Summary

- Palantir's commercial revenue growth kept accelerating in Q1'22.

- Revenue outlook for Q2'22 is a minor disappointment, but long-term top line guidance is not changing.

- The market is massively overreacting and Palantir has become too cheap.

Shares of Palantir (NYSE:PLTR) cratered more than 21% after the software analytics company submitted its earnings card for the last quarter. The technology sell-off also broadened yesterday, adding selling pressure on Palantir. I believe the market completely overreacted to Palantir's earnings card as momentum in the commercial business kept building in the first-quarter. The market reaction indicates that the market has lost its mind and I am buying more shares of Palantir!

Palantir Q1'22 earnings card

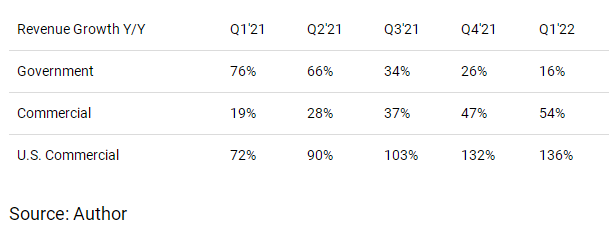

The data analytics company reported solid top line growth of 31% year over year to $446.4M in the first-quarter. Palantir guided for Q1'22 revenues of $443M in revenues, so the company beat its guidance by $3.4M. Government revenues were $241.8M, showing 16% year over year. Commercial revenues, a bright spot for growth for Palantir in recent quarters, especially in the U.S. commercial business, surged 54% year over year to $204.6M.

The commercial business continued to show a lot of promise in the first-quarter. While government revenue growth decelerated, the commercial business saw continual acceleration. Palantir's commercial revenue growth accelerated to 54% in Q1'22, with growth being chiefly driven by Palantir's U.S. commercial business. The private enterprise market is becoming increasingly important for Palantir, as the growth rates compiled in the table below show.

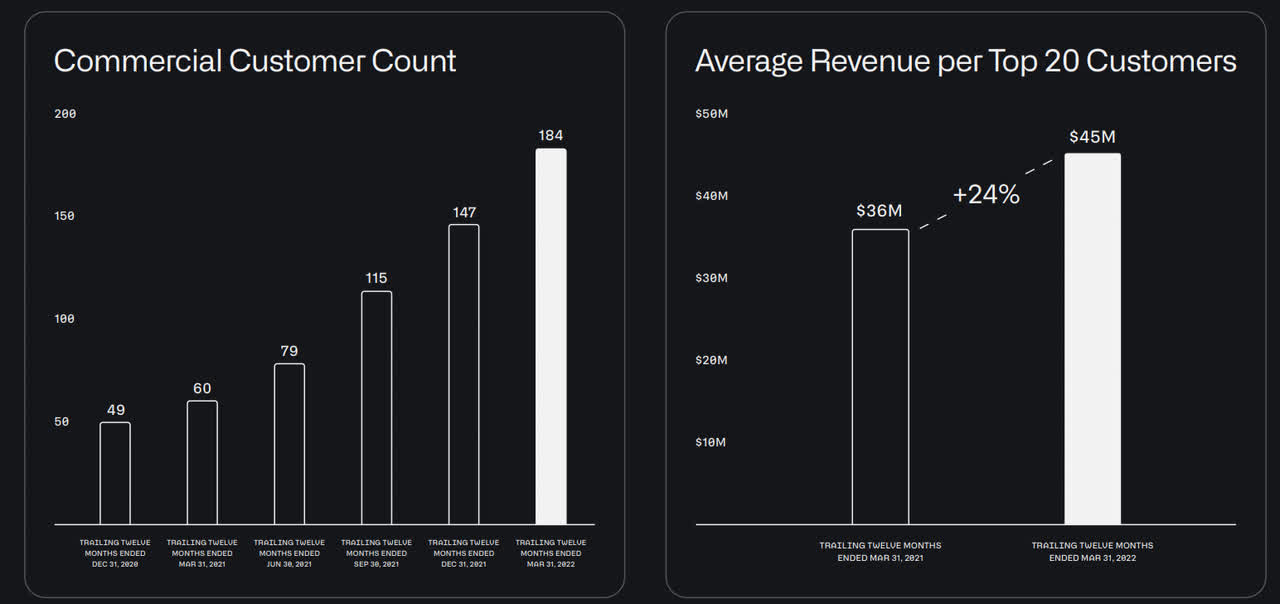

A key theme for Palantir in FY 2021 has been improving customer acquisition, which is a theme that is still highly relevant for the company. The data analytics firm added 40 new customers (net) to its client roster in the first-quarter, showing growth of 17% quarter over quarter and Palantir ended Q1'22 with 277 paying clients on its books. Once again, customer acquisition was especially strong in the commercial business where Palantir signed on 37 new customers just in the last quarter.

Equally important, Palantir continues to monetize its top customers better. Palantir generated 24% year over year growth in average revenue per top 20 customer, indicating that customers are willing to increase their spending on Palantir's products and services. The average top customers spend an average of $45M on Palantir's software solutions in Q1'22.

Palantir

Another way to look at Palantir's customer monetization is the net dollar retention rate/NDRR which in the first-quarter was 124%. Net dollar retention rates measure organic revenue growth from the same pool of customers, from one period to the next. Palantir's net dollar retention rate in Q4'21 was 131%, so the firm saw a quarter over quarter decline in its NDRR. But as long as net dollar retention rates stay above 100%, Palantir is growing its top line organically.

Palantir's first-quarter free cash flow disappoints

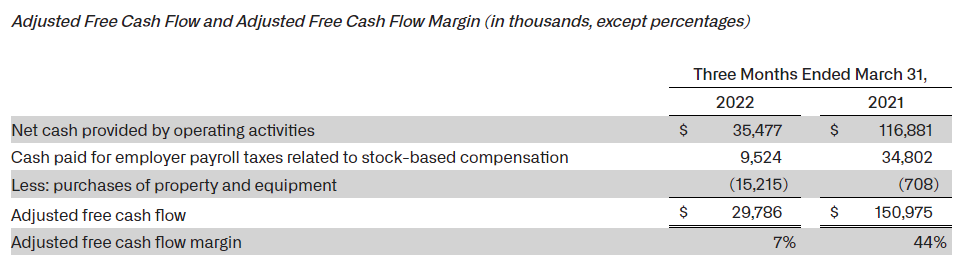

I will take the blame for my Q1'22 free cash flow estimate that was off by a large margin. I expected Palantir to generate more than $100M in Q1'22 free cash flow due to accelerating momentum in the U.S. commercial business and strong customer acquisition rates. Palantir's actual free cash flow was just $29.8M which calculates to a disappointing free cash flow margin of 7%. Much lower free cash flow than expected and a slightly weaker revenue outlook for Q2'22 are likely the reasons behind Palantir's 21% plunge on Monday.

Palantir

Slowing revenue growth?

Citing "developing geopolitical events", Palantir guided for Q2'22 revenues of $470M, which indicates 5% quarter over quarter growth. However, the guidance also implies just 25% growth year over year which marks a deceleration from the 30% growth rate that investors expected. Palantir, however, reaffirmed its 30% long term annual revenue growth goal. I don't believe investors have to worry about slowing top line growth right now. The firm said that it sees upside to its revenue guidance and Palantir likely is guiding carefully for the next quarter.

Shares of Palantir are currently deeply discounted

The 21% drawdown in pricing on Monday indicates to me that the market has lost its mind and the firm's commercial growth prospects are not evaluated rationally. Palantir made significant progress in the first-quarter regarding customer acquisition and monetization, especially in the U.S. commercial segment. For those reasons, I believe the market misjudges the earnings report and undervalues Palantir's prospects in the data analytics business.

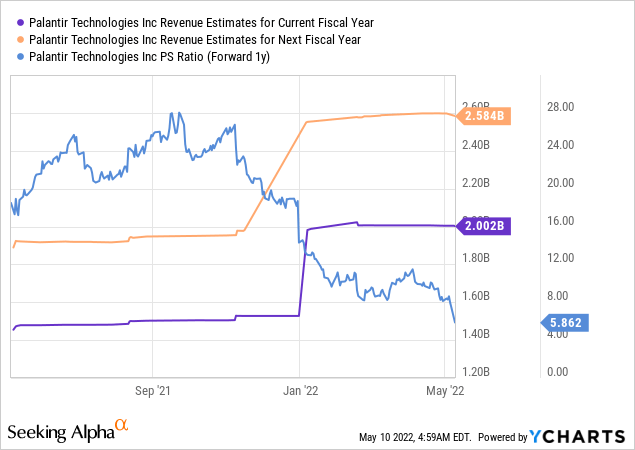

Shares of Palantir are currently valued at a P-S ratio of 5.9 X, based off of $2.6B in expected revenues in FY 2023. Palantir's P-S ratio was almost five times higher in FY 2021.

Risks with Palantir

There are a few risks with Palantir that refer to the company's high stock-based compensation and slowing top line growth. Palantir is remunerating executives with stock and options which results in shareholder dilution. The number of Palantir's outstanding shares increased 10% year over year in Q1'22 to 2.05B and this dilution is a problem for shareholders considering that the firm is currently not profitable.

Palantir

The other big risk I see with Palantir is the market environment. Clearly, investors don't value exposure to technology stocks right now. Although I believe Palantir's first-quarter earnings card was way better than the market reaction indicates, shares of Palantir could make new lows if current market trends continue.

Final thoughts

Panic has gripped the market. Technology stocks, including stocks of software analytics companies, are currently not favored and the tech sell-off clearly has potential to accelerate in the short term, which could potentially add even more pressure on Palantir's valuation.