Alpine Immune Sciences: Going Strong But For How Long?

Suriphon Singha/iStock via Getty Images

A little less than a year ago I wrote an article about Alpine Immune Sciences (NASDAQ:ALPN), explaining the reasons why I still believed in the company, after the ditching of their main trials, based on the death of their second patient. Since then, the stock has run nearly 150%. Too bad I got out around the $11 price point.

Recently, the company reported their financial results for the second quarter of 2023, showing a loss of $0.27 per share, beating estimates by $0.10 per share, and revenues of $8.6 million, beating estimates by $1.5 million. On a year-over-year basis, the company saw its revenues increase by 65% and a nearly 30% reduction in its net loss.

Although I continue to be supportive to the company, I believe that there may be a minor to medium pullback imminent, mostly due to broader market reasons. Within the early pharma universe, this is a quality company. However, it has its pros and cons and bears the increased risk associated with these type of companies.

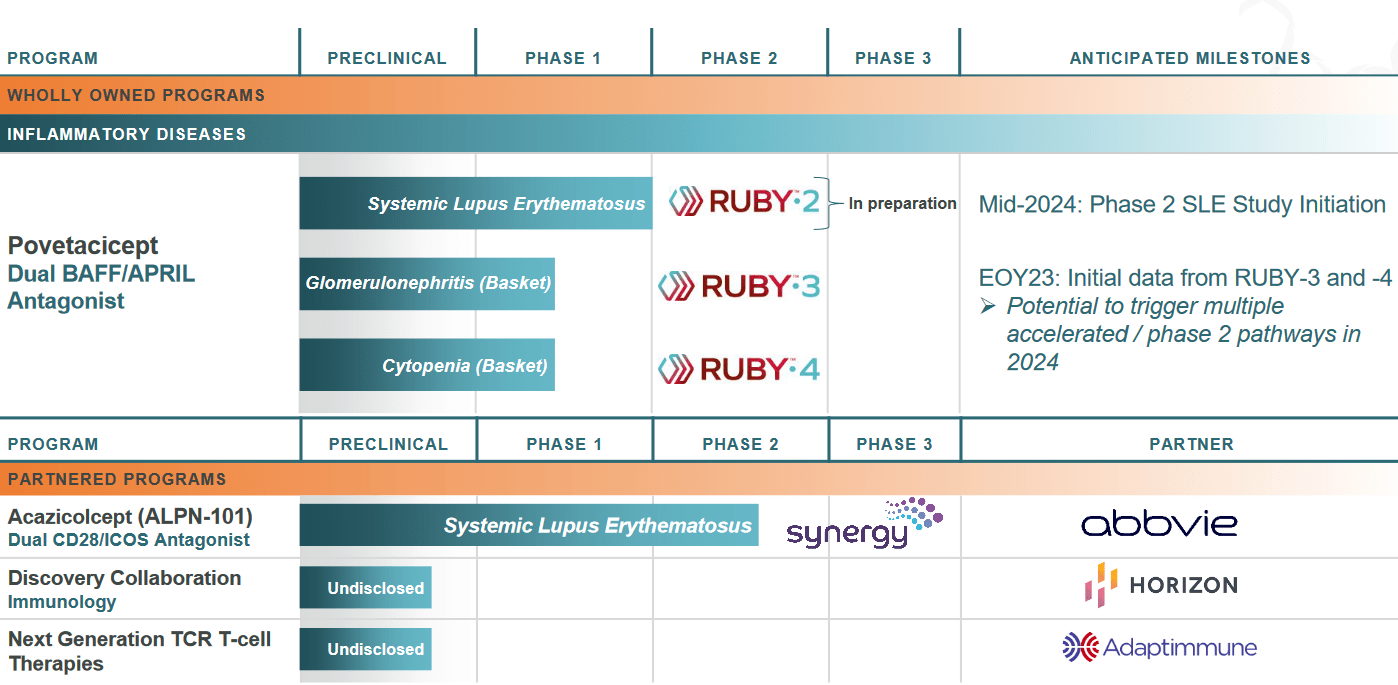

The Good: Smoothly progressing trials

The company is continuing to enroll patients to its RUBY-3 and RUBY-4 trials of their ALPN-303 dual B - cell cytokine antagonist. Alpine is testing the safety and efficacy of ALPN-303 on various conditions, such as systemic lupus erythematosus, immune thrombocytopenia, autoimmune hemolytic anemia and other diseases. Preliminary clinical data of their RUBY-3 study, regarding autoimmune glomerulonephritis, including IgA nephropathy, lupus nephritis, and primary membranous nephropathy, will be presented in the American Society of Nephrology Annual Kidney Week Meeting in early November.

The other drug candidate, namely the ALPN-101, is being developed by Alpine, while the company has a deal with AbbVie (ABBV) for the commercialization of the final product and several milestones along the way. As we can see in the image listed below, it is currently in Phase 2 of its development.

Alpine Immune Sciences Pipeline (Alpine Immune Sciences August 2023 Investor Presentation)

Speaking of partnerships, the company is also partnered with Adaptimmune for the development of their next gen TCR T-Cell therapies. As a matter of fact, these partnerships lead J.P. Morgan to issue a bullish rating to the stock, with a price target of $17.

The (not so) bad: Dilution creates adequate cash runway

The problem with early - stage pharma companies is that they don't generate earnings and they are often caught in a liquidity spiral. They often opt for share offerings and maybe more debt, diluting their shareholders in the process. The topping of this whole process is a reverse stock split of "many shares to one", in order to comply with NASDAQ policies.

Something similar is going on with Alpine Immune Sciences. Based on the company's recent earnings report, they have a total of $240 million in cash reserves and short term investments. At the end of Q2 2022, the company had a total of $200 million in cash and investments. The company also reported a total of 49 million shares outstanding at the end of Q2 2023, while at the same period of 2022, this number was 31.5 million. The respective EPS figures for Q2 2023 and Q2 2022 were $-0.27 and $-0.60. We can therefore see that, while on a "per share" basis, the company seems closer to profitability, on an absolute level this is not the case. By multiplying the EPS figures with the total number of shares outstanding, we get a total loss of approximately $13.2 million and $18.9 million, for Q2 2023 and Q2 2022 respectively. However, the company said that they expect their current cash position to be able to continue to support their operations until 2025.

The Ugly: Increased expenses from progressing clinical trials

Early stage pharma companies also have one more thing to worry about: Clinical trial costs. Drug development is an expensive sport and as clinical trials are progressing, time and headcount required for completion is also increasing. Alpine posted R&D expenses of $19.2 million for the second quarter of 2023, while the respective figure for Q2 2022 was $17.6 million. As RUBY-2 study is heading into Phase 2 and ALPN-101 is progressing, also in Phase 2, the company's research and development expenses are expected to increase exponentially. It should also be mentioned that the company expects that any promising data from RUBY-3 and RUBY-4 studies, will also trigger Phase 2 pathways in the next year.

Bottom Line:

I have been supportive to Alpine Immune Sciences for several years, since before their collaboration with AbbVie was announced. And indeed, the management seems to be doing a great job here with all those collaborations. However, for various reasons I decided to sell my (small) stake in the company and at this point, I'm not considering any re-entry. As research and development costs are ramping up, dilution will continue to be elevated.

In addition, market volatility is high during this period, as geopolitical and economic issues emerge. I believe the current share price was clearly fueled by J.P. Morgan's report on the company. In the possible presence of some broader bad news (a higher CPI, another Fitch downgrade etc), investors will move their hard earned cash to safer havens in my view.

For all these reasons, I wouldn't jump in the company just yet, but I would hold my stake if I had one, placing a stop loss below the $12.50 price point.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.