It's been a year since the pandemic first blindsided the U.S., turning many jobs, forms of schooling and ways of socializing into stay-at-home events.

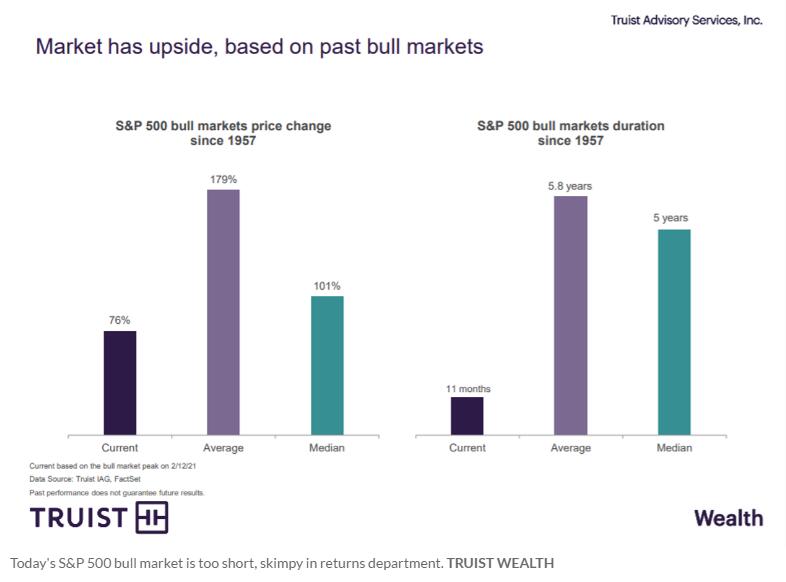

But it's only about 11 months since the new bull market for the S&P 500 started.

That's one of two key reasons why analysts at Truist Wealth think a sustained upswing for the S&P 500 index still has room to run.

This chart shows that the S&P 500's current bull-market run may be both too short-lived and too limited, in terms of price gains, to be over anytime soon, at least if the past six decades of performance apply during a pandemic.

U.S. stocks began to swoon into correction territory some 12 months ago, after the coronavirus pandemic first began to cut off travel and trade globally, a rocky period that was followed by the major U.S. equity benchmarks carving out fresh lows in late March.

But after quickly recouping their losses in 2020, stocks this year have continued to touch a series of all-time highs, thanks in part to trillions of dollars' worth of fiscal and monetary stimulus that's been sloshing through the economy, as policy makers look to shore up households hit hard by the crisis and to keep confidence and liquidity running high on Wall Street.

More recently, those same forces also have sparked concerns that the good times, post-COVID, might already be fully baked into stock prices and other financial assets, and that high-flying equities and riskier parts of the debt market could be headed for trouble if runaway inflation takes hold, or borrowing costs for companies and consumers get too high.

The S&P 500, Dow Jones Industrial Average and Nasdaq Composite Index were hit by volatile patches last week, as the 10-year Treasury yield spiked, and again on Wednesday when yields on the benchmark bond were spotted about 1% higher from a year prior, or near 1.47%.

All three major stock indexes closed lower Wednesday for a second day in a row, as bond yields climbed and technology stocks again came under selling pressure.

So how does today's rise from a low-rate environment compare with the '50s?

Truist analysts also have a chart showing that the S&P 500 and 10-year Treasury yields rates rose in concert during the 1950s.

"While there are many differences between the 1950s and today, there were some similarities, such as very high U.S. debt levels as a result of the war, an activist Fed and a postwar boom in the economy," wrote Keith Lerner, chief market strategist at Truist, in a Wednesday note. "Interest rates rose from 1.5% at the beginning of the decade to nearly 5% by the end. During the decade, despite two recessions, the S&P 500 rose 257% based on price and 487% on a total return basis."

This time around, Federal Reserve officials also has repeatedly vowed to avoid tightening monetary conditions, while keeping policy rates near zero and its $120 billion-per-month bond-buying program open until the economy fully recovers from the pandemic.

And yield-starved bond investors have welcomed the rush among highly rated companies this week to borrow, amid the prospects of higher borrowering costs.