Options Trading 101: Using Iron Condors In Rangebound Markets

Vladimir Zakharov

After a strong run in Q2, the major market indices have been trading in a more subdued fashion during the last month.

With Q2 earnings season mostly in the books, investors and traders may be considering new trading approaches in the stock market. One potential strategy to consider - especially for those market participants that are expecting sideways (aka rangebound) movement - is the iron condor.

Much like covered calls and short strangles/straddles, iron condors perform optimally when the underlying trades sideways during the life of the options. In fact, the iron condor is essentially a variation of a short strangle, but with less risk.

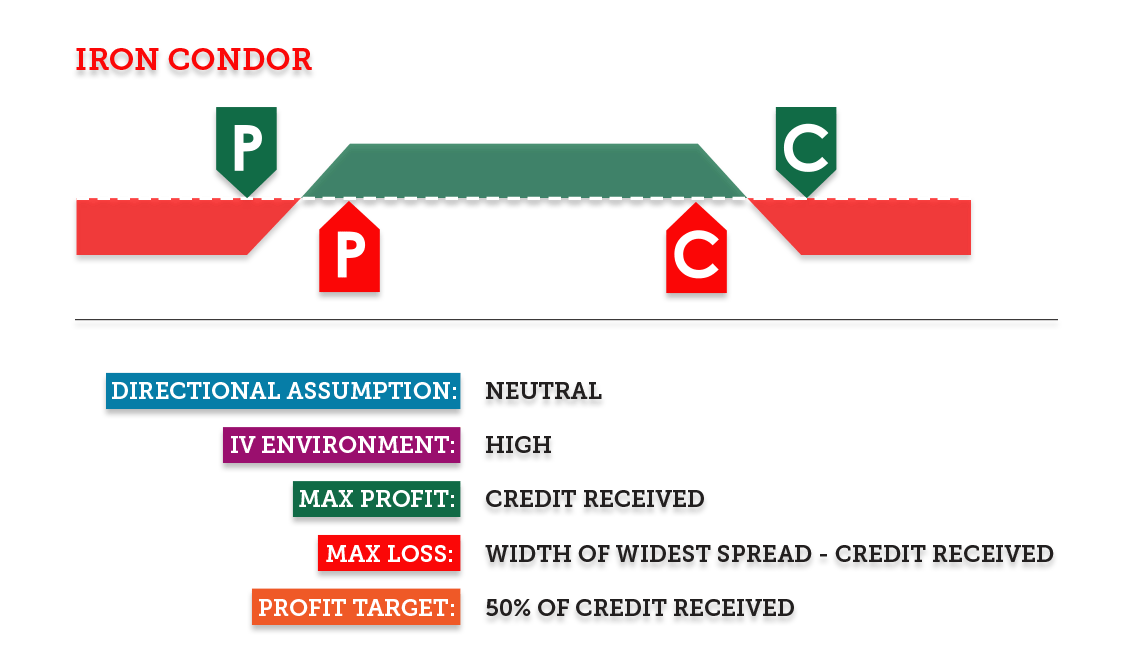

An iron condor is constructed by combining a short strangle with a long strangle - the latter offering protection against a big move in the underlying.

Unlike a pure short strangle, an iron condor is a defined-risk position, which means the worst-case scenario (i.e., maximum potential loss) is known prior to trade deployment.

Setting Up an Iron Condor

Imagine hypothetical stock XYZ is currently trading for $50/share, and an investor or trader believes the stock will trade in rangebound fashion during the next 30 days.

If the investor or trader holds an existing long position in XYZ, he/she might consider deploying a covered call (i.e., a short call against an existing long stock position) to leverage his/her rangebound outlook.

But if the investor or trader does not have an existing long stock position, and doesn't want to initiate a long stock position, then an iron condor could be considered.

Assuming the investor/trader thinks that XYZ will trade between $45 per share and $55 per share during the next 30 days, he/she could deploy an iron condor by executing a short strangle using an out-of-the-money (OTM) short $45-strike put and an OTM short $55-strike call.

In order to complete the iron condor, the investor/trader would simultaneously deploy a long strangle along with it. For example, using the $40-strike OTM put and the $60-strike OTM call.

Taken all together, the iron condor is therefore constructed using four different options positions in the same underlying and the same expiration cycle. It should be noted that each leg of the position should have the same number of option contracts.

tastytrade

Now let's walk through a practical example:

- Sell 1 OTM Call Option: Sell a call option with a strike price of $55 for a premium of $2.00.

- Buy 1 Further OTM Call Option: Buy a call option with a strike price of $60 for a premium of $1.00.

- Sell 1 OTM Put Option: Sell a put option with a strike price of $45 for a premium of $2.00.

- Buy 1 Further OTM Put Option: Buy a put option with a strike price of $40 for a premium of $1.00.

In terms of options premium, the above trading structure results in a net credit, as outlined below:

- Total premium received from sold options = $2/sh (from call) + $2/sh (from put) = $4/sh or $400/contract

- Total premium paid for bought options = $1/sh (for call) + $1/sh (for put) = $2/sh or $200/contract

- Net premium received = $400 (received) - $200 (paid) = $200

In an ideal situation, the investor/trader will keep the entire $200 in net premium, which occurs if the underlying is trading anywhere between $45 and $55 at expiration.

Stated differently, the maximum profit occurs when all the options expire worthless, which will happen if the underlying remains within the range defined by the strike prices of the short options. In this case, that's the $45-strike put and the $55-strike call.

Now let's examine three different outcomes involving a best-case scenario, a middle-case scenario, and a worst-case scenario.

Best Case Scenario

At expiration, the stock is trading anywhere between the short strike prices of $45 and $55. In this case, all of the call options and the put options expire worthless:

- Keep the entire net premium received of $200

Middle Case Scenario

Imagine that, at expiration, the stock is trading at $56/share. In this case, the $55 call option will therefore be worth $1 (intrinsic value). However, all other options expire worthless. That means the investor/trader will have to buy back the $55 call for $1/sh of $100/contract, offsetting half of the initial net premium $2/sh or $200/contract:

- Profit = $200 (the initial net premium) - $100 (cost to buy back call) = +$100

Worst Case Scenario

Imagine the stock is trading at $61/share at expiration. This is the worst-case scenario because the underlying has broken through the short strike of the $55 call, which creates a loss. However, this example also illustrates how the long $60-strike call offers some degree of protection, especially when the underlying breaks through $60/share.

The net result of this scenario represents the maximum potential loss of the position:

- Loss = $200 (the initial net premium collected) - $500 (loss from the short $55 call)

- Loss = -$300/contract

The net loss would have been exactly the same had the underlying stock dropped to $39/share, instead of rallying to $61/share.

Parting Shots

Depending on one's outlook and risk profile, the iron condor may be suitable for investors and traders who expect rangebound or sideways movement in a given underlying.

That's because the iron condor performs optimally when the underlying trades within a specific range during the life of the options.

As a reminder, all options lose value over time due to time decay, which benefits sellers of options. Therefore, it may be advantageous to set up an iron condor when there's enough time for time decay to work in one's favor, but not so much time that it allows for significant price movements in the underlying asset.

As always, investors and traders that are new to options - or new to the iron condor structure - may want to mock trade (i.e., paper trade) this strategy before deploying it "live" in the markets. Mock trading provides for important insight into how a given position or product behaves in the market, without the risk of capital losses.

This article is courtesy of Luckbox magazine.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.