(June 23) Most of Chinese education stocks gained in morning trading Wednesday.

Do Hedge Funds Think EDU Is A Good Stock To Buy Now?

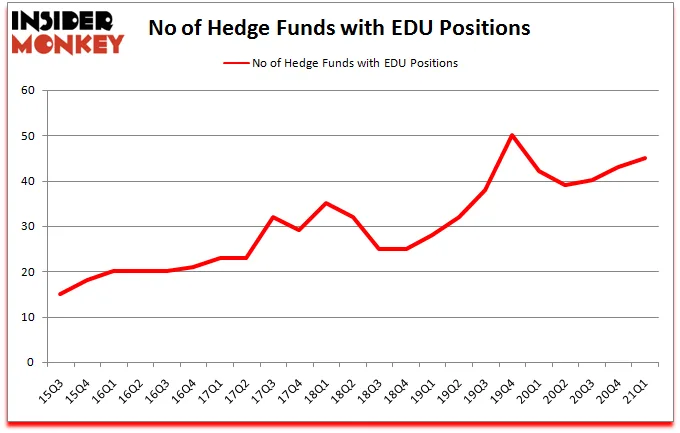

At first quarter's end, a total of 45 of the hedge funds tracked by Insider Monkey were bullish on this stock, a change of 5% from one quarter earlier. Below, you can check out the change in hedge fund sentiment towards EDU over the last 23 quarters. With the smart money's positions undergoing their usual ebb and flow, there exists an "upper tier" of noteworthy hedge fund managers who were upping their holdings significantly (or already accumulated large positions).

As industrywide interest jumped, some big names were breaking ground themselves. Thunderbird Partners, managed by David Fear, established the most valuable position in New Oriental Education & Technology Group Inc. (NYSE:EDU). Thunderbird Partners had $16.7 million invested in the company at the end of the quarter. Eduardo Costa'sCalixto Global Investorsalso made a $14.7 million investment in the stock during the quarter. The other funds with brand new EDU positions are Matthew Hulsizer's PEAK6 Capital Management, Campbell Wilson'sOld Well Partners, and Daryl Smith's Kayak Investment Partners.

Let's now review hedge fund activity in other stocks - not necessarily in the same industry as New Oriental Education & Technology Group Inc. (NYSE:EDU) but similarly valued. These stocks are Kansas City Southern (NYSE:KSU), Nucor Corporation (NYSE:NUE), Franco-Nevada Corporation (NYSE:FNV), Fortive Corporation (NYSE:FTV), The Hartford Financial Services Group Inc (NYSE:HIG), Itau Unibanco Holding SA (NYSE:ITUB), and Trip.com Group Limited (NASDAQ:TCOM). All of these stocks' market caps are closest to EDU's market cap.

As you can see these stocks had an average of 32.1 hedge funds with bullish positions and the average amount invested in these stocks was $1239 million. That figure was $2188 million in EDU's case. The Hartford Financial Services Group Inc (NYSE:HIG) is the most popular stock in this table. On the other hand Itau Unibanco Holding SA (NYSE:ITUB) is the least popular one with only 12 bullish hedge fund positions. New Oriental Education & Technology Group Inc. (NYSE:EDU) is not the most popular stock in this group but hedge fund interest is still above average. Our overall hedge fund sentiment score for EDU is 70.7. Stocks with higher number of hedge fund positions relative to other stocks as well as relative to their historical range receive a higher sentiment score. This is a slightly positive signal but we'd rather spend our time researching stocks that hedge funds are piling on. Our calculations showed thattop 5 most popular stocksamong hedge funds returned 95.8% in 2019 and 2020, and outperformed the S&P 500 ETF (SPY) by 40 percentage points. These stocks gained 17.4% in 2021 through June 18th and beat the market again by 6.1 percentage points. Unfortunately EDU wasn't nearly as popular as these 5 stocks and hedge funds that were betting on EDU were disappointed as the stock returned -45.8% since the end of March (through 6/18) and underperformed the market.

TAL Education: Not Ready To Handle A New Wave Of Market Rivalry

Summary

- FY2Q2021 revenue and XRS online growth fell below consensus expectations.

- In 2020, the online K12 education market size in China reached CNY 89 billion, with a year-on-year increase of 37.6%.

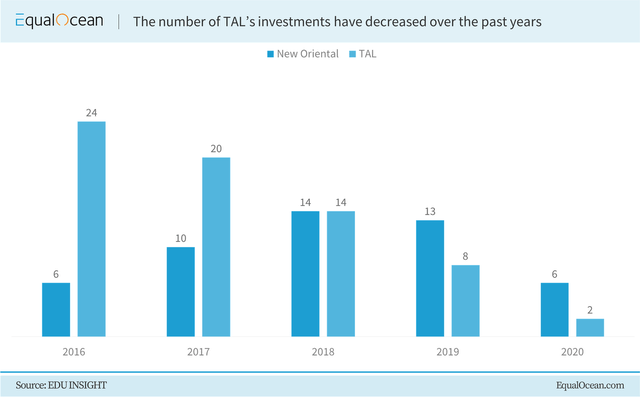

- Unlike its nemesis New Oriental, TAL's investment amount into other firms has been continuously decreasing since 2016.

- With COVID-19 reshaping the market, tech giants have started to make big moves into the digital education industry.

- We do not see the company handling the upcoming tough competition within the industry but are rather optimistic about its business capabilities and steady growth.

TAL Education Group (also known as Tomorrow Advanced Learning) (TAL) is an education company that focuses on K12 students in China. It also has business segments in adult education, early education & parenting and education informatization. The firm takes quality education and extracurricular tutoring as the carrier system to serve on a global scale. Founded in 2003, it went public on NYSE in 2010.

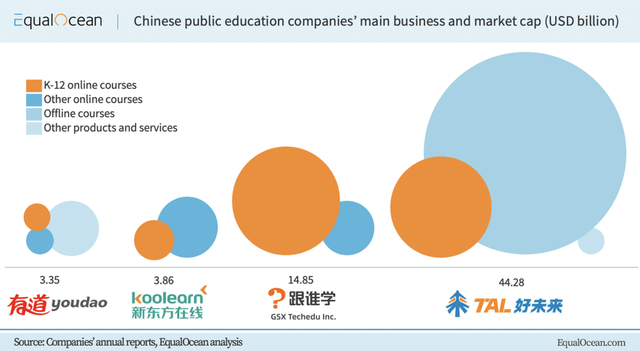

In China, TAL competes with New Oriental (EDU), a company founded back in 1993. It can be said that both firms are leading China's education industry; for one, the market coverage of the two is evenly matched. From the latest information, New Oriental has active businesses in a total of 98 cities in China and one foreign city (Toronto). TAL has laid its business in a total of 90 cities across China.

As parents in the fast-growing country pay more and more attention to their children's basic education and e-learning is increasingly popular, the vast field of primary and secondary education and online education has eventually become a battleground for companies.

Decent financial results

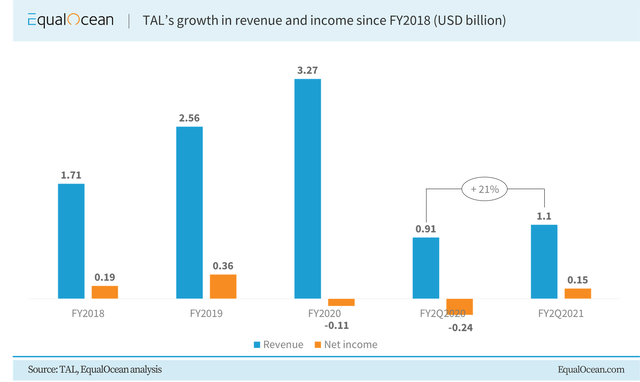

TAL's 2Q 2021financial resultsweren't very impressive, as the firm earned USD 1.10 billion (up 20.8% year-on-year) compared to analysts' expectations of USD 1.12 billion for the quarter. However, it reported USD 0.08 earnings per share for the quarter, beating analysts' consensus estimates of USD 0.05 by USD 0.03. TAL Education Group had a return on equity of 0.21% and a net margin of 1.35% compared to 8.97% in 1Q 2021 due to strong competition presented in the primary education segment. It includes local pure online education companies such asYuanfudaoandZuoyebangthat recently completed mega-rounds of investment. Meanwhile, the non-GAAP operating margins were down to -1.1% compared to 9.8% in 2Q 2020 as customer acquisition costs rose backed by the fierce competition.

In the past five to six years, with the support of the state, the development of technology, and the inflow of capital, China's online K12 education industry has undergone rapid development. In 2020, the overall online K12 education market size in China reached approximately CNY 89 billion, with a year-over-year increase of 37.6%.

In 2019, the penetration rate of K12 online education in China was about 15%. As COVID-19 struck during the beginning of 2020, the advantages of online education have been very apparent. The penetration rate of online K12 education reached its peak in March 2020. Although the industry is still in the stage of consumption popularization in China, there are obvious trends. This field consistently demonstrates a long-term massive demand as an emerging way of obtaining education information and services. Hence, the industry penetration rate has huge room for improvement in the future. According to thepredictionof the Chinese Academy of Sciences, the penetration rate of the K12 online education industry may exceed 55% by 2022.

The fact that TAL owns 871 learning centers (offline tutoring centers), 648 Peiyou (好未来培优) centers and 128 one-on-one centers is the reason why we believe TAL is not pandemic-proof. Possible closure of these centers by the government in order to control the spread of COVID-19 will lead to huge declines in the firm's financials.

TAL does own online education apps – but they can't compete with the likes of VIPKID, Yuanfudao, and Zuoyebang, even though there has been an increase in revenue contribution of Xueersi TAL’s online app from 17% in FY2Q2020 to 26% in FY2Q2021.

The re-emergence of COVID-19 in China is a headwind for TAL's offline classroom-based training business. Although the vaccine has emerged, children below the age of 18 are not allowed to administer it. TAL's stock price might soon fall when most investors realize that the company still focused on formal or classroom-based tutorials and training.

TAL has had stable growth since getting listed about nine years ago. Revenue has increased about 30 times, at a compound annual rate of 45.7% since then and gross margins averaged as high as 50.8%.

Results from the last fiscal year ending February were materially affected by COVID-19 induced restrictions which had started early in China. Offline operations, primarily core Peiyou small classes, had to be quickly transferred to online platforms. As a result, some revenue was lost due to the lower selling prices for online classes, the total revenue in Q4 grew just 6.2% compared to 44.1% the previous year. Student enrollments were still up on aggregate with a rate of, 56.6% year-over-year.

Less venture investment presence

Since 2017, the number of investments by TAL has been decreasing. New Oriental has been more aggressive compared to TAL since 2018. TAL's financing has dropped sharply from 24 in 2016 to only two in 2020. The two investments were made on an interactive learning SaaS platform UMU and an online children's math tutoring app.

The entrance of tech giants

Sales and marketing expenses surged as the competition got tough for online players in the summer. Sales and marketing expenses surged 64% year-on-year and made up 22% of the total revenue, up 4.9% year-on-year.

With upstarts raising mega-rounds, things might get even tougher for TAL as more companies with huge capital to spend on marketing will try to grab market share. Other than that, Chinese giants such as Alibaba(NYSE:BABA), NetEase(NASDAQ:NTES), Tencent(OTCPK:TCEHY), ByteDance and Baidu(NASDAQ:BIDU)engage their businesses into online education. TAL needs to upgrade its online education business to stay afloat.

The education field is likely to be divided up by companies outside of this industry. It is also worth mentioning that the firm's key competitiveness is its in-depth application of technologies such as big data and live broadcast intelligence in China's online education industry. The firm has not spent much on research and development in terms of proprietary tuition-based technology. There are few existing barriers to entry. Teaching staff and market share could be theoretically purchased by new entrants.

Allegation probe

In April 2020,TAL became one of the scandalous US-listed Chinese firmsafter admitting to inflate sales figures driven by employee wrongdoing, further hindering market confidence after Luckin Coffee's(OTCPK:LKNCY)USD 310 million fraud.

Two years before this event, Muddy Waters released areportnaming the company 'A Real Business With Fake Financials.' The report claimed that "TAL commits fraud in the financials for its core Peiyou business. The Peiyou fraud is more difficult to quantify, but our research suggests fraudulent overstatement of approximately 25% to 30% of the company’s revenue."

Bottom line

This might not be a suitable time to invest in TAL Education. We give a neutral rating to the stock because we do not see the company handling the upcoming tough competition within the industry but are rather optimistic about its business capabilities and steady growth. Therefore, TAL does have a chance to enhance its online business and compete with newcomers and experienced enterprises, including the likes of Zuoyebang, Yuanfudao, Baidu and NetEase.

Gaotu Group: Policy Overhang Keeps The Risk-Reward Balanced

Summary

- The longer-term outlook remains bright for Gaotu Group (formerly GSX TechEdu).

- Adverse regulatory changes remain the key risk for the near-term outlook, but a healthier longer-term dynamic should benefit profitability.

- Growth drivers such as alternative student acquisition channels and increased contribution from adult education should help as well.

- Despite the discounted EV/Sales multiple, I would hold off on initiating a position for now pending clearance of the policy overhang.

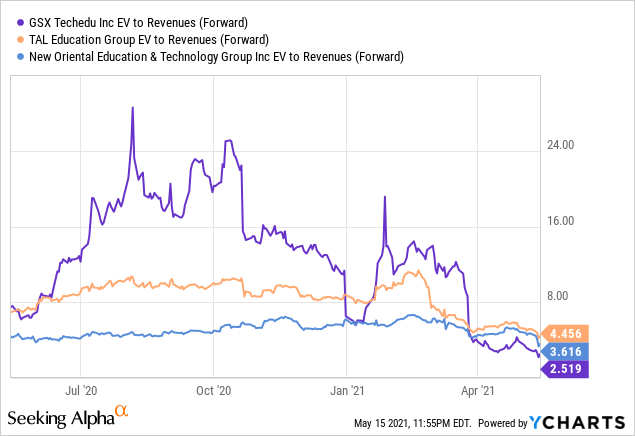

Newly rebranded Gaotu Group’s (GOTU/GSX) recently heldinvestor eventfeatured an interesting tour of its operation and top management strategy presentations, which offered timely insight into the longer-term outlook. In particular, GSX emphasized its continued focus on teaching excellence, service quality, and technology investments as key differentiators. However, policy risks remains the biggest concern, and if government intervention in the online after-school tutoring space turns out to be stricter than expected, I see material downside risks to GSX’s near-term growth trajectory. On the flip side, it could also result in a healthier industry dynamic, which should drive narrowing losses as well. While the policy reform overhang makes it difficult to turn bullish, GSX’s discounted c. 3x EV/Sales multiple also looks undemanding, keeping the risk/reward fairly balanced.

Growing Importance of Alternative Student Acquisition Channels

Worryingly, GSX has seen reduced traffic acquisition in FQ4 ‘20 and FQ1 ‘21, with a whopping c. 20% lower sales lead cost in Jan-Feb 2021 (down from the Nov-Dec 2020 period). The recent decline is likely attributable to regulatory uncertainties around online traffic acquisition triggered by a recent Ministry of Education (MOE)interviewearlier this year. The significantly pressured new enrolment growth in FQ1 ‘21 may have been one of the reasons for the lower-than-expected top-line guidance as well. In response, management is exploring new student acquisition channels to offset the pressure – this includes the offline, short video, and live streaming e-commerce channels, among others. The good news is that successful expansion here could see the student acquisition cost lowered by over 50%, which is positive for the margin outlook (GSX is currently loss-making at the operating level).

Source:GSX Investor Presentation Slides

However, GSX is not alone in this regard – other online AST players have initiated similar moves, from online one-on-one and small-class players such as 51talk (COE), VIPKID, and New Oriental subsidiary Koolearn, whose large-class coverage has reached c.100 cities. Similarly, online large-class after-school tutoring players have also started expanding into offline acquisition through partnerships, with TAL Education (TAL) subsidiaryXueersi.comalsotying upwith Lenovo (OTCPK:LNVGY) in recent months. And with private players like Zuoyebang alsobuildingoffline traffic acquisition teams, the competitive pressures could drive downside to the near-term outlook.

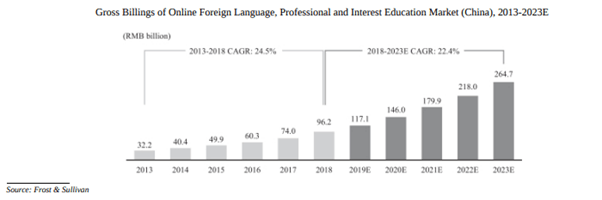

Adult Education Set to be Another Top-Line Growth Driver

Within the Chinese education market, adult education is also emerging as a potential growth opportunity as people are increasingly looking to upskill in an uncertain job market. Alongside income level rises, people are also spending more on education to better prepare themselves for career development. As a result, gross billings have grown at a CAGR of 24.5% and are expected to grow further at 22.4% CAGR into fiscal 2023, reaching RMB265 billion.

Source:GSX Listing Prospectus Filing

Notably, while GSX currently expects fiscal 2021 revenue growth to be in the range of 70-80% Y/Y, the adult education business is guided to be a key growth driver at +100% Y/Y revenue growth. Considering that adult education accounted for over 10% of GSX’s revenue in fiscal 2020, I expect the contribution to continue rising over time. Key areas of growth here include English training, graduate school admission exam prep, and finance-related courses. Longer-term, I think the adult education business could even see higher gross margins than K-12 after-school tutoring due to the higher enrolment/tutor ratio.

Online Regulations Remain the Key Concern

Looking ahead, potential online regulations in the after-school tutoring space are concerning, with likely measures including a fake advertising ban, increased control over marketing spend in education, and more stringent quality requirements for institutions and instructors. On the flip side, these measures will also be beneficial to the overall industry development longer-term, allowing online after-school tutoring players to reinvest more dollars into improving the product and teaching quality. While clarity around the new regulations for both the offline/online markets remains lacking, I see a more positive outcome than the prior industry experience in 2018.

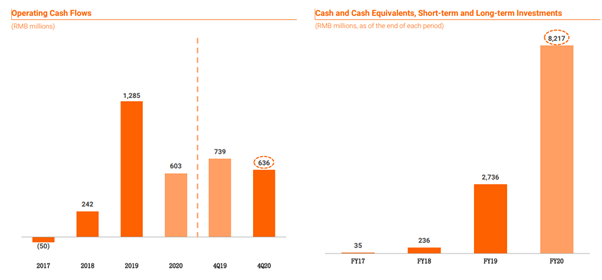

Any restrictions on marketing limitation will likely have a negative impact on enrolment and sales growth in the near term but will also benefit margins due to the lower marketing spending. In turn, this should improve the longer-term economics of the business and drive narrowing losses in the upcoming quarter. Another key positive from the slower growth is that GSX will be able to focus on improving its product/service quality and extract more student lifetime value while also preserving its robust balance sheet. As of end-2020, GSX had a c. RMB8.2 billion cash position (including liquid investments), which should allow it to weather any unforeseen negative policy impacts.

Source: GSX Investor Presentation Slides

Final Take

Overall, regulations on marketing will likely have a negative impact on enrolment and top-line growth but should also lead to a healthier operating dynamic and narrowing losses ahead. With GSX also focused on alternative acquisition channels and tapping into markets such as adult education, I think the company could surprise positively in the upcoming quarters. While the GSX share price has suffered due to the Archegos Capital event and policy concerns, its forward EV/Sales multiple has declined significantly to c. 3x, and the widening relative discount to peers like TAL and EDU likely means the negatives have been priced in. Until the policy overhang has been lifted, however, I see the risk/reward as balanced at current levels.