Down 60%, Yielding 6%. Should You Buy UGI?

MicroStockHub/iStock via Getty Images

Introduction

It's time to talk about UGI Corporation (NYSE:UGI), one of America's largest regulated gas utilities. The stock is down more than 30% year-to-date, bringing the total selloff from its all-time high to 60%. The company now yields 6.1%.

This begs the question: should we start buying UGI?

After all, the company has a strong track record of generating shareholder value. Prior to the pandemic, the stock had beaten the S&P 500 (SP500) by a wide margin, thanks to consistent growth and generating a big part of its income from less-cyclical operations.

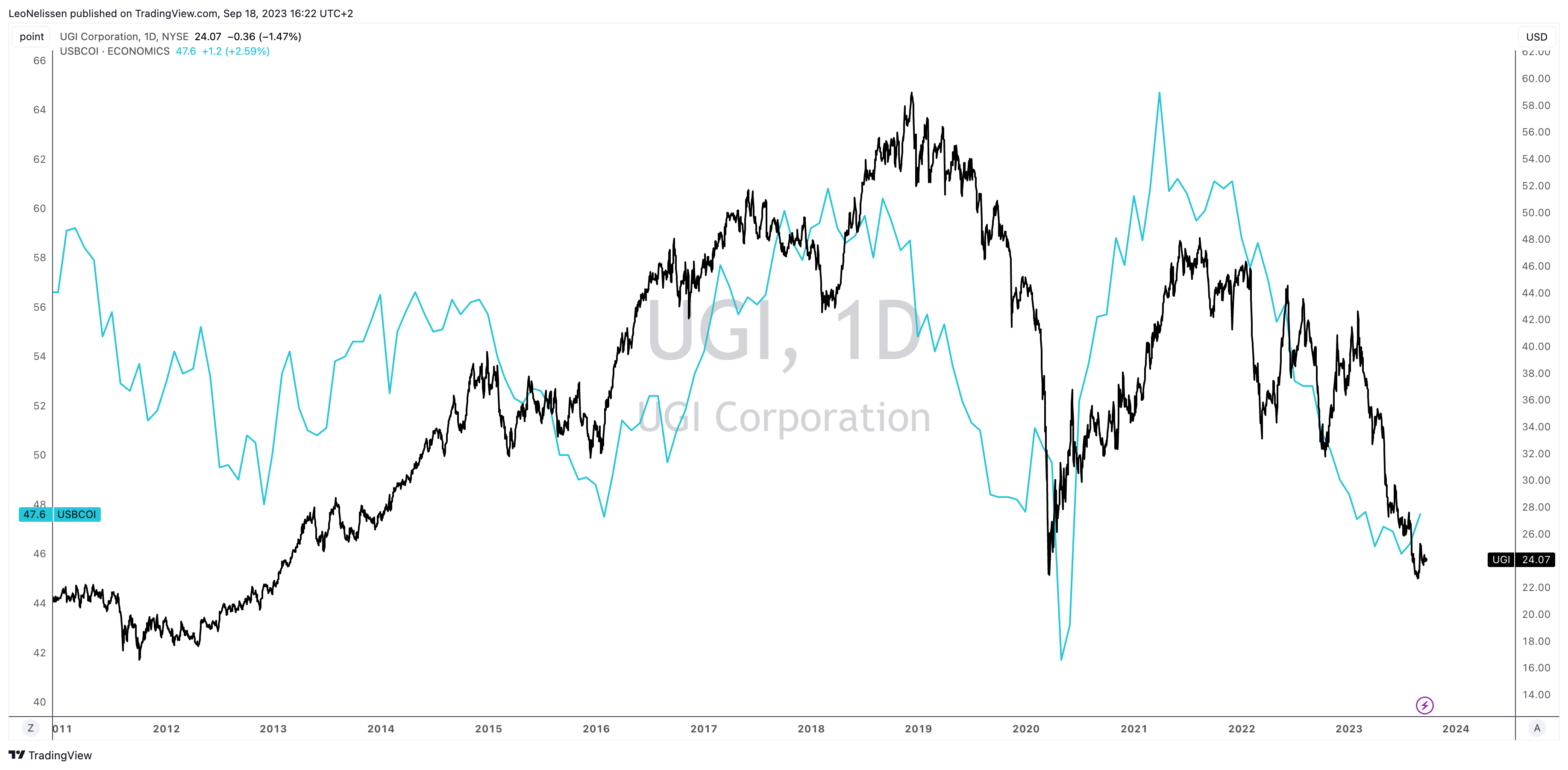

Data by YChartsNow, its stock price is at a decade-low.

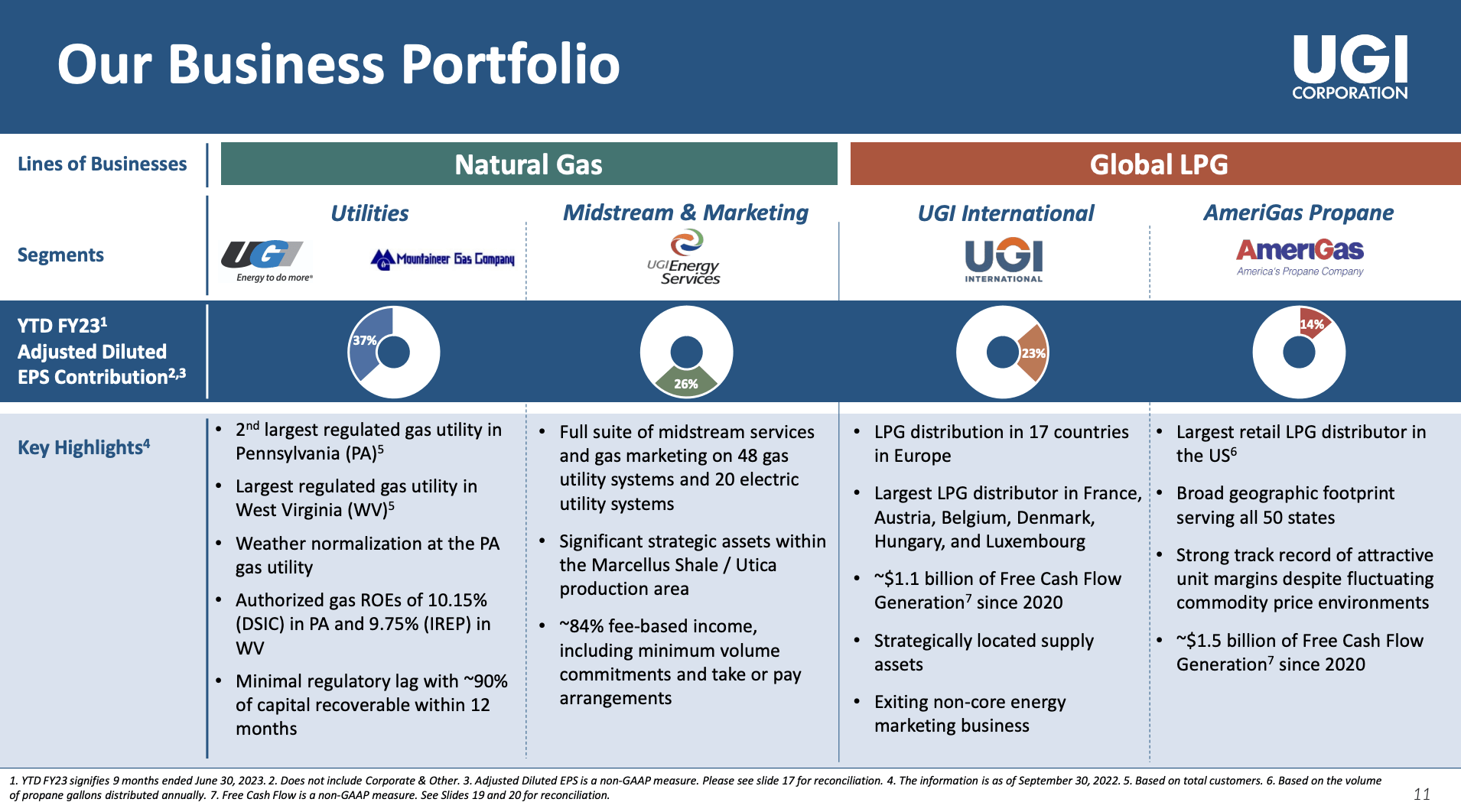

A Not-So-Traditional Utility Company

Incorporated in Pennsylvania in 1991, operates as a member of the regulated gas utilities industry.

The company, whose history goes back much further than 1991, is far from a traditional utility company. It services more than 18 countries and 2.5 million customers through a number of major subsidiaries and two major business segments.

Roughly 63% of the company's earnings come from its Natural Gas business, which includes its utilities business and its midstream assets. In the utilities segment, the company is the 2nd-largest regulated gas utility in Pennsylvania and the largest gas utility in West Virginia.

Its midstream segment adds significant stability through 84% fee-based income, including minimum volume commitments and take or pay arrangements.

UGI Corporation

The company also has a Global LPG business.

AmeriGas Propane, UGI's domestic propane distribution business, serves customers in areas where natural gas is not readily available. They distribute propane to residential, commercial/industrial, motor fuel, agricultural, and wholesale customers.

Approximately 85% of sales are to retail accounts and 15% to wholesale.

The ACE program and Cynch propane home delivery service are significant components of the company's business. Retail deliveries of propane are typically made via bobtail and rack trucks, and portable cylinders are also used.

UGI Corporation

UGI's AmeriGas Propane procures propane from approximately 170 sources domestically and internationally, including the spot market.

They use a combination of increased regional storage and various transportation methods to ensure propane availability and offset localized supply/demand imbalances. About 99% of their propane supply is purchased under supply agreements with terms of one to three years.

UGI International serves customers overseas.

What this means is that the company is only partially defensive. Unlike its major peers, a big part of its business is cyclical. There's nothing wrong with that. It's just a factor that tends to drag the stock down during economic downcycles.

Comparing the UGI stock price to the leading economic indicator, the ISM Manufacturing Index, we see that UGI is not a great spot to be during economic downtrends.

TradingView (UGI, ISM Index)

Right now, investors are in the second major selloff since the 2018 stock price peak.

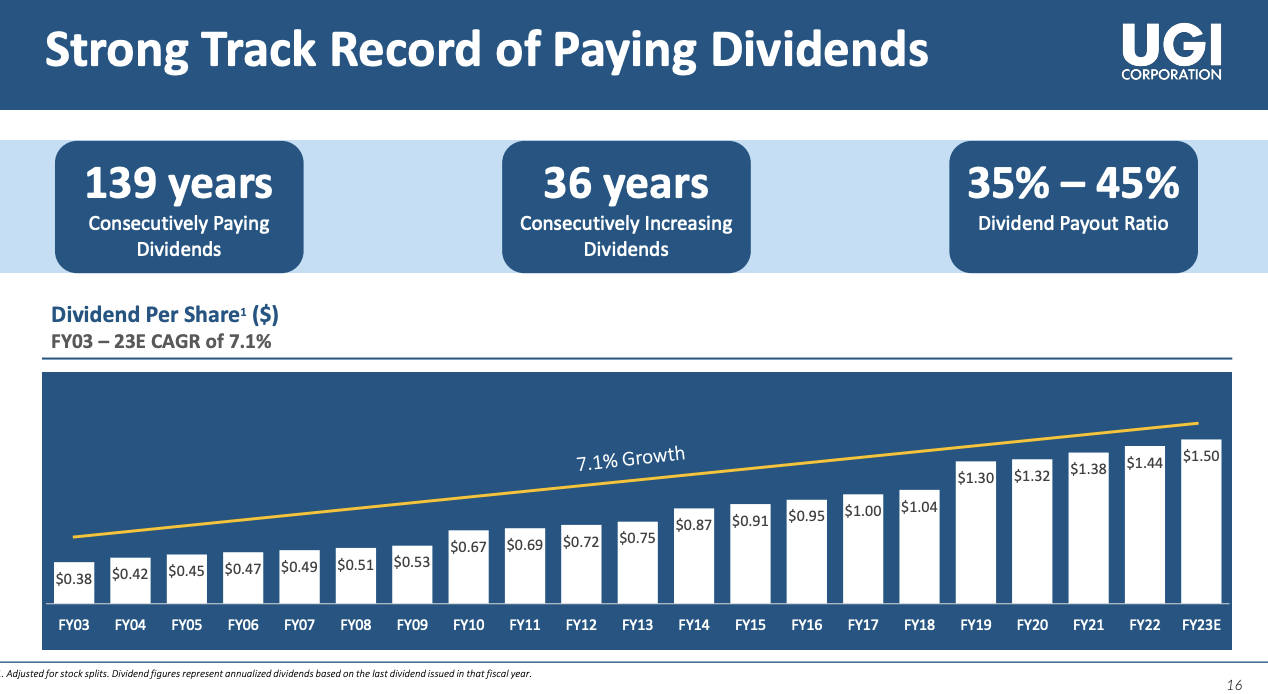

Before we dive into its earnings, one thing that sets UGI apart is its dividend.

The company has paid a dividend for 139 consecutive years. It has hiked its dividend for 36 consecutive years, making it a dividend aristocrat.

UGI Corporation

Thanks to consistent earnings growth, the company was able to compound its dividend at 7.1% per year since 2003, maintaining a healthy 35% to 35% payout ratio.

On May 3, the company hiked its dividend by 4.2%. It now yields 6.1%.

Lower dividend growth is no surprise, as the company's earnings growth is expected to slow.

Analysts expect the company's earnings per share to average $2.95 over the next two years ($2.96 in 2024 and $2.94 in 2025).

This translates to an earnings yield of 12.2% and a dividend payout ratio of 50%, which increases the likelihood of significantly lower dividend growth going forward.

What's Going On At UGI?

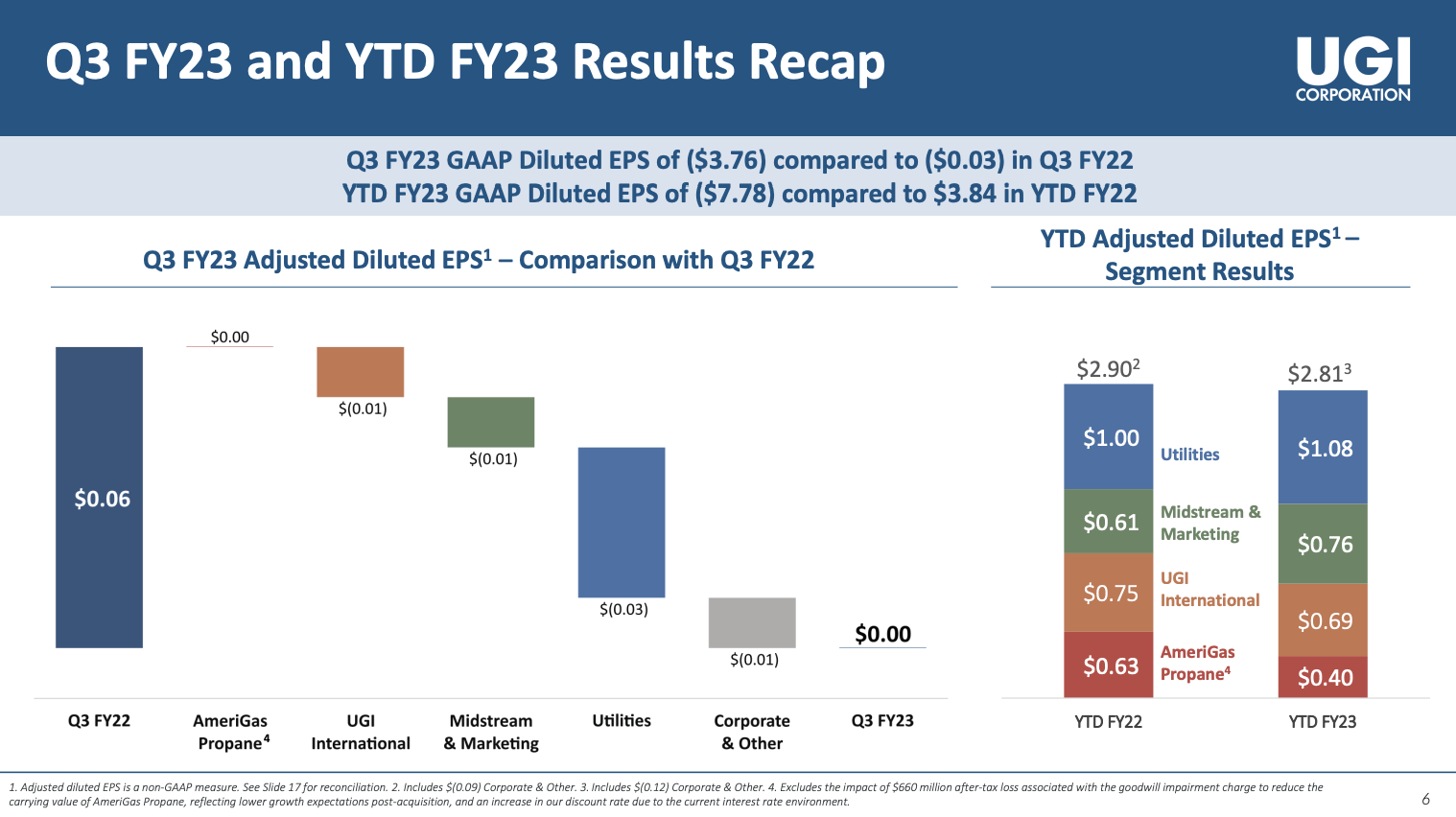

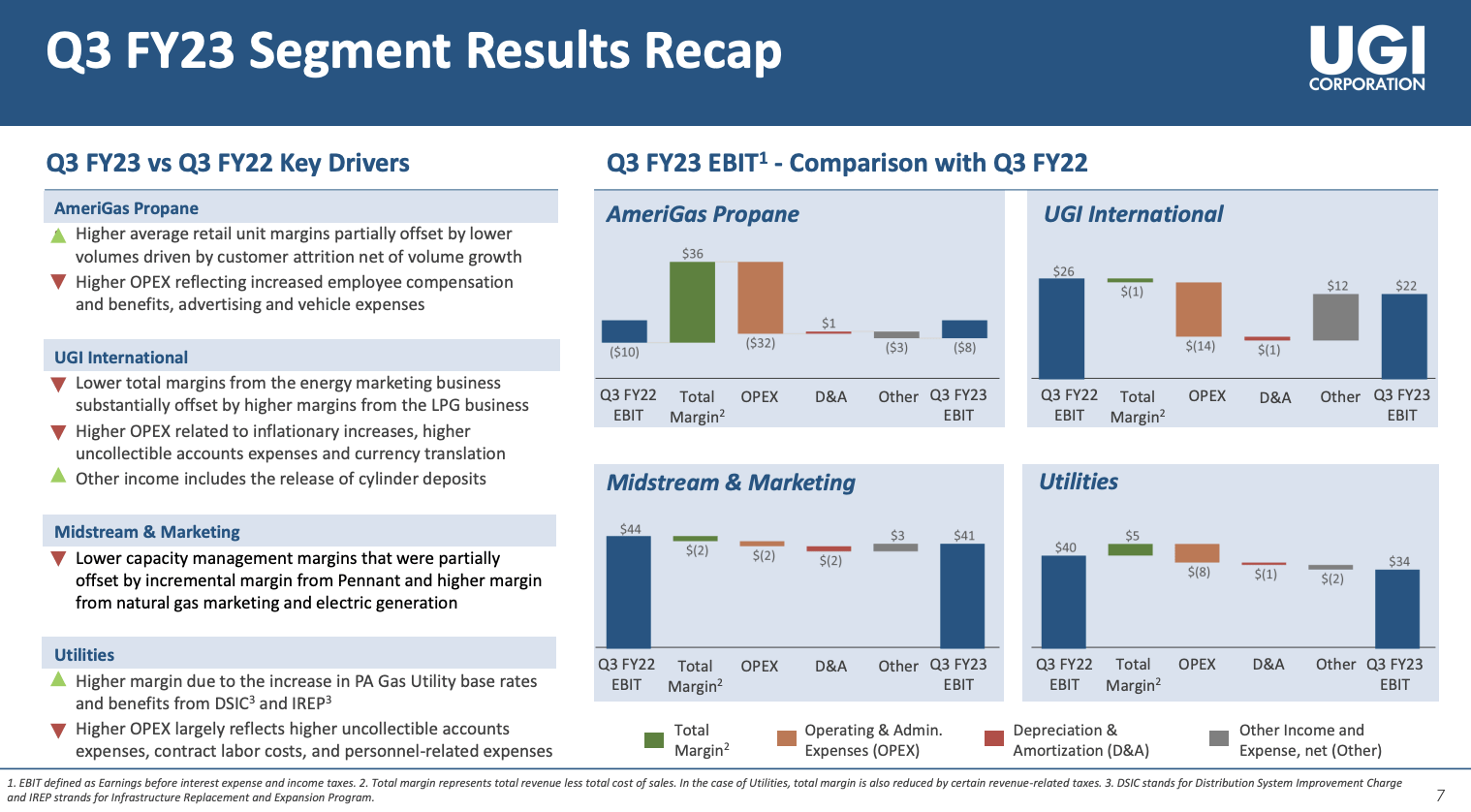

In the third fiscal quarter of 2023, the company reported adjusted diluted earnings per share of $0.00, which is a decrease from $0.06 in the previous year.

UGI Corporation

- AmeriGas remained flat in comparison to the prior year due to higher margins offsetting increased operating and administrative expenses.

- UGI International saw a decrease of $0.01, despite higher LPG margins, due to lower earnings from the non-core energy marketing business.

- The midstream and marketing segment also declined by $0.01 due to a reversal of capacity management margins from the prior year.

- The utility segment performed lower than the previous year, mainly due to higher operating and administrative expenses during the quarter.

Additionally, the company recorded a pre-tax non-cash goodwill impairment charge of approximately $660 million related to AmeriGas, reflecting lower growth expectations post-acquisition and an increase in the discount rate due to the current interest rate environment.

UGI Corporation

On a year-to-date basis, the company's natural gas businesses showed an increase of $0.23 in earnings per share, primarily due to higher gas-based rates, benefits from weather normalization, incremental margin from acquisitions, and higher margins from natural gas marketing activities.

Unfortunately, these gains were partially offset by higher operating and administrative expenses.

The global LPG businesses saw a decrease of $0.29 on a year-to-date basis, mainly due to lower volumes, capacity constraints, and investments in distribution metrics at AmeriGas.

Essentially, we see a major impact from its cyclical businesses, while some weather-related benefits were offset by expense-related issues.

- AmeriGas reported a 6% decrease in LPG volumes due to softening demand, customer attrition, and conservation efforts.

- UGI International saw a 2% increase in LPG volumes due to colder weather, but this was offset by lower margins from the non-core energy marketing business and higher operating expenses.

As a result, during the 3Q23 earnings call, the company highlighted its focus on rationalizing and optimizing its cost profile in response to the challenging global environment.

The company aims to simplify processes, leverage technological improvements, and use digital innovation and analytics to create operational efficiencies. These actions are expected to reset the cost baseline, achieve sustainable cost savings, generate incremental cash flow, and ultimately enhance shareholder return.

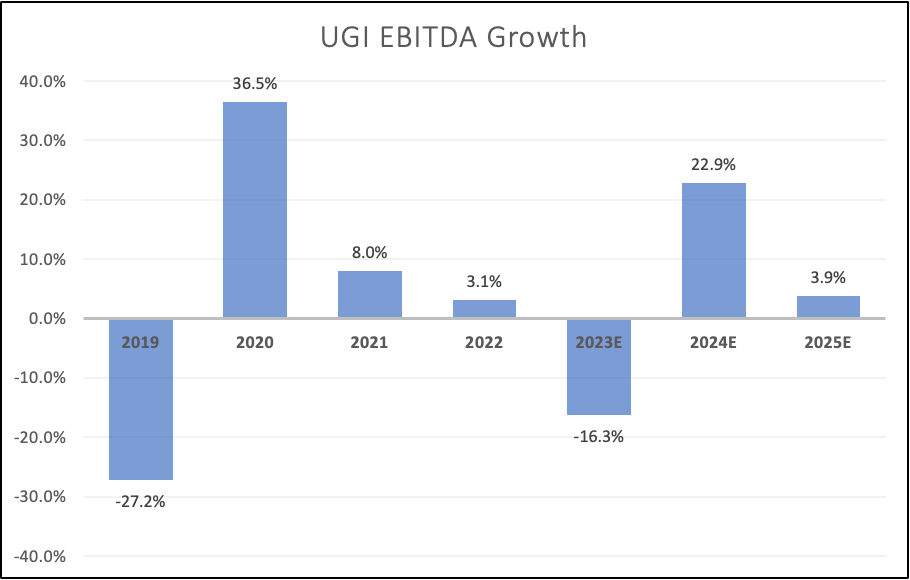

Analysts expect the company to grow its EBITDA again next year, followed by a subdued growth rate in 2025.

Leo Nelissen (Based on analyst estimates)

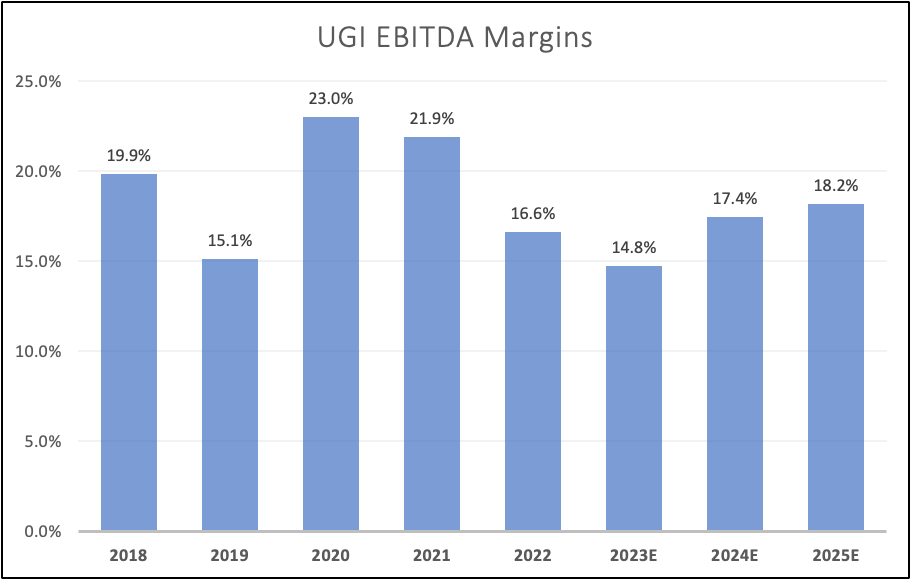

EBITDA margins are expected to bottom below 15% this year, followed by a gradual increase to 18.2% by 2025.

Leo Nelissen (Based on analyst estimates)

So, what does this mean for the valuation?

Valuation & Personal Opinion

Despite selling off, the valuation is less attractive than I expected before researching this company. UGI is trading at 8.6x NTM EBITDA. While EBITDA will likely pick up considerably the moment global economic growth rebounds, this valuation is fair for a company with likely low-single-digit long-term annual EBITDA growth.

Data by YChartsAnalyst estimates vary. The consensus price target is $32, which is 33% above the current price. The ratio between the highest and lowest estimates is at a multi-year high (ignoring a recent outlier).

Data by YChartsI agree that UGI is trading below its fair value.

The problem is that I cannot make the case for an investment in UGI. Although I believe that recovering economic growth will pave the way for higher growth and a continuation of satisfying dividend growth, there are better alternatives.

There's no need to buy a company that combines midstream assets, LPG distribution, and gas utility exposure.

I can buy a midstream company with a double-digit dividend yield, add a pure-play utility with a 5% yield, and buy companies with exposure to LPG and natural gas liquids.

For example, Enbridge (ENB) comes to mind. This Canadian giant will soon combine massive natural gas distribution exposure and North America's largest midstream network, with a yield of 8%. I covered ENB in a recent article.

Data by YChartsDon't get me wrong, I'm not trying to push anyone out of UGI. I just believe that there are better opportunities on the market.

Although, buying UGI's 6% at these levels has a high likelihood of paying off. I prefer to buy exposure in other companies with more focused business models - especially if we consider that energy price volatility comes with risks.

Depending on the terms of our contracts with suppliers as well as our use of financial instruments to reduce volatility in the cost of LPG and natural gas, changes in the market price of LPG and natural gas can create margin payment obligations for us and expose us to increased liquidity risk. In addition, increased demand for domestically produced LPG and natural gas overseas may, depending on production volumes in the U.S., result in higher domestic prices and expose us to additional liquidity risks. - UGI 2022 10-K.

If I had to build my own UGI, I would buy a company like ENB and combine it with an upstream driller with both oil and natural gas exposure, which benefits from strong natural gas demand growth, oil supply growth weakness, and energy problems in Europe. A company like Pioneer Natural Resources (PXD) could get the job done. It's my largest energy investment. I discussed PXD in this article.

Again, I'm just saying how I would deal with UGI, as I prefer to build my own conglomerates instead of buying companies that somewhat get stuck in the middle by diversifying too much.

Please feel free to disagree with me.

Takeaway

UGI Corporation presents an intriguing investment opportunity, but it's not without its challenges. The stock has seen a significant decline, offering a tempting 6.1% yield, and the company boasts an impressive history of dividend payments and growth.

However, UGI's diverse portfolio covering midstream assets, LPG distribution, and gas utilities makes it less appealing compared to more specialized alternatives in the market.

While there's potential for recovery with improving economic conditions, investors might find better prospects elsewhere.

In essence, investing in UGI Corporation at its current levels may pay off, but I believe there are superior opportunities out there, especially considering potential margin pressures in a volatile energy market.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.