Summary

- Palantir's post-earning sell-off underscores the market's disappointment with another weak showing for government sector revenues.

- It also accentuates the market's ongoing ignorance of Palantir's success in achieving commercial acceleration despite tightening financial conditions and an increasingly uncertain economic growth outlook.

- Palantir's continued effectiveness in deploying its "land and expand" business growth strategy, as evidence by 1Q22 government contract wins, has also been faced with market disregard.

- Although the ongoing development of macroeconomic challenges continue to fuel the contracting valuation environment across growth stocks, Palantir's fundamental outlook continues to be supported by a robust demand environment.

- In addition to continued commercial acceleration, Palantir is expected to benefit from backloaded government growth in the latter half as increasing global military spending in response to ongoing war efforts bolsters favourable near-term trends for the segment.

Palantir's stock (NYSE:PLTR) has taken a monthslong beating since reporting two consecutive quarters of mixed results, and after the Fed pivoted towards an aggressive policy stance in November upended the stock market. But regaining footing in the first quarter with a sales beat continues to underscore the company’s fundamental strength, bolstering the outlook on its multi-year growth target of 30% on an annual basis. Palantir continues to demonstrate market share gains across both the public and private sectors by encouraging adoption of its Foundry, Gotham and Apollo solutions through different deployment strategies, including modularization of existing offerings and industry-tailored solutions to better address different end user needs.

On the government front, the market appears disappointed still in the segment’s slowing growth, with the stock plummeting close to 20% in pre-market trading. But Palantir continues to demonstrate improvements by expanding existing opportunities with non-defense public agencies. Many renewed contracts with non-defense agencies this year, such as the U.S. Center for Disease Control and Prevention (“CDC”), are reflective of the value created by adoption of Palantir’s software under non-recurring COVID-era contracts, and underscores the continued effectiveness of the company’s “land and expand” strategy. Palantir has also played a supportive role in bolstering defense for the U.S. and its allies, as well as war relief efforts as the Russia-Ukraine conflict continues. The combination of increased market penetration into both non-defense and defense public agencies continues to reinforce sustained growth in Palantir’s government segment.

Meanwhile, Palantir’s commercial segment is also demonstrating continued strength, underscoring effectiveness of its recent roll-out of modularized enterprise solutions to break the barrier of IT resistance to complex new software structures like Foundry. By tailoring Foundry solutions to better suit end users’ needs, Palantir makes its offerings easier to digest and more relevant as digital transformation across the enterprise sector rapidly accelerates, driving better capitalization of related growth opportunities ahead. Recent management rhetoric on slowing SPAC investments are also welcomed news by many investors, as previous concerns of over-reliance on affiliated commercial sector revenues are putting sustainability of Palantir’s topline growth into question.

While the market performance of growth stocks like Palantir have continued to be challenged by the Fed pivot towards a more aggressive monetary policy stance to quell 40-year-high inflation, the ongoing Russia-Ukraine war and rapid acceleration of digital transformation trends continues to support the company’s fundamental performance by highlighting the value its technologies bring to the table. However, the stock likely faces further near-term volatility as investors continue to mull on the “[durability of Palantir’s] government business and yields on recent investments in commercial”, while broader markets await for further clarity on where current macroeconomic conditions are headed. Yet, with Palantir pushing through on its longer-term growth initiatives, including further expansion into non-U.S. opportunities and continued modularization of its offerings, to encourage mass market adoption and better capitalization of digitization opportunities in coming years, we expect favourable risk/reward at the stock’s current price levels for investors with patience.

Palantir - Brief Recap of 1Q22 Fundamental Performance

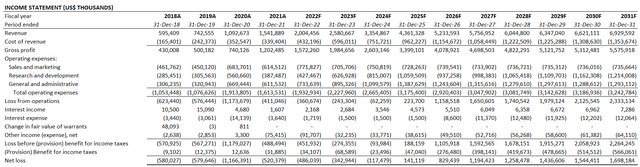

Palantir reported first quarter revenues of $446 million (+31% y/y; +3% q/q), beating consensus estimate of $443.51 million (+30% y/y; +2% q/q) and its previous guidance of $443 million (+30% y/y; +2% q/q). But government revenues continued to decelerate at 16% year-on-year growth in the first quarter, providing no respite to investors’ concerns experienced over the past two quarters. Meanwhile, commercial segment growth remains strong, with revenues increasing 54% year-on-year. In the U.S., enterprise opportunities drew in revenue growth of more than 136% year-on-year, which are impressive results that resonate with signs of an inflationary-resistant demand environment ahead of robust digitization trends.

Earnings fell short of expectations at $0.02 per share, compared with consensus estimate of $0.04 per share. But losses continue to narrow, showing positive progress towards profit realization by mid-decade.

Meanwhile, cash from operations remain strong, coming in at $35 million for the first quarter (8% margin), while adjusted free cash flows totalled $30 million (7% margin). As discussed in our previous coverage, Palantir’s robust balance sheet with $2.3 billion in cash on hand and zero debt remains a competitive advantage that will minimize its exposure to rising costs of capital ahead and maintain its ability to invest in continued growth.

Expectations for Backloaded Government Growth

Palantir continues to show favourable developments this year across both its government and commercial segments based on recent deal wins observed, bolstering sustainability of its multi-year growth target of more than 30% on an annual basis. While government revenue growth continued to decelerate for the third consecutive quarter, we are expecting some of the new deal wins in response to the ongoing Russia-Ukraine war to materialize further in the latter half of the year. This is also corroborated by management’s expectations for a “wide range of potential upside to [its second quarter guidance], including those driven by [Palantir’s] role in responding to developing geopolitical events”. Paired with continuing momentum from Palantir’s commercial segment, the company continues to show favourable fundamental growth prospects in line with its long-term target despite tightening financial conditions in the current market climate.

Boosted Global Military Spending Tailwinds

On the military front, global governments have been bolstering their defense spending in response to the ongoing Russia-Ukraine war. U.S. allies in Europe are increasing adoption of Palantir’s solutions to facilitate current war efforts spanning “the distribution of materials such as food and beds to Ukrainian refugees…, [to powering] military response against Russia’s invasion of Ukraine”. The war-driven tailwinds for Palantir are further corroborated by the spike in global military spending this year, which has surpassed $2 trillion for the first time and “looks set to rise further as European countries beef up their armed forces in response to Ukraine war”.

Europe:European military expenditures have been increasing for seven years straight, and the trend is expected to “accelerate and intensify” in response to the latest geopolitical crisis in Ukraine. The development bodes favourably with Palantir’s amped up efforts in penetrating opportunities outside of the U.S., especially in Europe. Last quarter, the company announced plans to expand its salesforce in Europe with at least 175 experienced hires this year to accelerate market penetration across the region’s public sector. The announcement came shortly after the company appointed Philippe Mathieu as President of Palantir EMEA to take charge of leading Palantir’s penetration into the sizable addressable market in Europe. And these efforts have already started to pay off nicely, as evidenced by Palantir’s latest contract win with the U.K. Ministry of Defence (“MoD”). Valued at $12.5 million, the contract would require Palantir to implement its Foundry platform across the MoD to enable cost efficiencies by “automating work and reducing data-processing time”.

Defense spending by the European government alone accounts for a fifth of the global total, underscoring the massive growth opportunities that await Palantir. This is further bolstered by “early indications that modernizing and upgrading weapons systems will be a key priority” for the European governments. Many of the challenges observed in the ongoing Russia-Ukraine war have been “related to things like logistics, fuel, tires and secure communications”, which suggests that a war chest of weapons is insufficient in modern-day warfare and must be complemented by technologies like AI and data analytics to ensure adequate progress. This accordingly reflects Palantir’s improved position in benefiting from a “favourable government spending environment”, especially in Europe, over coming years.

U.S.: Similar tailwinds are expected from the U.S., which is currently the world’s largest military spender. The U.S. government allocated $801 billion to the armed forces last year, representing “as much as 39% of global expenditures”. There has also been an increasing deployment of related funds towards “military research and development, suggesting that the U.S. is focusing more on next-generation technologies”, which bolsters Palantir’s longer-term government segment outlook. Looking ahead, President Biden has recently requested “$813.3 billion in national security spending, including $773 billion for the Pentagon, in the federal budget” for fiscal 2023. The proposed budget represents a 4% increase from the current fiscal year and exceeds the fiscal 2023 budget projected by the White House a year ago by more than $40 billion. In addition to the ongoing Russia-Ukraine war, the U.S. government’s beefed-up budget also “reflects the increasing military challenge from China”.

A meaningful portion of the allocated budget to the Pentagon – about $130 billion of the $773 billion – will be deployed towards “development of costly new defense systems…, [including] accelerated research into hypersonics and AI”, representing an increase of $15.6 billion compared to projections outlined in the fiscal 2023 budget made last year. But with rising inflationary pressures, some industry experts are expending an even larger increase to related spending in the coming fiscal year, underscoring even greater opportunities for next-generation warfare technology providers like Palantir.

Expanding Adjacent Non-Military Opportunities

Palantir’s effective deployment of COVID-era solutions and support to various non-military public agencies in recent years has also continued to bolster its growing share of related government procurement contracts. In the core U.S. market alone, non-defense agency contracts represented more than 52% of total public sector awards received by the company to date. This continues to underscore Palantir’s ability in diversifying government segment growth drivers and benefiting from opportunities related to major non-defense government agencies. Continued penetration of non-defense government opportunities, which represents about 3% to 4% of annual GDP in the U.S. alone, paired with increased military expenditure in the near-term are expected to reinforce Palantir’s government segment performance:

- COVID-19 Response for the CDC: The latest contract forged between Palantir and the CDC pertaining to the U.S. government’s ongoing COVID-19 response efforts highlights the company’s continued effectiveness in executing its land and expand business strategy. The expanded partnership underscores Palantir’s effective job as a “trusted technology partner” during the pandemic-era. Specifically, the latest partnership with the CDC results from Palantir’s success in helping the Department of Health and Human Services (“HHS”) with vaccine distribution in mid-2020. Palantir’s solutions have been procured under the latest contract with the CDC, valued at $5.3 million, to support the department’s “key distribution and supply chain efforts” pertaining to ongoing COVID-19 response efforts.

- CDC DCIPHER Program Extension: The CDC has expanded its use of Palantir’s solutions in support of the “Data Collation and Integration for Public Health Event Response” (“DCIPHER”) Program. Palantir has been supporting the roll-out of the CDC’s DCIPHER Program since 2010. The latest extension will further Palantir’s participation in the CDC’s ongoing efforts related to modernizing the agency’s data management system, and supporting “time-sensitive data integration, management and analysis that widespread events require”.

- HHS SHARE Blanket Purchase Agreement: Earlier this month, Palantir was rewarded another contract by the HHS to support its “5-year Solutioning with Holistic Analytics Restructure for the Enterprise (“SHARE”)” program under a Blanket Purchase Agreement (“BPA”). Valued at $90 million, the BPA will require Palantir’s platform be implemented across the HHS’ “many agencies and missions…to support their work”. Palantir was selected based on its proven strength in delivering effective “built-in data protection features, innovative technology, and common security framework”, which further corroborates our observations that the company’s achievements with non-defense public agencies during the pandemic-era have been a beneficial trial period that is driving today’s expansion. Palantir’s initial obligation under the BPA is a “10.5 month, multi-million-dollar contract to support HHS’ core administrative data and applications through a vertically integrated platform that allows teams to configure low to no code applications to manage, ingest, and access data securely, across business domains” using its Foundry platform.

Commercial Acceleration

Acceleration in Palantir’s commercial sector has been consistently gaining momentum in recent quarters. Despite tightening financial conditions in the economy, the segment’s latest results continue to underscore the critical role that Palantir plays in the enterprise sector’s ongoing digital transformation efforts. More than half of the corporate scene have expressed that they would rather “tighten the belt” in other parts of the business than to miss out on digital transformation, which is considered a strategic investment in differentiating themselves from competitors, while also enabling cost efficiencies. Commercial customers are increasing demand for tools to make sense of their massive data troves. To date, only 4% of companies claim to have a "highly sophisticated approach to leveraging data”, leaving sizable growth opportunities for Palantir over coming years.

Modularization:The company’s continued commitment to modularization and honing its offerings to better suit end users’ needs are also bolstering its capitalization of opportunities stemming from demand environment. In addition to Foundry for Builders, which we have previously analyzed as an effective tool for driving mass market adoption in the corporate sector over coming years, Palantir has also been ramping up deployment of modular offerings like “Carbon Emissions Management” and “Anti-Money Laundering / Know Your Client” solutions to increase its appeal to the commercial sector, including the emerging crypto sector, which stands to expose Palantir to a broader market that is expected to grow into a $67 billion opportunity by mid-decade.

Industry-Specific Solutions:There has also been a consistent trend of leveraging third-party expertise in the development of industry-tailored versions of its Foundry platform. After forging a $25 million multi-year deal with Hyundai Heavy earlier this year to co-develop and commercialize software tools curated for breaking down siloed data fields across relevant workflows spanning shipbuilding to industrial machinery processes, Palantir is back at it again with a similar deal forged with Jacobs (J), a consulting and project delivery expert for both the public and private sectors.

Palantir and Jacobs will collaborate on the development and launch of a “joint data analytics offering to support public and private sector clients in solving their most complex water infrastructure problems”. Built on Palantir’s Foundry platform, the joint data analytics offering will also be leveraging Jacobs’ existing expertise in providing operations and maintenance (“O&M”) solutions to the water sector, as well as its “proprietary machine learning modules and wastewater process optimization tools”. The joint analytics tool aims at driving insights that can help increase water plant performance, cost efficiencies, security from cyber threats, and compliance with ESG goals – all of which are pressing needs to support the evolution of critical water infrastructure required to satisfy rising “global demand for clean water, more stringent regulatory issues, and increasing environmental concerns”. With the global water and wastewater treatment addressable market expected to exceed $200 billion by mid-decade, Palantir’s latest foray into the water infrastructure sector with the help of Jacobs marks another significant step towards greater commercial penetration.

Seamless Digital Migration with Apollo:In addition to developments made with Foundry that are accelerating growth for Palantir’s commercial segment, the company’s recent roll-out of a new suite of offerings available within Apollo also heightens its appeal to the enterprise sector. Apollo is an operating system developed by Palantir to facilitate “autonomous software deployment across environments” faster and in a more efficient way to ensure scalability. Apollo has already “managed the deployment, security, and upgrades for Palantir’s software, including 500+ independently released microservices across 300+ unique environments”, accentuating the system’s proven effectiveness.

The latest product additions within Apollo include “Cloud Portability”, which allows “organizations to maintain flexibility across cloud providers” by housing different cloud provider managed operating systems under one roof. This creates a particular appeal to the corporate sector’s increasing migration of workloads from legacy IT systems to the cloud, which is considered a business essential that drives “better economies, more innovation and greater speed”. With more than half of global corporations indicating plans to allocate a significant share of budgeted investments to cloud-related projects over the next two years, the Apollo operating system and its newly curated offerings stand to further Palantir’s reach into related opportunities over coming years.

Fundamental Estimate Update

Adjusting our latest Palantir financial forecast for its actual first quarter financial results, and growth outlook based on recent developments discussed in the foregoing analysis, the company remains on a positive track towards reaching +30% revenue growth this year. Our base case forecast expects revenues to total $2.0 billion by the end of the year (+30% y/y), driven by continued commercial acceleration, as well as restored government momentum in the latter half resulting from solution deployments related to the ongoing Russia-Ukraine war.

Consistent with narrowing losses observed in recent quarters, the company’s expected trajectory towards profits by mid-decade remains intact. Operating margins are expected to further improve over time as Palantir continues to ramp deployment of new and existing offerings and achieve greater economies of scale. Share-based compensation expenses, which investors consider a sore spot for the company, are also expected to further improve and taper towards lower levels by mid-decade. Share-based compensation as a percentage of total revenues has consistently improved from 116% in 2020 (4Q20: 75%) to about 50% in 2021 (4Q21: 39%) and 33% in 1Q22. This continues to signal Palantir's increasing balance between top talent retention through generous compensation packages and growth-driven economies of scale to facilitate meaningful margin expansion towards GAAP-based net profits by 2025.

PLTR Stock Valuation Update

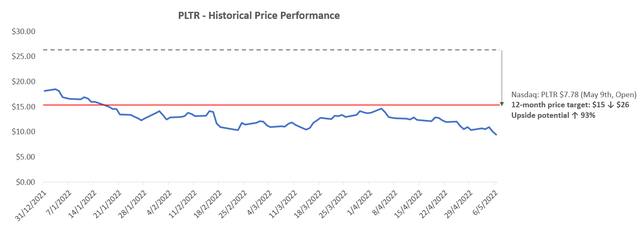

The market continues to be extremely unforgiving towards signs of near-term underperformance in growth stocks like Palantir. The stock’s massive pullback in value in recent months as a result of three consecutive quarters of decelerating government growth has effectively erased Palantir’s previous premium to the broader SaaS peer group. At under $8 per share (May 9th), Palantir current trades at about 6x EV/’23 sales, which is below the SaaS mean of 8.1x and median of 7.8x. Considering Palantir’s continued fundamental strength, which includes 1) continued top-line growth expected at more than 30% per year as analyzed in the foregoing analysis, 2) self-sufficient, cash-positive day-to-day operations, and 3) a robust balance sheet with $2.3 billion in cash on hand and zero debt to facilitate continued growth with minimal exposure to rising costs of capital, we are confident in the return of a favourable risk-reward payoff at current price levels for patient long-term investors.

Considering the ongoing compression of valuation multiples observed across the SaaS peer group in response to still-evolving economic uncertainties stemming from macro challenges including runaway inflation and tightening monetary policy, we are adjusting our 12-month price target for the stock from $26 to $15. Our near-term price target implies a 10.8x EV/’23 sales to better reflect the currently contracted valuation environment for SaaS stocks, compensated by Palantir’s increasing appeal to commercial sector digitization needs, and its “favourable government spending environment” expected in the near-term as discussed in earlier sections.

Conclusion

While we have tapered our near-term expectations for the stock considering the current risk-off environment for growth equities, we remain optimistic on its longer-term upside potential. Palantir’s software solutions remain the best-in-class for addressing critical data management and analytics needs across both the public and private sector. With robust customer growth still, and a strong demand environment ahead of global digitization trends, Palantir continues to sit on a mountain of opportunities stemming from a market that is still significantly under-addressed. This accordingly underscores further fundamental growth in coming years, buoying better valuation prospects over the longer-term especially when the current market storm subsides.

Author's Note: Thank you for reading my analysis. Please note that we will be launching a Livy Investment Research Marketplace service on June 1. The service will allow you to follow my coverage portfolio, interact with me directly, and participate in chat rooms with other subscribers. Early subscribers will receive a legacy discount at $249 per year. Stay tuned for more details as we ramp up to launch in the coming months.