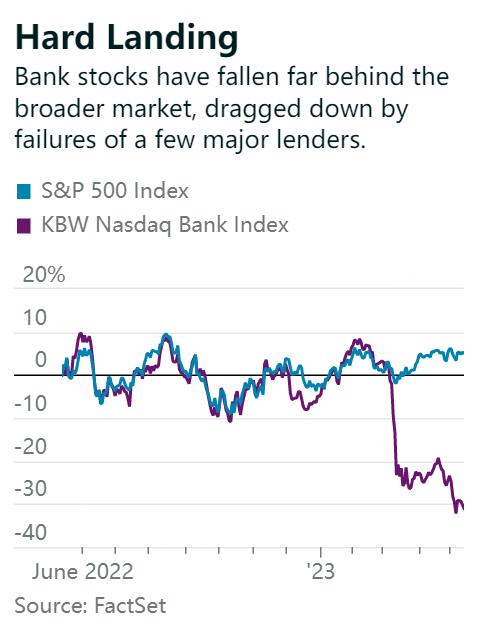

Banks are heading for a “new world order.” The outlook comes from investment firm KBW, referring to a shakeout following the failures of First Republic Bank, Silicon Valley Bank, and Signature Bank. Individually, none was big enough to upend the industry. Together, their collapse is helping to reshape it.

Investors, regulators, and companies are reassessing deposit flows, loan books, and balance sheets buckling from higher interest rates. Some firms are feeding off the turmoil, notably JPMorgan Chase (ticker: JPM), First Citizens BancShares (FCNCA) and New York Community Bancorp (NYCB), which snapped up deposits and assets of the failed banks at discounts. But regional lenders aren’t out of the woods, as firms like PacWest (PACW) continue to lose deposits—including a 9.5% drop in the past week.

The next 12 months will be rocky, but there are opportunities in stocks that may be unduly depressed. Pressured by the Federal Reserve’s interest-rate hikes, banks are sitting on huge losses in “safe” securities like Treasuries and are pulling back on loans. Another worry is losses in commercial real estate. If the economy tips into a recession, profit estimates would come down as banks rebuild capital and reserves, while loan growth dwindles.

Regulation is also an overhang as federal and state supervisors investigate the failures—including their own—and try to plug oversight holes. Big banks face higher insurance charges from the Federal Deposit Insurance Corp., since the FDIC spent $15.8 billion bailing out uninsured depositors of the failed banks. The FDIC now plans to levy a special charge on uninsured deposits above $5 billion, aiming to raise nearly $16 billion starting next year. Large banks with more than $50 billion in assets are expected to pay 95% of the cost.

“Ultimately, the markets will heal, and confidence will be restored,” says Christopher McGratty, KBW’s head of U.S. bank research. But it’s going to take time for the fog to lift on regulation. Valuations look attractive, he says, but there are more important considerations, including the regulatory overhang and economic outlook.

The New Bank Landscape

While the shakeout is in its early stages, contours are forming. One is that JPMorgan and a few other megafirms should benefit. Banks with more than $250 billion in assets have long been held to stiffer stress-test rules and capital requirements than those in a category just below. That effectively de-risked the giants’ securities and asset portfolios, enabling them to withstand the pressure of higher rates better than smaller banks that wound up taking more interest-rate risk.

Deposit trends indicate that the giants are benefiting from a perceived flight to safety. JPMorgan reported a $50 billion increase in deposits in March, before its First Republic acquisition in early May. Its deposits rose 2% in the first quarter to $2.38 trillion.

Yet JPMorgan, like other banks, has lost deposits for much of the last year, partly because it doesn’t pay as much interest in checking and savings accounts as money-market funds. JPMorgan’s deposits are down by nearly $200 billion from the first quarter of 2022. That has been an industrywide slow burn as the Fed hiked the federal-funds rate from about zero percent to roughly 5%.

“From a very high level, the bank space has never seen such outflows of deposits, in either total dollars or percentage, than what has taken place over the past year,” said analysts at boutique investment bank Hovde Group in a note. The big banks have plenty of asset cushions, the analysts noted. But it’s still too early to tell whether small banks are back to normal or if their stocks have hit bottom.

The spate of bank failures raises another concern: Banks are sitting on an estimated $2.2 trillion of unrealized losses on securities, according to Stanford University finance professor Amit Seru. About 10% of banks have larger unrealized losses than Silicon Valley Bank, he estimates. Most of those losses are in Treasuries and agency-backed mortgage securities that lost value as rates spiked.

Ideally, banks won’t have to sell bonds at a loss, holding them to maturity and getting 100 cents on the dollar. The Fed and Treasury are providing emergency liquidity facilities that could help lenders avoid the fate of SVB and others that faced bank runs triggered partly by disclosures of losses on bondholdings.

One problem that isn’t going away near term: commercial real estate. Banks are pulling back sharply on real estate loans amid widespread price declines and weakness in office properties. The National Association of Realtors points to a record-high office vacancy rate of 12.9% compared with the previous year’s 12%.

Banks hold about $2.2 trillion in outstanding commercial real estate debt, the Fed said in a recent report. More than 70% is with lenders that have less than $100 billion of assets—big players in local business, autos, and construction loans. If those regionals keep pulling back on credit, it could slow the economy almost as much as one or two more quarter-point rate hikes, analysts say.

A regulatory reckoning is coming. Lawmakers have held hearings on the role of the San Francisco Fed in the SVB collapse. The Fed, in a recent report, said SVB’s failure exposed regulatory gaps, including supervision that lacked force and urgency.

Another problem: a hole in stress testing and capital requirements. Banks with more than $250 billion in assets are subject to international standards on oversight and capital rules, since they’re considered globally systemically important. But the rules are more lenient for banks just below that level, in part thanks to industry lobbying. The Fed has proposed new liquidity and reporting requirements for banks with more than $100 billion in assets.

The stress tests need an overhaul, too. The tests failed to measure the effect of rising rates in all but two of the years since the Fed began the exercise after the 2008-09 financial crisis. Instead, it tested banks for their ability to withstand a period of low inflation and falling rates—the opposite of the economic dynamics today.

California’s financial regulator, which oversaw SVB, says it will increase scrutiny of banks with more than $50 billion in assets. Uninsured deposits will also be more closely assessed, along with the role that mobile banking apps and social media may play in accelerating a bank run.

Analysts at KBW expect a wave of mergers, especially for banks with a sizable sum of assets in the $80 billion to $120 billion range. “Longer term, we believe there will be very few banks operating within this asset range,” they said in a recent note.

How to Invest Amid the Turmoil

The selloff may yield profits for investors willing to hold through a downturn. The sector is off more than 25% this year, and even if a recession hits in 2024, large-cap regional banks could still deliver 15% returns on tangible common equity, estimates UBS analyst Erika Najarian. For large banks, the new FDIC fees will shave an average 4% off earnings in 2024 and 2025, she estimates, though it will cause only “modest pain.”

Miles Lewis, a financial sector stockpicker for Royce Investments, points out that tangible book values—a measure of liquidation value—in many cases are below where they were in the financial crisis. New regulation aimed at the larger banks is unlikely to touch the smaller banks in a material way, he adds.

One stock he likes is BankUnited (BKU). The East Coast regional lender has a big presence in Florida and New York, and could benefit from Signature’s demise by picking up commercial accounts. The stock is down 51% this year on fears of a deposit flight, pushing it to 50% of tangible book value; Lewis thinks that it will rebound and expects the bank to cover its dividend, recently yielding 6.5%.

Valley National Bancorp (VLY), based in New Jersey, is another one he favors. It was a bidder for SVB, a sign of its financial strength, and insiders have been snapping up shares, which also trade at about half of book value and with a 6.5% yield.

Home BancShares (HOMB) of Conway, Ark., has 70% of its deposits in Florida and Texas—markets with healthy economies and population growth. It trades slightly above book value around $20 a share, which gives it currency for acquisitions. “This is a port in the storm,” Lewis says.

Steven Alexopoulos, a bank analyst at J.P. Morgan, recently upgraded Western Alliance Bancorp (WAL), Zions Bancorp (ZION), and Comerica (CMA) to Overweight. All have been caught in the regional-bank storm, tanking their stocks. But it “won’t take much to see a significant intermediate-term favorable rerating,” he says, referring to upward revisions of valuations.

There is also the newly enriched king: JPMorgan. The bank added $103.9 billion in deposits from First Republic, taking its total above 10% of the U.S. total. The firm added an advisory business for wealthy clients, and said the deal would lift net income by $500 million a year. That’s incidental for the firm, which booked $12.6 billion in net income in the first quarter.

The stock trades at 9.5 times estimated 12-month earnings, a 20% discount to its five-year average. Like other banks, it should rally on signs of a Fed pivot to lower rates. Investors can pick up a 2.9% dividend yield while waiting for better days ahead.