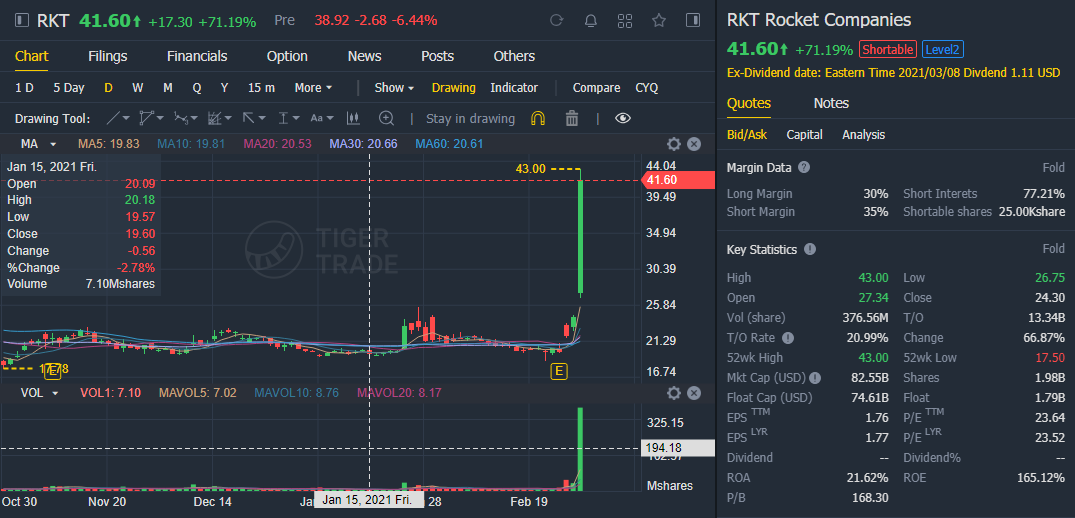

1) Rocket Companies fell 6% in Wednesday’s premarket trading after more than doubling over the past three sessions. On Tuesday, the Quicken Loans and Rocket Mortgage parentsurged over 71%on no apparent news. The heavily shorted stock appears to have garnered bullish interest from day traders on Reddit’s WallStreetBets forum.

3) Lyft, Inc. – The ride-hailing company said that last week saw the highest level of ride volume since the pandemic took hold last March. As a result, Lyft expects to report a smaller quarterly loss than it had previously projected. Lyft shares jumped 5.6% in premarket trading.

4) fuboTV Inc. – FuboTV reported quarterly revenue in excess of $100 million for the first time, with the live sports streaming company reporting a better-than-expected $105.1 million in sales. Subscriber numbers jumped 73% from a year earlier to a total of 548,000. Its shares fell 4% in the premarket, however, following a nearly 50% year-to-date jump.

5) Las Vegas Sands – The casino operator’s shares rose 3% in the premarket after it announced a deal to sell its Las Vegas properties to private-equity firms Apollo Global (APO) and VICI Properties for $6.25 billion. The sale includes The Venetian Resort Las Vegas and the Sands Expo and Convention Center. Apollo Global shares gained 2.1%.

6) Wendy's – The restaurant chain missed estimates by a penny a share, with quarterly earnings of 17 cents per share. Revenue came in short of forecasts as well. Global comparable sales rose 4.7%, shy of the FactSet consensus estimate of 5.7% due primarily to international weakness. Its shares fell 3.3% in the premarket.

7) Dollar Tree – The discount retailer earned $2.13 per share for the fourth quarter, beating estimates by 2 cents a share. Revenue essentially was in line with expectations. Comparable-store sales rose 4.9%, short of the 5.5% estimate of analysts surveyed by FactSet. The company’s shares fell 2% in the premarket.

8) Hewlett Packard Enterprise – HPE beat estimates by 11 cents a share, with quarterly earnings of 52 cents per share. The enterprise computing hardware maker’s revenue came in above forecasts as well. The company issued strong guidance for both the current quarter and full year, as it continues to benefit from the pandemic-inspired digital transformation.

9) Box – Box reported quarterly earnings of 22 cents per share, 5 cents a share above estimates. Revenue beat projections as well. The online data storage company also issued a better-than-expected full-year outlook and expects that the current quarter will see revenue above $200 million for the first time.

10) Nordstrom – Nordstrom earned 21 cents per share for its latest quarter, 7 cents a share above estimates. The retailer also reported better-than-expected revenue. Nordstrom was helped by a boost in digital sales as well as growth in its off-price operation, but the retailer warned that it would have to clear excess holiday inventory through that off-price channel. Shares fell 2.6% in premarket action.

11) Urban Outfitters – Urban Outfitters beat estimates by 2 cents a share, with quarterly earnings of 30 cents per share. The apparel retailer’s revenue fell slightly below Wall Street forecasts, however, and gross profit margins dropped more than 3 percentage points from a year earlier. Its shares fell 1.6% in the premarket.

12) Ross Stores – Ross Stores sank 3.1% in the premarket after it reported quarterly earnings of 67 cents per share, below the $1.00 a share consensus estimate. The discount retailer’s revenue came in below estimates as well, hurt by pandemic-related store closures in California.

What to know today

- 7:00 a.m. ET: MBA Mortgage Applications, week ended February 26 (-11.4% during prior week)

- 8:15 a.m. ET: ADP Employment Change, February (200,000 expected, 174,000 in January)

- 9:45 a.m. ET: Markit US Composite PMI, February final (58.8 in prior print)

- 9:45 a.m. ET: Markit US Services PMI, February final (58.9 expected, 58.9 in prior print)

- 10:00 a.m. ET: ISM Services Index, February (58.7 expected, 58.7 in January)

- 2:00 p.m. ET: Federal Reserve releases Beige Book

A Peek Into Global Markets

European markets were higher today. The Spanish Ibex Index rose 0.4% and STOXX Europe 600 Index rose 0.5%. The French CAC 40 Index rose 0.8%, German DAX 30 gained 0.8% while London's FTSE 100 rose 1%. French government budget deficit increased to EUR 21.9 billion in January from EUR 20 billion in the year-ago month.

Asian markets traded higher today. Japan’s Nikkei 225 rose 0.51%, China’s Shanghai Composite climbed 1.95% and Hong Kong’s Hang Seng Index rose 2.7%. Australia’s S&P/ASX 200 rose 0.8%, while India’s BSE Sensex rose 2.3%. Indian services PMI rose to 55.3 in February from 52.8 in the prior month, while China’s services PMI dipped to a ten-month low of 51.5 for February. Japanese services PMI rose to 46.3 in February from a final reading of 46.1 a month earlier, while Hong Kong’s private sector PMI increased to 50.0 in February from 47.8 in January. The Australian GDP increased 3.1% qoq in the fourth quarter, while services PMI fell to 53.4 in February from 55.6 in the prior month.

Currencies

The Bloomberg Dollar Spot Index gained 0.1%.The euro fell 0.2% to $1.2063.The British pound was little changed at $1.3952.The onshore yuan strengthened 0.1% to 6.465 per dollar.The Japanese yen weakened 0.3% to 107 per dollar.

Bonds

The yield on 10-year Treasuries advanced five basis points to 1.44%.The yield on two-year Treasuries climbed less than one basis point to 0.13%.Germany’s 10-year yield gained two basis points to -0.33%.Britain’s 10-year yield advanced three basis points to 0.719%.Japan’s 10-year yield dipped one basis point to 0.119%.

Commodities

West Texas Intermediate crude advanced 1.9% to $60.87 a barrel.Brent crude increased 1.9% to $63.87 a barrel.Gold weakened 0.9% to $1,722.81 an ounce.

Bitcoin Price

Bitcoin jumped more than 6% to climb above $50,000 and to its highest in a week.

Gold

Gold, on the other hand, slipped 0.8%.