Summary

- Netflix has been an exceptional growth story.

- But as subscriber growth rates peak and competitive pressures mount, the company's long-term prospects become somewhat shaky, even as near-term prospects remain highly bullish.

- I move from a bullish to a neutral long-term prospects position until we get more information on their competitors' performances.

Netflix (NFLX) has seen exponential growth over the past several years as subscriber growth in both the United States and globally surged to record highs. The COVID-19 pandemic further aided this growth as more individuals were stuck inside and explored the vast video library the company holds while in quarantine, lockdown, or general isolation.

However, now that global and US markets have begun becoming saturated with the limit of population growth driving subscriber growth as well as the vast number of competitors the company is facing, they are becoming more and more reliant on price increases to drive higher margins and net income, which they in turn can spend on new content which they hope can become enough of a sensation to drive subscriber growth.

This business model is nearly certain to produce solid and growing results for the company in the near future as streaming services remain extremely cheap at around $10 to $20 each month as we continue and see the transition away from the far more expensive cable and TV options. But the longer-term question is at what point does the company exhaust this price hiking measure and how does that fit in with the amount of investment it must make on content to stay a relevant player in this industry.

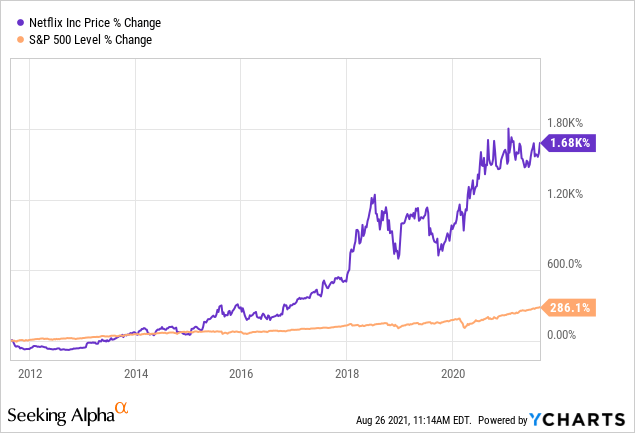

Outperforming Broader Market

Netflix has easily outperformed the broader market since it changed its business model from the early days of DVD rentals and has returned over 1,650% over the past 10 years, while the S&P500 Index returned over 280%.

This growth and outperformance were primarily driven by the surge in paid subscribers the company has seen over the better part of the past decade. Early on, they spent mountains of cash on content without seeing much profits but later on subscriber growth reached a comfortable level relative to the overall population, they put an emphasis on margins and profitability and are not reporting a steady profit stream.

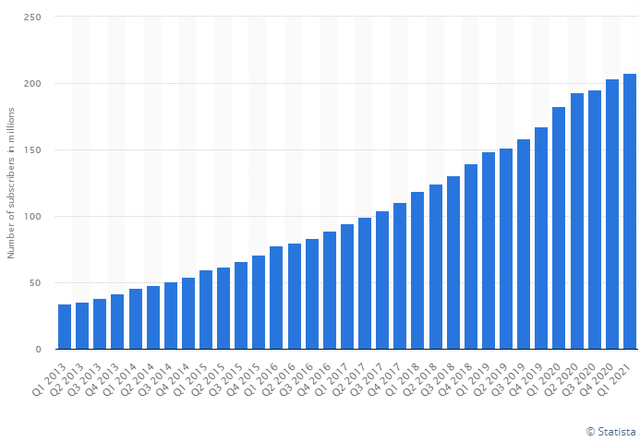

As we can see, worldwide subscriber growth has been slowing a little in recent years as the company inevitably hits peaks in some domestic and international markets. I expect this to continue over the coming quarters as we see both a saturation in this growth organically but also as people return to work, there is bound to be a certain percentage of pandemic-era users which have not been big viewers before the lockdowns who minimize expenses by canceling their subscription.

It is also noteworthy that there are now many applications and services, mostly from private companies, which help you manage your subscriptions and cancel them for you if they're inactive for a long period of time. There is certainly a set amount of paying Netflix subscribers who are not active and it's unclear if these cancellations will have any material effect but it does compound some of the other aforementioned subscriber growth issues.

Profitability set to surge

The near-term thesis derived from what I mentioned above is rather simple - the company currently charges just $10 to $20 a month for their streaming services, which in relative terms to cable TV or internet costs is very low. This means that they can, and likely will set price increases over the coming years and I believe that when doing so they won't be losing any significant number of subscribers.

I do believe, though, that a lot of these future price hikes are baked into current net income projections for the company and it's evident by those numbers that the company will enjoy much higher margins in the nearer term of 24 to 48 months. The question is, can that continue forever? I don't think so, but let's look at those projections and see where we go from here.

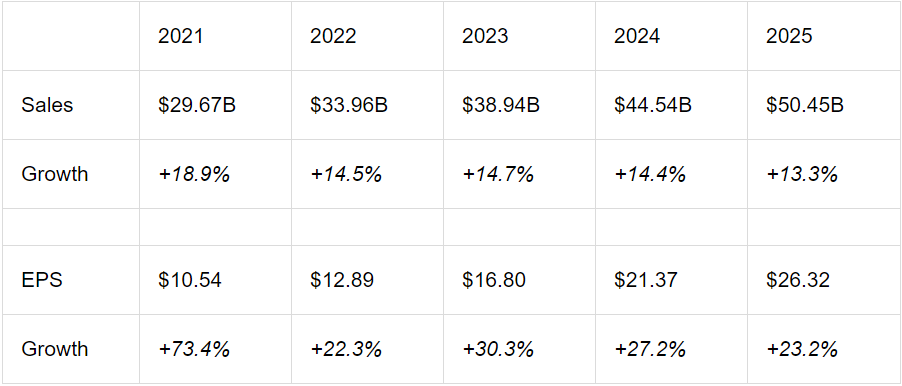

The company's sales are expected to double over the next 5 years, growing from $25 billion in 2020 to just over $50 billion by 2025, presenting a CAGR of 15.1%. This does indicate that the company will still see solid subscriber growth numbers in line with population growth and some organic growth as more of the world gets access to high-speed internet and develops a stronger non-poverty classes which tend to be the core base of the company.

When it comes to net income, the company is expected to report an EPS CAGR of over 34%, more than double their sales CAGR of 15.1%, indicative of higher prices expected to come in the next few quarters. Here's the annual breakdown of those figures for growth rate comparison:

The #1 Risk - Competition

The number one risk for the company's long term prospects is competition and it materialized in 2 ways:

The first is organic competitive pressures. Services like Amazon Prime (AMZN), Disney+ (DIS), Apple TV (AAPL), and several other major and minor players have launched their own on-demand streaming services in recent years and have seen growth rates similar to Netflix when they themselves were starting out. In it of itself, this isn't the worse thing in the world since the low prices make for the reality that most people who subscribe to one of these services also subscribes to many others but there is still content preferences and the fact that one of these other services, especially Disney+ with children shows and programs, may come out with a new hit series or movie can take away the glory from the others and Netflix can surely suffer from this.

The second part of this is that when a lot of competition emerges, it's much harder to hike prices. Netflix is a streaming company and they don't have any other parts of their business which they can use to drive subscriber growth. Almost all of the Netflix's direct competitors like Amazon, Apple, and Disney have massive cash cows in other business segments which they can use to temporarily keep subscription prices down dramatically in order to attract new subscribers. This in turn will force Netflix to keep their price hikes to a minimum and result in underperformance relative to current expectations.

So Bullish short term, cautious long term

Netflix is by no means overvalued. They currently trade at around 30x to 40x 2022 and 2023 earnings projections, respectively, which are set to grow at a 20% to 30% rate, meaning you can make the argument that they are even slightly undervalued at current levels. This makes me maintain my highly bullish rating on their near-term prospects and that they are extremely likely to outperform the broader market whether we keep heading up or even if we see a small cyclical market correction.

But their long-term prospects get a little shaky given the level of risk factors they are facing down the line. We simply will need to wait and see how their price increases fair relative to the other competitors and how their subscriber growth goes. For the meantime, these factors have me neutral on the company's long-term prospects.

I am continuing to hold a position in the company but have trimmed down shares in recent days and will continue to do so in the coming weeks.