Alibaba's (NYSE:BABA) shares rallied 15% after the Chinese e-Commerce company submitted earnings results for the last quarter of FY 2022 on Thursday. Alibaba easily sailed past revenue and earnings predictions and I believe sentiment regarding Chinese companies has deteriorated too much at this point. Although Alibaba skipped its guidance for FY 2023, the firm's valuation still makes very little sense. Investors are underpricing Alibaba’s earnings potential!

Previous expectations

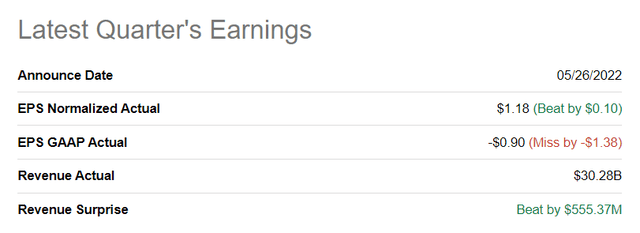

In my previous work on Alibaba, I mentioned the very real possibility of Alibaba outperforming EPS predictions on Thursday which have gone through a significant downward revision cycle over the last year. Low expectations were the main reason why I thought Alibaba could outperform low consensus EPS predictions. And this is what Alibaba did: The company reported Q4’22 adjusted EPS of $1.18 which beat predictions by $0.10. Additionally, Alibaba beat on revenues as well.

Seeking Alpha

Alibaba’s e-Commerce growth

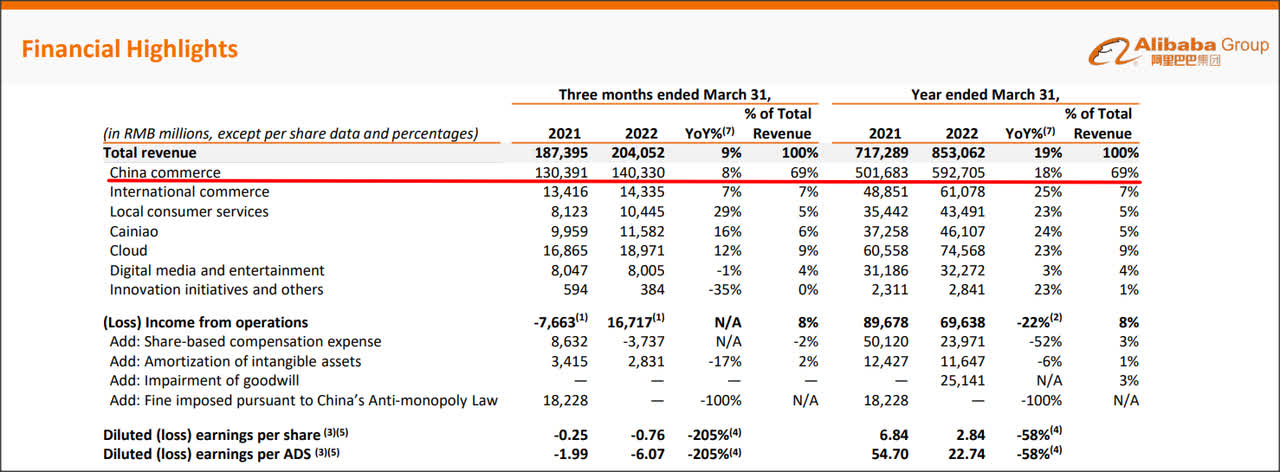

Overall, Alibaba’s revenues increased 9% in the last quarter to 204.1B Chinese Yuan which calculates to $32.2B. Alibaba’s core China e-Commerce revenues increased 8% year over year to 140.3B Chinese Yuan ($22.1B), which was an improvement over the previous quarter which saw 7% top line growth. So, Alibaba slightly improved its performance in its most important business quarter over quarter. Alibaba also saw continual strength in Local Consumer Services where revenues surged 29% year over year to $10.4B Chinese Yuan ($1.6B) and the Cloud segment which saw its revenues increase by 12% year over year to 19.0B Chinese Yuan ($3.0B).

Alibaba

What stood out positively from Alibaba’s earnings sheet was that the company continued to make progress expanding its e-Commerce platform despite a challenged macro environment. Alibaba added 28M new accounts to its ecosystem in the last quarter, the majority of which (25M) were added in China. Alibaba’s domestic e-Commerce business is still the firm’s largest revenue source, contributing 69% of total revenues. However, Alibaba has a huge opportunity to grow its other businesses as well, especially its logistics operations which are vertically integrated into Alibaba’s e-Commerce operations, and its Cloud segment. I recently described the progress Alibaba is making in the Cloud business.

Alibaba

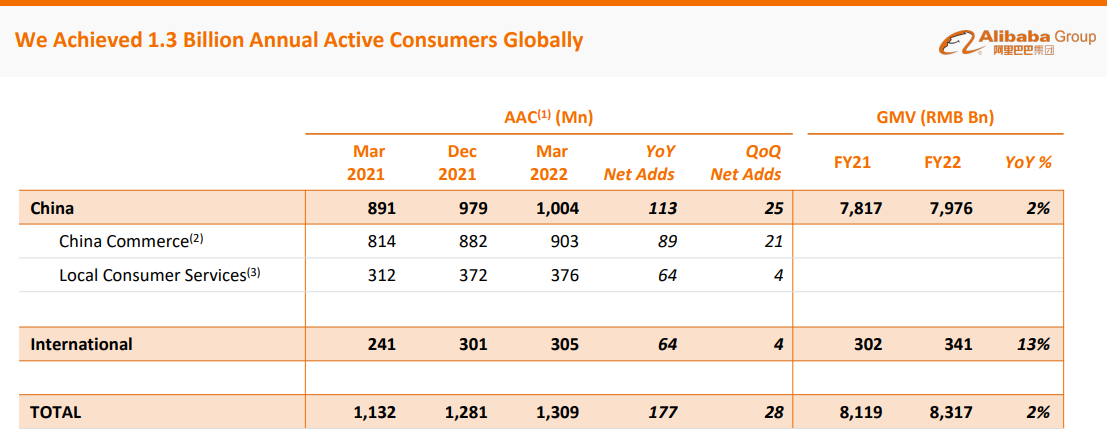

Alibaba ended the quarter with 1.3B active customer accounts in its enterprise. Over the last year, Alibaba added a massive 177M new customers to its platform which creates a base for long term earnings and free cash flow growth.

Alibaba’s share buybacks

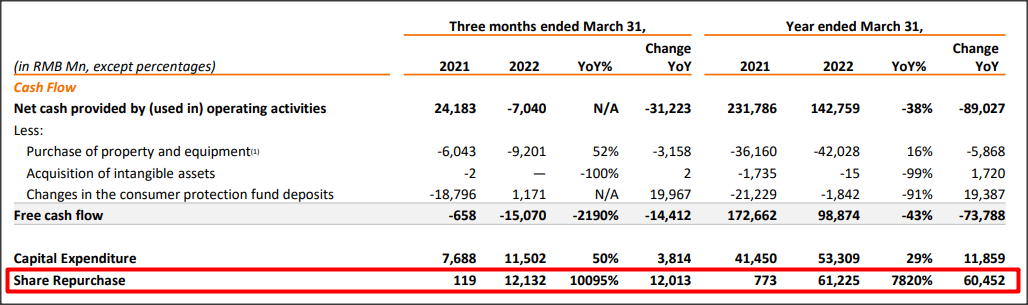

Before Alibaba released earnings, I mentioned that the company likely used its free cash flow in the last quarter to repurchase a ton of shares. It was obvious to me that the e-Commerce company would repurchase a lot of shares considering that Alibaba just up-sized its stock buyback from $15B to $25B at the time and that the stock traded at unreasonably low prices in March.

I like it when companies increase their buybacks when stock valuations are depressed and Alibaba did in fact repurchase a significant amount of shares in the last quarter. In Q4’22, Alibaba repurchased approximately 17.8M American Depositary Shares for about $2.0B. I expected a minimum share repurchase of $2.0B. In the last twelve months, Alibaba repurchased 60M American Depositary Shares for a total consideration of $9.6B.

Alibaba

Skipped earnings guidance

Alibaba did not provide earnings guidance which it normally does at the beginning of the fiscal year. The e-Commerce firm cited uncertainties related to COVID-19 as a reason not to provide guidance. Normally, a lack of guidance is not well received and stocks of companies that don’t guide are punished by the market. In this case, however, things are different. Alibaba’s shares have been so battered so much since the fourth-quarter of 2020 that investors cheer results even if they are more mediocre.

Alibaba’s valuation is wrong: Undervalued e-Commerce prospects

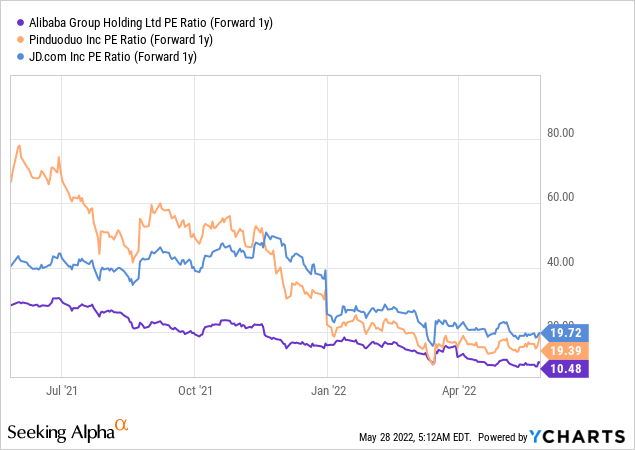

Alibaba’s stock market valuation makes very little sense to me. This is because, for one, Alibaba is very profitable. Alibaba generated net income of 47.1B Chinese Yuan ($7.4B) in FY 2022 while adjusted net income was 136.4B or $21.5B. There is some serious profitability in Alibaba’s business and investors don’t seem to appreciate this right now. Additionally, we are dealing with one of the largest e-Commerce empires in the world regarding account size and reach, but Alibaba's valuation still does not reflect those factors. Shares of Alibaba trade at a P-E ratio of 10 X. JD.com (JD), for example, has a P-E ratio nearly twice as high as Alibaba's. Alibaba's historical valuation shows a P-E ratio as high as 30 X. As wrong as Alibaba's valuation is, it represents deep value and low risk.

Risks with Alibaba

Alibaba faces continual top line risks related to a slowdown in the Chinese e-Commerce market. While Alibaba is investing in other businesses to diversify its revenue mix, a continual moderation in top line growth poses a risk for Alibaba and the stock. What would change my mind about Alibaba is if earnings and free cash flow prospects in the e-Commerce business seriously deteriorated or Beijing announced new crackdowns on the company.

Final thoughts

I expected Alibaba to do better than estimates in Q4’22, in large part because investor expectations have been driven too low. Given the circumstances with COVID-19 lockdowns and a regulatory onslaught in the last year, Alibaba did a good job in squeezing out 9% revenue growth.

Alibaba does have some problems, like slowing top line growth and reliance on domestic e-Commerce transactions, but the firm’s irrationally low valuation is not of them. Alibaba added a significant number (177M) of new accounts in the last twelve months which speaks to the strength and the appeal of Alibaba’s various e-Commerce platforms. Alibaba’s growth is still widely undervalued and I believe the valuation is just plain wrong!