TSM Q2: Hidden profit warning under the popularity!

Before the market on July 15th,$Taiwan Semiconductor Manufacturing(TSM)$ , the king of chip foundry, announced Q2 financial report. From the data point of view, the revenue continued to soar under the shortage of semiconductor supply, but the profitability turned downward under the pressure of capital expenditure and raw material price increase, and the net profit fell short of market expectations.

Before the US stock market, Taiwan Semiconductor Manufacturing shares fell slightly by 1.6%.

Revenue is hot, and net profit has hidden warning!

Taiwan Semiconductor Manufacturing's revenue has never been a secret. At the beginning of each month, Taiwan Semiconductor Manufacturing will announce the revenue of last month in official website. Therefore, Taiwan Semiconductor Manufacturing's quarterly revenue is basically winning numbers.

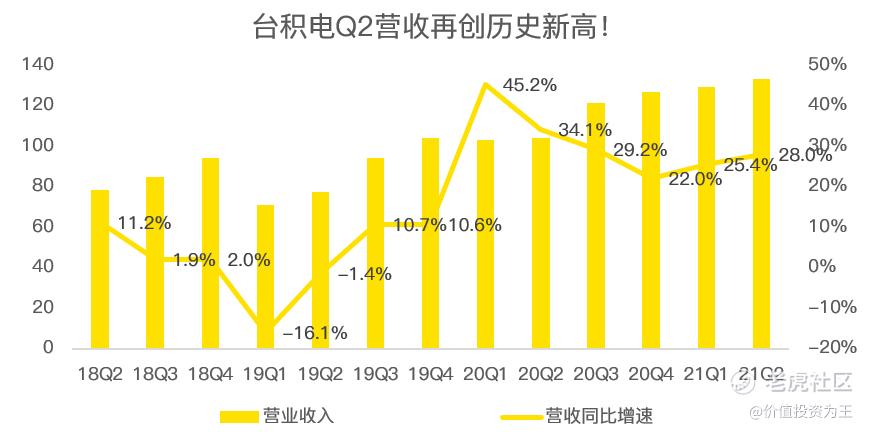

In the second quarter of 2021, Taiwan Semiconductor Manufacturing gained US $13.289 billion in revenue, up 28% year-on-year, slightly exceeding market expectations.

When Q1 financial report was released, Taiwan Semiconductor Manufacturing gave a revenue guide range of 12.9-13.2 billion US dollars in the second quarter. From the actual operating results, Taiwan Semiconductor Manufacturing once again made history and set the best revenue record in history.

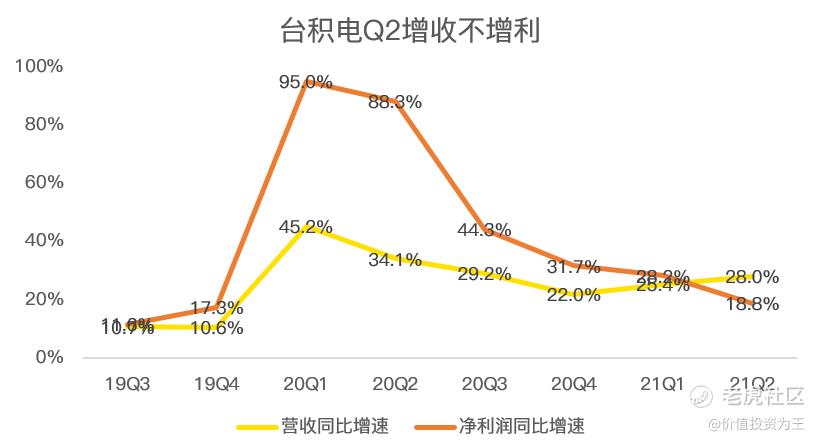

Although the growth rate of revenue is still hot, the net profit is less than expected.

Taiwan Semiconductor Manufacturing Q2 achieved a net profit of USD 4.802 billion, up 18.8% year-on-year, which was less than the market expectation of USD 4.831 billion.

In absolute terms, the actual net profit is not much different from the expected one, but it is worth noting that the growth rate of Q2 net profit breaks the previous practice of being higher than the growth rate of revenue.

In the history of resumption of trading, Taiwan Semiconductor Manufacturing's net profit growth rate is often higher than its revenue growth rate, but from the first quarter of 2021, the gap between them became smaller and smaller, until it was upside down in the second quarter.

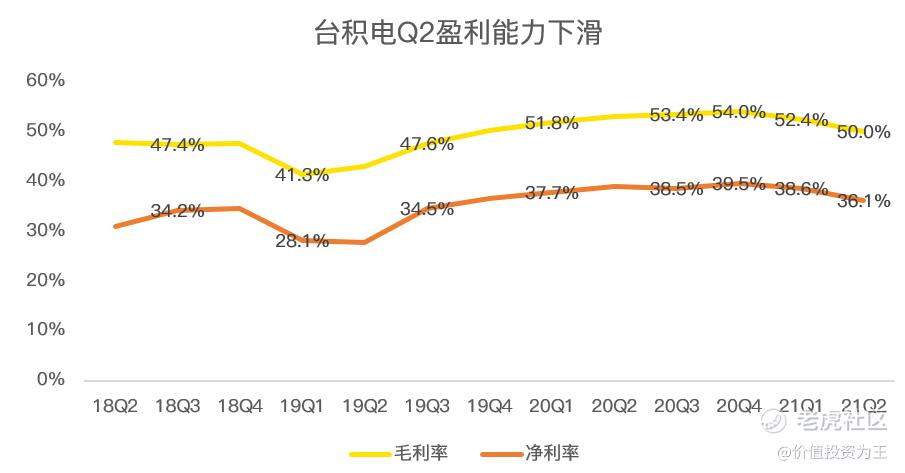

The main reason for the lower than expected net profit is the decline in gross profit margin.

In the second quarter, Taiwan Semiconductor Manufacturing's gross profit margin was 50%, significantly lower than 53% in the same period last year, but still in the range of 49.5%-51.5% given by the company in the first quarter.

In the financial report, the reason for the decline in gross profit margin given by the company is the slow improvement of 5 nm process cost.

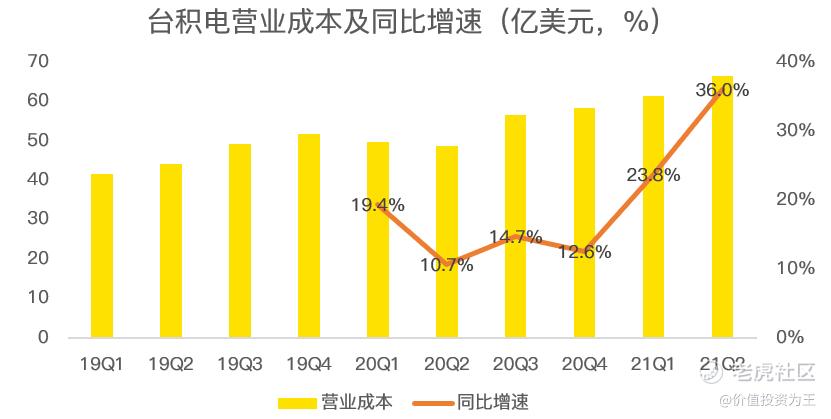

From the year-on-year growth rate of operating costs, the operating costs in the second quarter were US $6.64 billion, up 36% year-on-year, which was significantly higher than the 28% revenue growth rate.

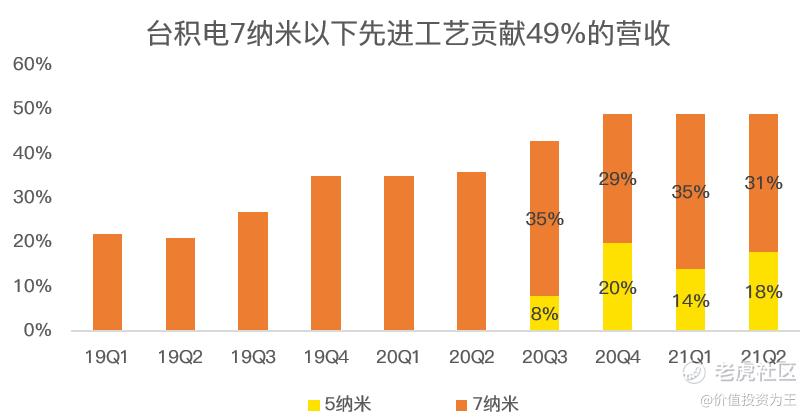

In terms of revenue composition, 5 nm technology contributed 18% of revenue and 7 nm contributed 31% in the second quarter, which together contributed 49% of revenue, which was the same as that in the first quarter.

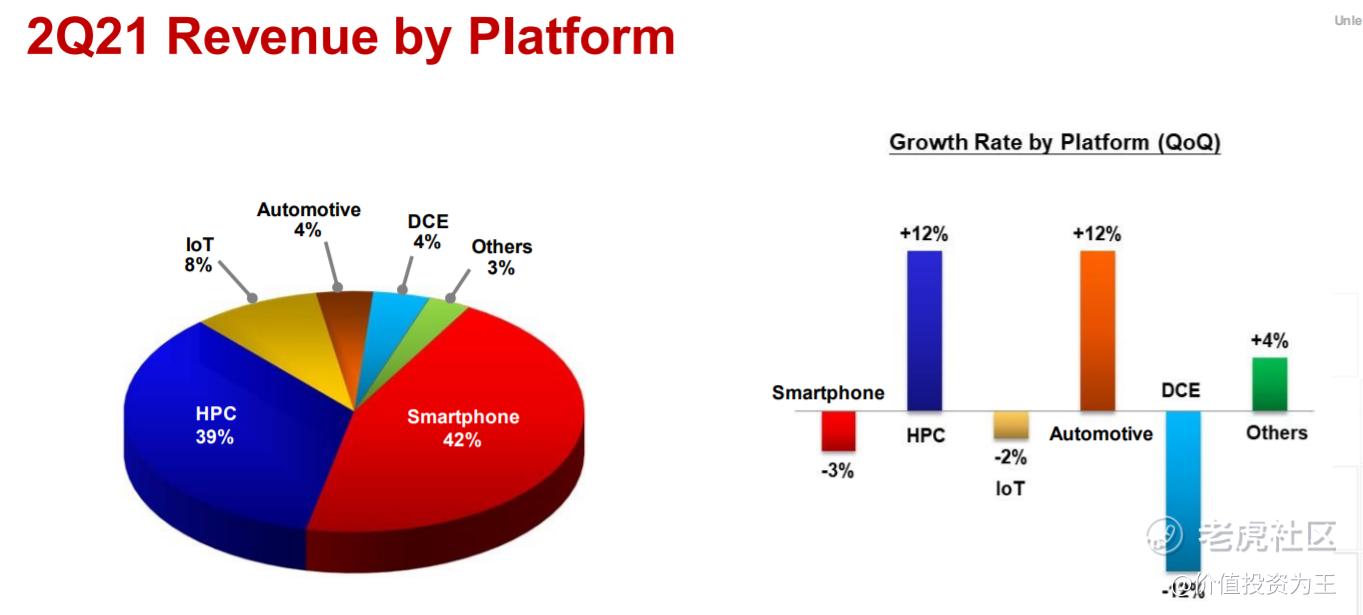

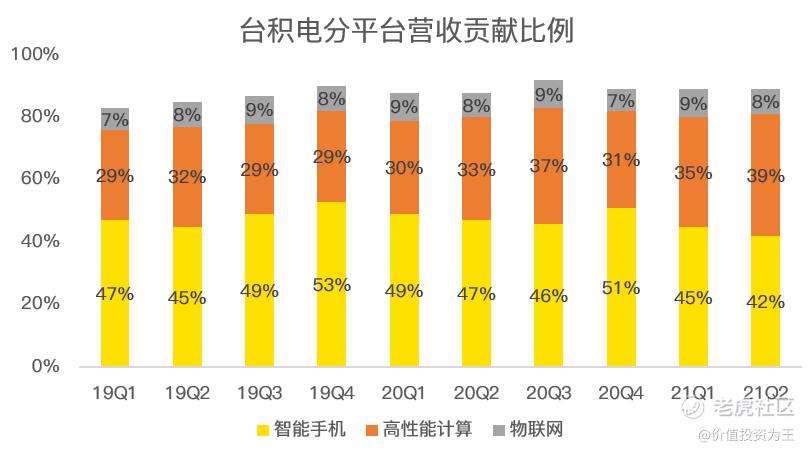

In terms of platforms, smart phones contributed 42% of revenue, high-performance computing contributed 39%, Internet of Things 8%, autonomous driving 4%, and digital consumption and others contributed 7% in the second quarter.

According to historical data, smart phones generally adopt the most advanced manufacturing technology and contribute the most powerful profits, but the revenue contribution of 42% is still slightly lower than before, which shows that the demand for smart phones is still cold in the second quarter.

Q3 and Annual Performance Outlook

Taiwan Semiconductor Manufacturing predicts that in the third quarter, there will be strong demand for 5nm and 7nm processes in smart phones, HPC, Internet of Things and automotive chips, which will promote the growth of Q3 performance. It is estimated that the revenue range in the third quarter will be between 14.6-14.9 billion US dollars, with a year-on-year growth rate of 20.3%-22.8%, and the gross profit margin will be between 49.5% and 51.5%, which is the same as the forecast value in the second quarter.

According to the quarterly guidance given by the company, profitability will still be under pressure.

Due to the lack of core, the demand for advanced manufacturing processes continues to be strong, and it is expected that the production capacity will remain tight in 2021 or last until 2022.

Therefore, Taiwan Semiconductor Manufacturing expects its revenue to increase by more than 20% in dollar terms in 2021.

Summary:

Taiwan Semiconductor Manufacturing's second-quarter financial report was no surprise. In terms of revenue, the market had already learned in advance through monthly income. On the contrary, the second-quarter financial report was slightly frightened, and the growth rate of net profit began to be lower than that of revenue, resulting in a situation of increasing income without increasing profits.

From the valuation point of view, Taiwan Semiconductor Manufacturing's price-earnings ratio in 2021 is about 32 times, which is in a historically high range.

Although profitability is under pressure, from the perspective of a longer period, smart phones, high-performance computing and Internet of Things will still maintain strong market demand. Superimposed Taiwan Semiconductor Manufacturing will mass-produce 4 nm in this quarter and 3 nm in 2022. It is estimated that there is still room for improvement in the revenue share of advanced technologies of 7 nm and below.

As rumored in the market, Apple is full of confidence in iPhone13 due to the hot sale of iPhone12, so it has greatly increased its orders. The first orders of iPhone13 are expected to reach 90 million to 100 million units, an increase of 10% to 20% over the 80 million orders of iPhone12.

As long as Taiwan Semiconductor Manufacturing can stay ahead of the process, the temporary drop in profitability will not affect the long-term value.$Taiwan Semiconductor Manufacturing (TSM) $

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- L34rn3r5·2021-07-16TOPLong run should be good. Fundamental well coy. Ignore short term noise40Report

- Viboon·2021-07-16TOPSemiconductor Manufacturing expects its revenue to increase by more than 20% in dollar terms in 2021 !!!19Report

- Mhong·2021-07-16TOPLiKe and comment17Report

- WinnerSG·2021-07-16TOPSemicon sector has been positive on the shortage story for a long time. This could mark the end of the run. At least in the short term. No positive story goes on forever.11Report

- Gobbler·2021-07-16TOPWorldwide, chips are in shortage due to just in time inventory8Report

- LimLS·2021-07-17TOPTSM is good and has chips in demand by everyone. But do take note they are trading at their historical high. They are worthy of their high PE but market sentiment will eventually decide it's worth3Report

- DavvYap·2021-07-17TOPHold it long enough and it will become next FAANG2Report

- Teo69·2021-07-16Like and comment pls5Report

- Meshaarias72·2021-07-18Like n comment pls3Report

- 88wlam88·2021-07-16Competitors are miles away,,no worries in the short teR….4Report

- Ndus·2021-07-16Thanks for sharing5Report

- tkj·2021-07-18this is ironical. Good companies with good results but stock price dropped. on the other hand, meme stocks with no fundamentals and essentially loss making saw prices shot up like nobody's businessLikeReport

- Dcagency·2021-07-16it’a in the growth market and with 3nm coming Up in 202…. outlook is good.2Report

- mandyt25·2021-07-16Win win to both TSMC & Apple ! ?3Report

- LUKIE·2021-07-19Good to learn that it's still the Handphone that's driving the industry. Seems that EV is still a long way away to be significant. ???LikeReport

- Yangli·2021-07-16Go for TSMC is you prefer long. It’s the investment for the future.1Report

- Mikaelocw·2021-07-20If you go for long term.... I could say Yes. Strong fundamental principle.LikeReport

- JoelSeah·2021-07-17ignore noise and hold2Report

- CKWong0572·2021-07-17this is a long term hold1Report

- awesome7281·2021-07-16long term invest, no wori2Report