After a wild quarter, SoFi Technologies is set to report Q2'23 results prior to the market open on Monday. Between the Biden Admin. trying to block student debt repayments to questions regarding loan loss reporting to the use of traditional bank valuation metrics, the stock went from crashing below $5 to rallying above $10.

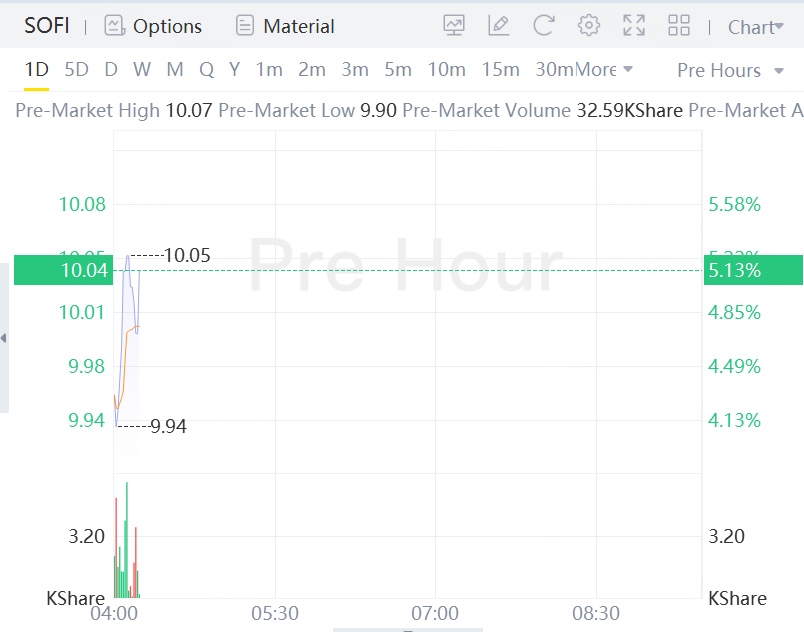

SoFi Technologies shares rise more than 5% before reporting Q2 results.

For this reason, the analyst consensus estimates for Q2 are only meaningful on the revenue side:

Consensus EPS Estimate is -$0.07 (+41.7% Y/Y)

Consensus Revenue Estimate is $475.78M (+33.6% Y/Y)

The forecast is for a GAAP loss of $0.07 in Q2 on the path to the promised GAAP profits in Q4. The big focus should be on the nearly 34% revenue growth.

Over the last few quarters, SoFi has easily topped analyst revenue targets. When the digital bank isn't impacted by surprise student loan repayment moratoriums, the company easily smashes estimates.

Going back to Q1'22, SoFi quite including the student debt expectations into financial targets, setting up the big quarterly beats of ~$20 million a quarter. The near certain student loan repayments for high income borrowers restarting in October should guarantee a ramp up in the student loan business.

When providing guidance, SoFi was clear any pickup in student loan refinancing wouldn't start until after September. The intriguing aspect of student debt loans is the profit aspect of the most mature business.

When the company made drastic cuts to the 2022 financial targets, the biggest impact was to adjusted EBITDA targets. All the way back in April 2022 prior to the Q1'23 earnings report, SoFi slashed revenue targets by $100 million while cutting adjusted EBITDA targets by $80 million.

Following Q1'23 results, SoFi guided up the adjusted EBITDA target for the year to $278 million, up $8 million. Remember, the target hike had nothing to do with student debt, as the Supreme Court ruling blocking the U.S. Education Department's debt forgiveness plan didn't occur until the end of June.

The company could up end up heading much closer to the original EBITDA targets when the SPAC deal was announced. The adjusted EBITDA margin was targeted at 32% in 2025 when profits hit $1.5 billion.