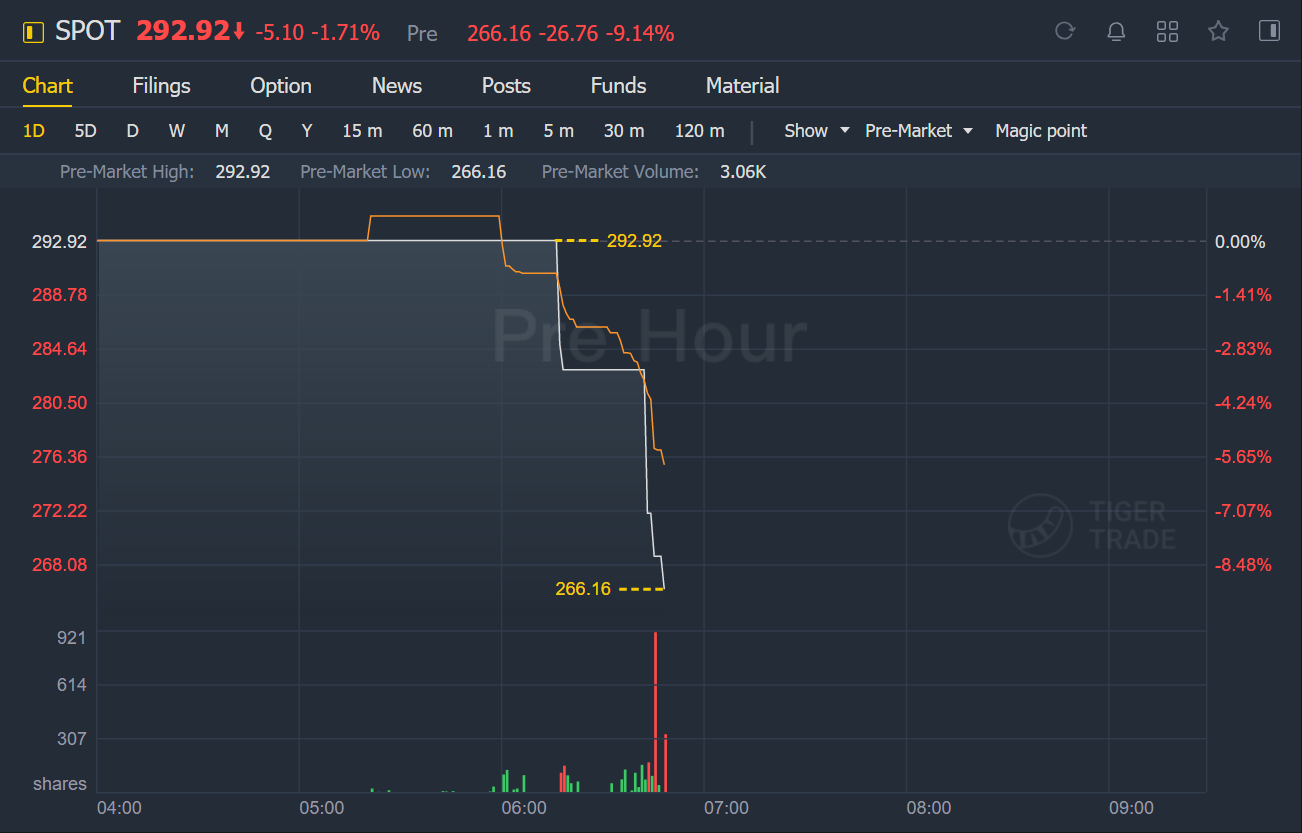

Spotify fell more than 9% in premarket trading, and the number of monthly active users in the first quarter fell short of market expectations.

Spotify Technology S.A. (NYSE:SPOT) today reported financial results for the first fiscal quarter of 2021 ending March 31, 2021.

Dear Shareholders,

We are pleased with our performance in Q1. The business delivered subscriber growth and Gross Margin at the top end of our guidance range, a continued improvement in ARPU, and operating income better than plan. We saw greater MAU variability this quarter, but results were within our range of expectations given the outperformance in Q4 and the continued impact from COVID-19. Revenue grew by 16% (22% excluding the impact of FX) and was at the upper end of our guidance range. Other highlights from the quarter include a successful launch in 86 new markets, a $1.5 billion Exchangeable Notes offering, and the acquisition of Betty Labs (Locker Room).

MONTHLY ACTIVE USERS (“MAUs”)

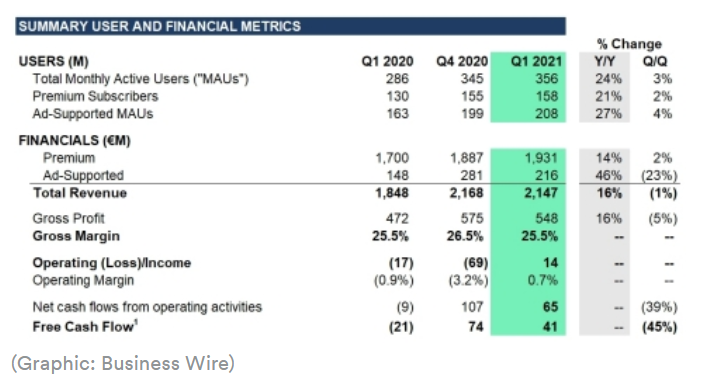

Total MAUs grew 24% Y/Y to 356 million in the quarter, finishing within our guidance range but modestly below our internal expectations. In Q1, we added 11 million MAUs, which drove healthy double digit Y/Y growth across all regions. We saw meaningful contributions from markets such as the US, Mexico, Russia, and India. However, growth was lower than plan in Latin America and Europe. In aggregate, the performance of our newly launched markets was in line with our expectations.

Global consumption hours continued to grow meaningfully in Q1 on a Y/Y basis. Per user consumption grew in developed regions such as North America and Europe, while developing regions showed signs of improvement but remained below pre-COVID levels.

PREMIUM SUBSCRIBERS

Our Premium Subscribers grew 21% Y/Y to 158 million in the quarter, hitting the top end of our guidance range. In Q1, we added nearly 4 million subscribers, which drove healthy double digit Y/Y growth across all regions and was strong relative to a tough promotional comparison from Q1 last year. The subscriber outperformance was fairly broad based and led by North America, where we saw stronger than expected performance of Trials & Campaigns and faster than anticipated growth in our Standard product. In Latin America, we saw outperformance driven by the continued success of our Family Plan product. We are pleased with the new market contributions, with South Korea being the biggest driver.

Our average monthly Premium churn rate for the quarter was down modestly Y/Y and flat Q/Q. The Y/Y improvement continues to be driven by the adoption of our higher retention offerings like Family Plan in addition to growth in high retention regions.

FINANCIAL METRICS

Revenue

Total revenue of €2,147 million grew 16% Y/Y in Q1 (22% Y/Y on a constant currency basis). Reported revenue was toward the top end of our guidance range due to subscriber outperformance, slightly lower headwinds from FX (600 bps impact vs. 770 bps incorporated into our plan), and advertising strength. The FX impact was primarily driven by the Y/Y US dollar weakness vs. the Euro. Premium revenue grew 14% Y/Y to €1,931 million (or 19% Y/Y in constant currency terms) while Ad-Supported revenue was particularly strong, growing 46% Y/Y to €216 million (or 57% Y/Y in constant currency terms).

Within Premium, average revenue per user (“ARPU”) of €4.12 in Q1 was down 7% Y/Y (but down only 1% Y/Y in constant currency terms vs. down 3% Y/Y in Q4). Excluding FX, product mix accounted for the majority of the ARPU decline. To date, we have raised prices across a variety of our Premium offerings in over 30 markets and early results have shown no material impacts to gross intake or cancellation rates. On April 26th, we announced price increases for various subscription products in 12 additional markets, including the United States (Family Plan), United Kingdom (Student, Family, and Duo Plans), and Brazil (Full Portfolio).

Ad-Supported revenue outperformed our forecast with all regions growing double digits Y/Y excluding the impact of FX. The strength in Ad-Supported revenue was led by our Podcast and Programmatic channels, with the former benefiting from the acquisitions of Megaphone and The Ringer along with our exclusive licensing of the Joe Rogan Experience. Spotify Ad Studio grew substantially Y/Y, and we continued to expand the self-serve offering to more markets (France, Germany, and Italy) and began beta testing podcast inventory ad buying on Spotify Ad Studio in the US. Additionally, in April, we expanded Streaming Ad Insertion (“SAI”) from the US, Canada, United Kingdom, and Germany to also include Australia and Sweden.

In February, we announced the Spotify Audience Network, a first-of-its-kind audio advertising marketplace which connects advertisers to listeners across Spotify Owned & Exclusive (“O&E”) podcasts, podcasts from enterprise publishers via Megaphone, podcasts from emerging creators via Anchor, and ad-supported music. The Spotify Audience Network bundles multiple shows for advertisers to buy specific audiences using our proprietary SAI technology. We believe this shift will provide advertisers much greater reach and efficiency while creators gain a much greater monetization opportunity.

Gross Margin

Gross Margin finished at 25.5% in Q1, at the top end of our guidance range and flat Y/Y. While we continue to see strong revenue growth in podcast and non-music revenue, our non-music costs continue to grow at a slightly faster rate which is a modest drag on our Gross Margin. We did see improvements in Other Cost of Revenue (e.g. payment fees, streaming delivery costs) which offset the content spend increase.

Premium Gross Margin was 27.9% in Q1, down 42 bps Y/Y and Ad-Supported Gross Margin was 4.4% in Q1, up 1,100 bps Y/Y. As a reminder, all content costs related to podcast investment are included in the Ad-Supported business for the current and historical periods.

Operating Expenses / Income (Loss)

Operating Expenses totaled €534 million in Q1, an increase of 9% Y/Y and below our plan. Social Charges were approximately €35 million lower than forecast due to a decrease in our share price during the quarter, accounting for the majority of our Operating Expense variance. Excluding the impact of our share price volatility, Operating Expenses grew less than forecast at 14% Y/Y. Certain marketing expenses came in lower than expected due to campaign timing shifts, which were partially offset by higher than expected personnel expenses.

As a reminder, Social Charges are payroll taxes associated with employee salaries and benefits, including share-based compensation. We are subject to social taxes in several countries in which we operate, although Sweden accounts for the bulk of the social costs. We don’t forecast stock price changes in our guidance so upward or downward movements will impact our reported operating expenses.

At the end of Q1, our workforce consisted of 6,794 FTEs globally.

Product and Platform

On March 29, 2021, we acquired Betty Labs, the creators of Locker Room, a live audio app that’s changing the way insiders and fans talk about sports. This acquisition builds on our work to create “future formats of audio” and will accelerate Spotify’s entry into the live audio space. We plan to evolve and expand Locker Room into an enhanced live audio experience for a wider range of creators and fans. Through this new live experience, Spotify will offer a range of sports, music, and cultural programming, as well as a host of interactive features that will enable creators to connect with audiences in real time. We intend to give professional athletes, writers, musicians, songwriters, podcasters, and other global voices opportunities to host real-time discussions, debates, ask me anything (AMA) sessions, and more.

During the quarter, Spotify launched multiple upgrades, including a new Desktop App and Web Player redesign that makes the user experience and navigation easier than ever by combining a modern scalable web player together with a cohesive Spotify design. Additionally, our web platform includes 36 new languages (62 in total), which also will be rolled out to the mobile app, allowing Spotify to reach more audiences.

We also began testing Podcast Topic Search in the US, which enables listeners to search for podcasts by theme and topic in an effort to make discovering new content easier than ever. In February, we announced a new partnership between Anchor and WordPress to generate opportunities for content creators to evolve their work and reach new audiences through the power of audio. With this new tool, bloggers can publish their written content as a podcast with just a few clicks—and podcasters can create a website for their podcast just as easily. This offers a whole new group of creators—those who have historically focused on the written word—to access an entirely new audience via audio and share their voices on Spotify.

We remain focused on our ubiquity strategy and continue to expand support for Spotify across a variety of platforms and markets. With the expansion of our footprint into non-music content, we also have expanded support for video podcasts on AppleTV (including AirPlay2), LG, and Comcast. At the end of Q1, users in 10 additional markets, including Sweden, Australia, and Chile, can now ask Alexa to play podcasts from Spotify. Additionally, PlayStation's PS4 and PS5 consoles now support Spotify in 5 new markets, including Russia, Ukraine, Croatia, Slovenia, and Israel.

Post Q1, we announced a limited launch of Car Thing to eligible US users. Car Thing is a smart player that allows users to more seamlessly engage with Spotify music, news, entertainment, talk, and more in the car. We also launched a joint partnership with Facebook to create an integrated ecosystem with a miniplayer experience driven by social discovery that allows listeners to enjoy audio from Spotify directly within Facebook, without switching between apps. Additionally, we announced new ways for podcast creators to monetize their work with the rollout of Spotify’s Paid Subscriptions, the Spotify Open Access Platform, and utilization of the Spotify Audience Network for independent creators. These initiatives provide creators with different options to monetize their work, which allows them to continue to grow their audiences and create meaningful revenue streams.

Content

At the end of Q1, we had 2.6 million podcasts on the platform (up from more than 2.2 million podcasts by the end of Q4). The percentage of MAUs that engaged with podcast content on our platform was consistent with Q4 levels. From a consumption standpoint, we saw a strong increase in Q1 podcast consumption hours vs. Q4, with March activity driving an all-time high in terms of podcast share of overall platform consumption hours.

The Joe Rogan Experience performed above expectations with respect to new user additions and engagement. Notable Q1 content launches in the US included Renegades: Born in the USA (Higher Ground), Unlocking Us with Brene Brown (Parcast), Ringer Dish Feed - Taylor Swift (The Ringer), and Welcome To Your Fantasy (Gimlet). Renegades: Born in the USA, featuring former President Barack Obama and Bruce Springsteen, was the second largest podcast on Spotify in March (on an MAU basis) and has been our most international show to-date, with listenership extending across more than 150 countries. Internationally, we released 55 new O&E podcasts. Select launches included a Japanese original Juju Talk, which was a major driver of user acquisition in the country, as well as our first daily new original in Germany, FOMO - was hab ich heute verpasst (what did I miss today?). Additionally, we launched our first slate of 7 Spotify Originals in the Philippines, with topics ranging from gaming to well-being, featuring personalities like Pia Wurtzbach and Donnalyn Bartolome.

On the music front, key Q1 releases included Olivia Rodrigo’s single,drivers license, which set the Spotify record for most streams in a day for a non-holiday song with over 15 million global streams on January 11. Additional releases include Arlo Parks’ album,Collapsed in Sunbeams, as well as Selena Gomez’s EP,Revelación. Daft Punk and Spotify partnered to celebrate the 20th anniversary of their highly acclaimed 2001 opusDiscoverywith an enhanced playlist experience after the announcement of the duo splitting up. The playlist included exclusive Canvas and Storylines for every track on the album, and since the start of the campaign, Daft Punk has seen a double digit increase in follows on-platform.

Two-Sided Marketplace

Sponsored Recommendations have shown strong growth and are becoming an essential part of new release marketing strategies for artists and labels. Q1 was the biggest quarter yet for Sponsored Recommendations, with an 11% increase over campaign volume from last quarter and a 10% increase in new customers vs. Q4. In an effort to expand and evolve Sponsored Recommendations, we expanded into Australia and New Zealand and have now made this tool available for singles. Additionally, we began the rollout of a self-serve buying experience for Sponsored Recommendations to select artist and label teams in the US.

At our Stream On event, we announced that we’re testing a new commercial tool called Discovery Mode with a small group of labels that enables artists to better reach new audiences on Spotify. To ensure the tool is accessible to artists at any stage of their careers, it will not require any upfront budget and instead, labels or rights holders agree to be paid a promotional recording royalty rate for streams in personalized listening sessions where we provided this service. Early results from the labels participating have been positive with participating labels seeing a 30% increase in streams for content opted in on average.

This quarter, we announced that all artists now have access to our popular feature, Canvas, through Spotify for Artists. The Canvas for Rodrigo’sdrivers licensewas shared from Spotify to Instagram Stories over 243,000 times in its first week alone and was viewed more than 50 million times in its first three weeks. Artists at every stage of their career have used Canvas, and we now have over 1 million Canvases live on Spotify.

In Q1, we launched Noteable — our new global home for songwriters, producers and publishers which is a central space to access all the resources we’ve made available to the songwriting and publishing community, including Spotify Publishing Analytics, SoundBetter, Songwriter Pages and Song Credits, the Songwriting Hub, and more.

Free Cash Flow

Free Cash Flow was €41 million in Q1, a €61 million increase Y/Y as the prior year included an unfavorable impact to working capital due to a shift in timing for select licensor payments as well as an increase in net income adjusted for non-cash items. These increases were partially offset by higher cash outflow for PP&E.

In addition to the positive Free Cash Flow dynamics, we maintain a strong liquidity position and are confident in the financial position of the business. During Q1, Spotify USA Inc. issued $1.5 billion in aggregate principal amount, zero coupon Exchangeable Notes due 2026 with a 70% conversion premium. At the end of Q1, we had €3.1 billion in cash and cash equivalents, restricted cash, and short term investments.

Q2 & 2021 OUTLOOK

The following forward-looking statements reflect Spotify’s expectations as of April 28, 2021 and are subject to substantial uncertainty. The estimates below utilize the same methodology we’ve used in prior quarters with respect to our guidance and the potential range of outcomes. Given the extraordinary operating circumstances we currently face with respect to the impact of COVID-19, there is a greater likelihood of variances with respect to those ranges than typical quarters.

Q2 2021 Guidance:

- Total MAUs: 366-373 million

- Total Premium Subscribers:162-166 million

- Total Revenue:€2.16-€2.36 billion

- Gross Margin:23.6-25.6%

- Operating Profit/Loss:€(134)-€(54) million

Full Year 2021 Guidance: We have modestly lowered our Total MAUs range for the full year consistent with the lower than expected Q1 Total MAU growth. Additionally, we have increased our outlook for Total Revenue and Gross Margin, as well as decreased the Operating Loss expectations. Our Premium Subscriber outlook remains unchanged.

- Total MAUs: 402-422 million

- Total Premium Subscribers:172-184 million

- Total Revenue:€9.11-€9.51 billion

- Gross Margin:24.0-26.0%

- Operating Profit/Loss:€(250)-€(150) million