Fed Decision, Big Tech Earnings Highlight the Busiest Week of the Summer

Last Week's Recap

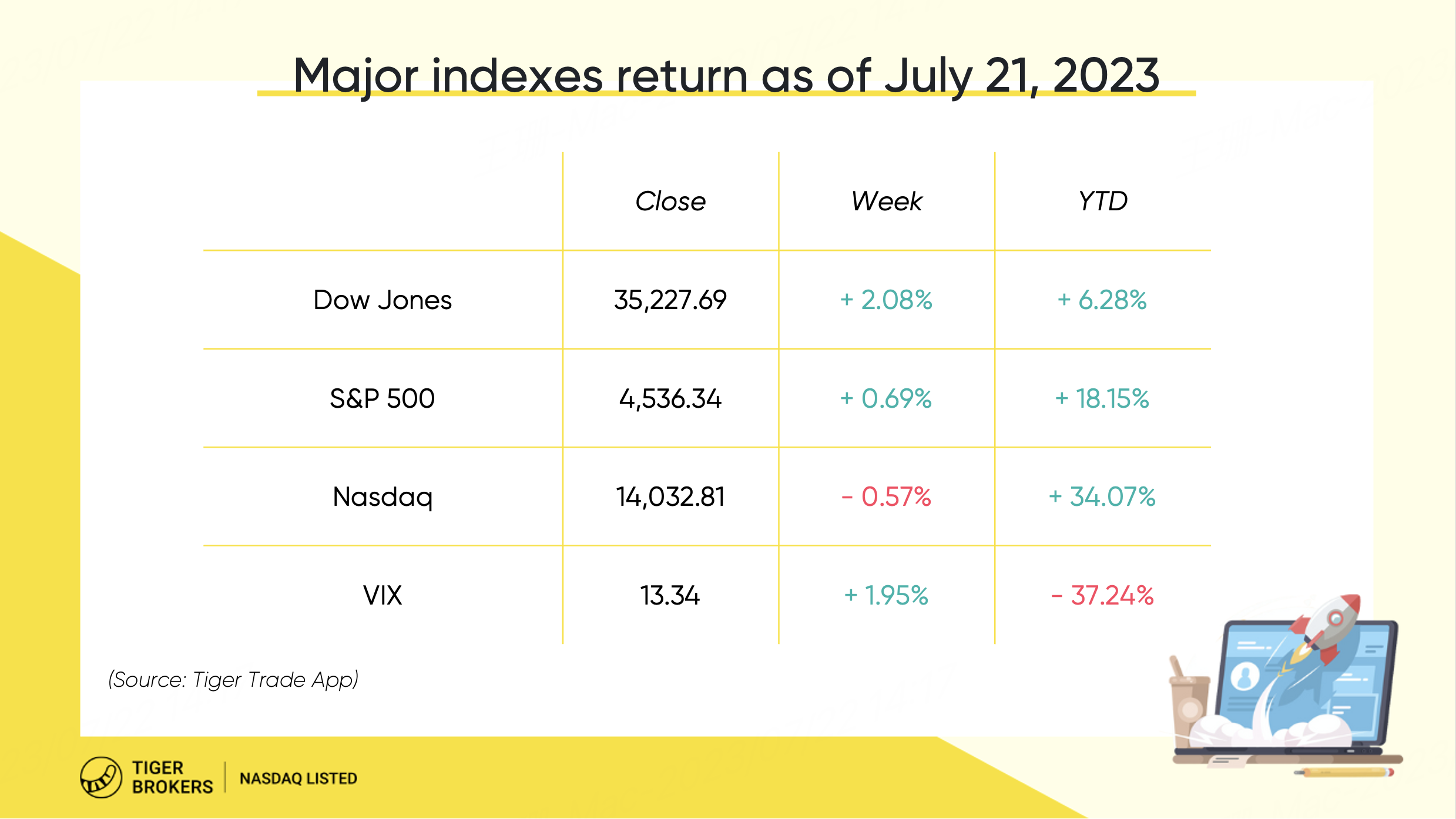

The US Market - The Dow posted a gain for the 10th straight session

Stocks were mixed last week as traders assessed the latest corporate earnings results. The Dow stretched its winning streak to 10 sessions despite earnings disappointments, its longest rally in almost six years. While the S&P 500 added 0.69% and the Nasdaq fell 0.57% for the week.

Corporate earnings have been mixed thus far. 75% of S&P 500 companies that have already reported have exceeded analysts’ expectations, which is below the 5-year average of 77%, according to FactSet data.

The week's relatively strong close likely reflects optimism over receding inflation and widespread confidence the Federal Reserve is nearly done raising interest rates. The Fed's policy-setting meeting next week is expected to result in a quarter-point rate increase that many believe will be the final hike in a historically sharp monetary tightening cycle.

The US Sectors & Stocks - TSLA & NFLX led tech stocks pullbacks

8 of S&P 500 sectors gained for the week, leading by the energy and the healthcare sectors, which were up more than 3%. However, the communication services was the worst-performing sector as TSLA plummeted.

The S&P Banks ETF-KBE was up 6.76% last week, as the most banks exceeded market expectations in terms of revenue and profits, though variations exist across different business sectors. The impact of the Q1 "Silicon Valley Bank crisis" seems to be gradually fading. The regional banks have displayed outstanding performance, outperforming comprehensive big banks during this week of banking financial reports. The regional banks ETF-KRE was up 7.54% for the period.

Tesla (TSLA) tumbled nearly 10% after it released earnings, and pulled back 7.6% for the week. Its second quarter gross margin of 18.2% was below the expected of 18.8%. Still, Tesla beat earnings and revenue expectations. Tesla CEO Elon Musk signalled on Wednesday that he would cut prices again on electric vehicles in "turbulent times". The large price cuts have pressured Tesla's automotive gross margin, a closely watched indicator in the industry, but Musk has said Tesla would sacrifice margin to drive volume growth.

Netflix (NFLX) declined as much as 8% on Thursday after earnings, and lost 3% for the week. Netflix’s second-quarter sales rose 2.7% to $8.19 billion, coming in slightly below analysts’ projections. That was due in part to foreign exchange rates and to price cuts in some markets. The company’s forecast for third-quarter revenue of $8.52 billion was also shy of Wall Street estimates, which average $8.67 billion. The company said revenue from advertising and add-on memberships to people who share passwords were not material enough to offset other factors, such as a lack of price increases.

Microsoft (MSFT) rallied to reach an all-time high Tuesday after the software giant announced that its flagship Microsoft 365 Copilot will be offered to business customers at $30 per user per month. However, the stock price pulled back.

Dutch semiconductor equipment maker ASML reported a second-quarter net profit of 1.9 billion euros ($2.1 billion) that beat analyst expectations. CEO Peter Wennink increased the company's full-year sales growth forecast to 30%, up from a previous forecast of 25%.

Bloomberg indicated that Apple (AAPL) has stepped up its momentum in getting its generative AI work ready based on its internally-built Ajax framework. The company was also reported to have created an internal chatbot called AppleGPT. However, Apple has "yet to finalize" its generative AI strategy for its consumer ecosystem, in line with the more cautious cadence that Cook likely prefers.

TSMC’s surprise cut in 2023 revenue projections after posting its first quarterly profit decline in four years, underscoring the extent of a global slide in smartphone and PC demand.

Carvana (CVNA) continues to fly after the used-car retailer easily topped sales expectations for its latest quarter and announced a deal with noteholders to restructure its debt.

Hong Kong Market - HSI lost 1.74% for the week

Hong Kong stocks trim weekly loss, as traders turned more optimistic about Beijing’s pledge to support the private sector.

Still, the Hang Seng Index lost 1.74% to 19,075.26, while the Tech Index declined 2.94% for the week.

China will release detailed measures to boost development and investment in the private sector “very soon”, officials at the top economic planning agency said in a media briefing on Thursday. The government earlier last week unveiled a list of policy solutions and promises political backing for private firms.

Singapore Market - STI ended the week in the black

Local shares ended the week in the black. The benchmark Straits Times Index rose 0.91% to close at 3,278.30.

Now it is time once again for the next earnings season. Singapore airlines (SGX: C6L) 、Keppel (SGX: C6L) and UOB (SGX: U11) will release quarter results next week.

Australian Market - The unemployment rate remained at 3.5% in June

The Australian market was weaker on higher chances of interest rate rises from central banks after continuing strength in job markets, although the ASX 200 was still up by 0.1% for the week.

Some of the bigger share price falls were among gold mining shares as the rampaging US dollar forced the price of gold lower.

The unemployment rate remained at 3.5% in June (seasonally adjusted), in line with the updated figure for May, according to data released by the Australian Bureau of Statistics (ABS).

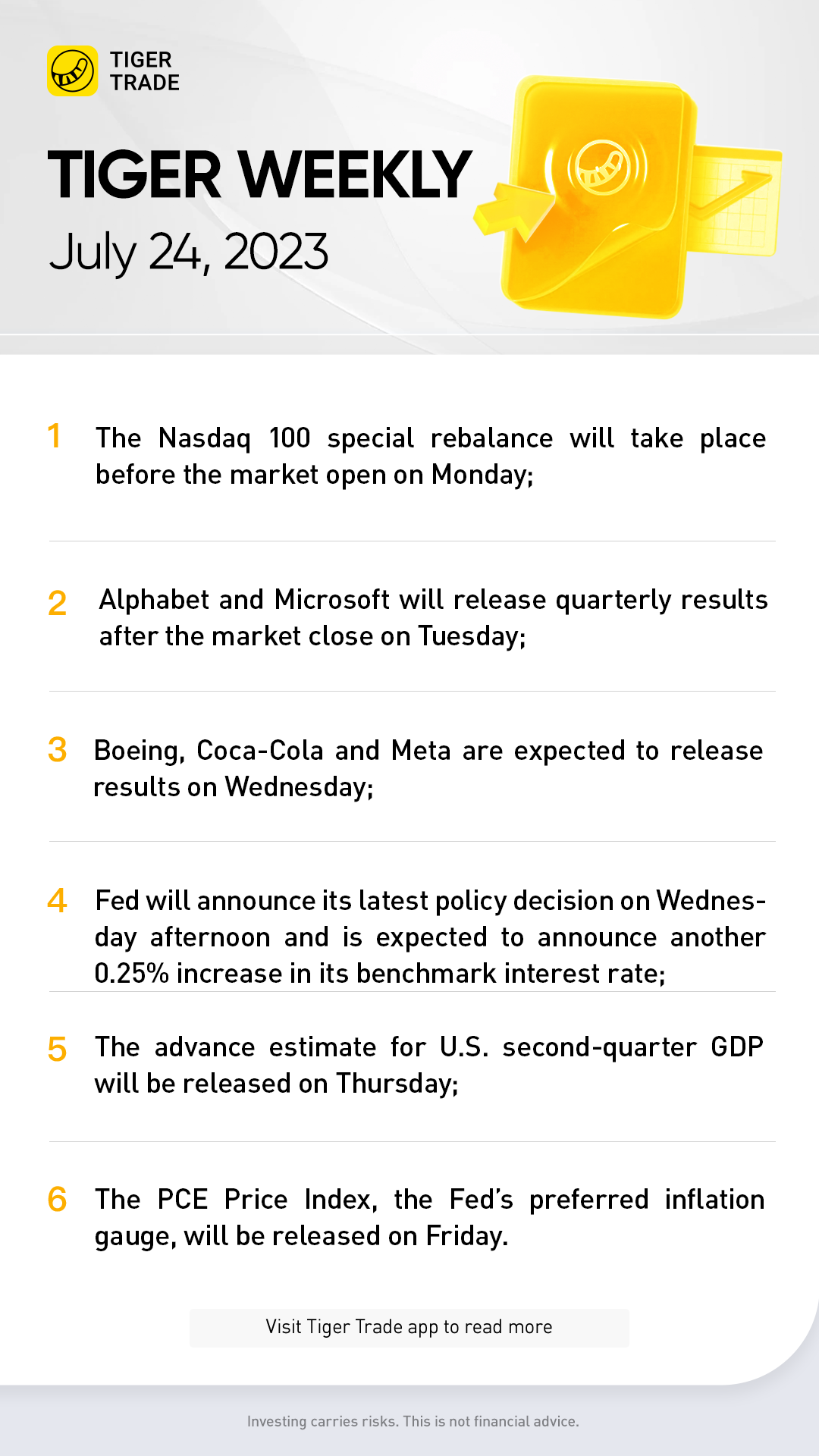

The Week Ahead

Macro Factors - Fed decision ahead the week

A Federal Reserve policy meeting and dozens of second-quarter earnings reports will roil the market this week.

A special rebalance of the Nasdaq 100 Index, which takes effect at the start of trading on Monday. The rebalance will dilute the impact of the largest stocks in the index, especially on Nvidia and Microsoft. The changes could force index funds and other investment products benchmarked to the Nasdaq 100 to adjust their holdings. The Invesco QQQ Trust (QQQ), which tracks the Nasdaq 100, manages more than $200 billion in assets.

The Federal Open Market Committee will convene on Tuesday and Wednesday, with a monetary-policy decision and press conference with chairman Jerome Powell due on Wednesday afternoon. Futures markets are pricing in overwhelming odds of a 0.25% increase in the federal-funds rate, to 5.25%-5.50%.

Many investors are anticipating the Fed will be “one and done” after its policy meeting in the week ahead, but a surprise move by the central bank or any hawkish commentary from Fed Chair Jerome Powell could potentially throw cold water on recent investor enthusiasm.

The rally themes in 2023 have been a resilient labor market and gradually declining pace of inflation growth; Big Tech profits, and the public and private sector response to the March banking crisis. While all three have been important, DataTrek co-founder Nicholas Colas said tech earnings are the most critical piece of the puzzle. “There is simply no other way for the S&P 500 to keep rallying,” he wrote. “Tech and Tech-adjacent names are 39% of the index. While we’re likely to meet this criteria in Q2 earnings season, it gets progressively harder for these companies to surprise on the upside as analysts reset expectations ever higher.”

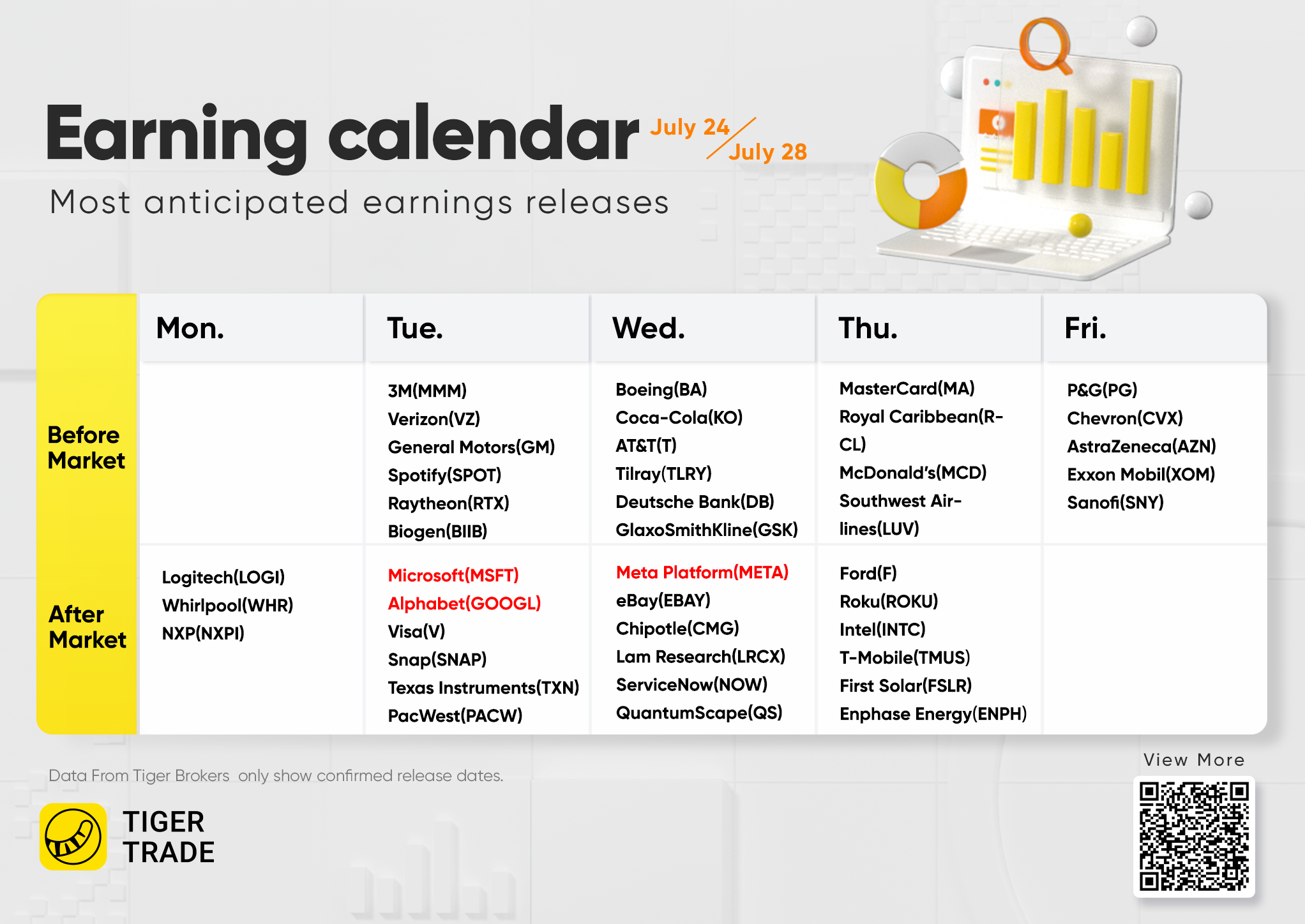

Earnings

The biggest week for earnings season is also up ahead, more than 150 S&P 500 companies are scheduled to report this week, including several tech giants: Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT) and Intel (INTC).

Thus far, 75% of the names that have reported have exceeded analyst expectations, FactSet data shows. However, that beat rate is below a three-year average of 80%, according to The Earnings Scout.

Beside of tech giants, General Motors(GM)、Coca-Cola(KO)、Boeing(BA) also give rise to investors.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- YueShan·2023-07-24okLikeReport