Summary

- AT&T's period of ambiguity surrounding its divesture has ended.

- Divesture creates immense opportunities with a potential for a significant valuation appreciation.

- Given AT&T's low valuation and valuation appreciation potentials after the divesture, I believe AT&T is a strong buy.

Introduction and Thesis

AT&T (T) stock has been punished by the market for uncertainties surrounding its divesture of Warner Media. However, with the announcement on February 1st, the period of ambiguity surrounding the divesture that is expected to happen in 2022Q2 has disappeared. Yet, the company's stock continues to be in its recent lows, and I believe Mr. Market is wrong. AT&T and the WBD, the new company that will be created through the divesture, are both undervalued in comparison to their peers considering their growth potentials. Therefore, given the massive opportunities ahead of the divesture, I believe AT&T is a strong buy today. It is very likely that AT&T will see a valuation appreciation following the transaction as investors value different subsets of business separately.

Clarity

Last month, I wrote an article called "Ambiguity is Creating an Opportunity" to argue that AT&T is a buy as the ambiguity surrounding the divesture was creating a fear leading to a stock price decline. However, today, the management team has cleared these uncertainties leaving significantly fewer risks in comparison to the potential opportunities.

On February 1st, AT&T informed investors that the company will be spinning off "100% of AT&T's interest in Warner Media," which will be "followed by the merger of Warner Media with Discovery (DISCA)." The divesture is expected to close in the second quarter allowing AT&T shareholders to control 71% of the WBD, and the existing AT&T shareholders will receive 0.24 shares of the WBD for a single share of AT&T they own. I believed this information effectively cleared most of the uncertainties and doubts that were created from prolonged silence from the management team.

Opportunities

I think an investment in AT&T today will most likely result in a favorable risk to reward ratio for investors as the company offers strong growth with low valuation multiples.

Valuation

Starting with the valuation, AT&T, as a whole,is worth about $172 billion. After the divesture of 0.24 shares of WBD, the remaining AT&T will be worth about $130.7 billion. This, in my opinion, is absurd.

The comparison of the valuations between AT&T and its closest competitor, Verizon (VZ) shows a significant discrepancy. First, Verizon has a market capitalization of about $223 billion with a forward price-to-earnings ratio of about 9.76. On the other hand, AT&T has a forward price-to-earnings ratio of about 7.7 before the WBD divesture. Thus, as the management team solely focuses on its core business, the likelihood for valuation appreciation on strong execution may be high.

WBD is expected to have an undervalued valuation upon the completion of the divesture. Discovery has a market capitalization of about $20 billion today while the 24% of AT&T represents a valuation of about $41 billion resulting in a probable valuation of about $61 billion for WBD. Warner Media reported revenue of $35.6 billion for FY 2021(Q1,Q2,Q3,Q4), andDiscovery has reported a revenue of $11.4 billion in the past four quarters(the company has not reported their 2021Q4 earnings yet). Thus, the combined company would have a revenue of about $47 billion. Although the net income for these companies is not known yet, I will attempt to assume the potential net income for WBD for the sake of argument. Discovery, in the last four quarters, reported an operating income of about $2.15 billion and a net income of about $1.24 billion showing that the net income was about 57% of the operating income. On a conservative note, assuming that Warner Media can convert 30% of its operating income into a net income, the company will report $2.16 billion in income creating a combined net income of about $3.4 billion. This signifies that the WBD is also significantly undervalued.

WBD's expected closest competitors, Netflix (NFLX) and Disney (DIS), have a forward price-to-earnings ratio of about35and34, respectively. However, WBD's price to earnings ratio is expected to be about 13.8 upon the completion of its divesture showing the immense discrepancy in valuation multiples.

Growth

If two similar companies competing in the same industry have massive valuation differences, one may think that the company with the lower multiples has a significant competitive disadvantage. However, for AT&T and WBD, this is not the case.

Starting with WBD, one of its closest competitors, Netflix,is showing slowing growth as the company has already reached nearly every customer that is seeking an OTT service. On the other hand, leveraging Warner Media's vast library of famous content names with a smaller subscriber base than Netflix, the company grew its subscribers from 60.7 million to 73.8 million representing about a 21.5% year-over-year growth compared to Netflix's 8.9%. Given that the customers are growing more likely to subscribe to multiple OTT platforms, I think it is reasonable to argue that the growth for WBD will continue going into 2022 beating Netflix's growth. For this reason, I do not think that the strong discrepancy shown between the WBD's valuation compared to its competitors is reasonable.

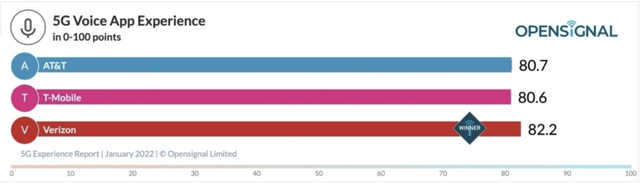

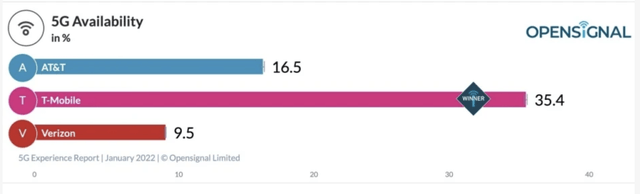

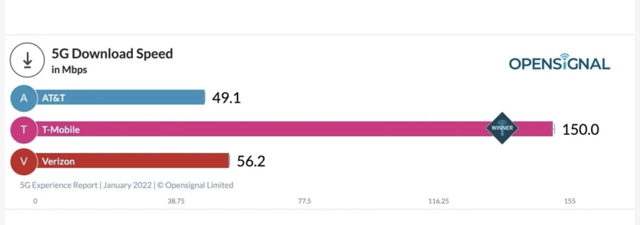

Further, AT&T's core telecommunications business fundamentals do not justify a significant valuation discrepancy in comparison to Verizon. T-Mobile (TMUS) is currently leading in 5G deployment and availability due to its uses of a different frequency, so I will only compare Verizon and AT&T as they both use a higher frequency, C-band. Starting in early 2022, both companies started rolling out their 5G offerings. Verizon is leading ahead of AT&T, but I do not think this slight difference will have a material impact on AT&T.As the multiple pictures below show, the differences in multiple tests do not show significant differences in the quality of services between Verizon and AT&T.

Phone Arena

Phone Arena

Phone Arena

Phone Arena

[Source]

Everyday consumers will not care if one carrier is X% faster download speed than the other, or if one carrier has X% better voice app experience. Even if one carrier has a faster download speed, as long as the consumers do not feel significant inconvenience, the chances are, they will most likely not care. This was somewhat proven over the past years where 4G LTE data speeds and availability were vastly different for many carriers, but a single company could not control the majority of the market. I believe as long as AT&T continues its investment in this area to keep up with its competition, that will most likely be enough for the market. Significant portion of the public will not know or care for the download speed 7mbps slower.

Summary

The remaining AT&T will have about a 40% dividend payout ratio, which is lower than today's payout ratio, and the company will receive about $43 billion from the divesture. The company will be more focused on its core telecommunications business with better capital and financial position. WBD will focus on the media business away from the influence of the dividend giant. I believe this separation and specific area of focus will create a positive sentiment around both of the companies resulting in a significant valuation appreciation for both companies. WBD and AT&T's expected valuation multiples are extremely low compared to its competitors without any valid reason. Therefore, I believe AT&T is a strong buy today before the company finishes its dilution.