HYG: Spread Over Treasuries Too Low For Comfort

champpixs

While the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA:HYG) still offers a great risk-reward outlook relative to US stocks, the decline in credit spreads leaves the ETF at risk from a reversal in risk appetite. The HYG has managed to post positive total returns even as Treasury yields have risen thanks to compressing credit spreads, but these spreads are now too low considering the deteriorating economic outlook and the threat of rising defaults.

The iShares iBoxx USD High Yield Corporate Bond ETF tracks the performance of the Markit iBoxx USD Liquid High Yield Index offers a yield to maturity of 8.3%. The ETF has a weighted average maturity of 4.8 years and an effective duration of just 3.6 years. The fund is highly diversified in terms of its exposure to individual credits as well as exposure to industry sectors, with consumer cyclicals the largest sector with a weighting of 21%, followed by communications at 17%. The expense fee of 0.48% is on the high side.

Default Rates And Credit Spreads To Rise As Economy Slows Further

The yield to maturity on the HYG is now an impressive 8.3%, yet the majority of this yield reflects the yield on equivalent maturity US Treasuries. The risk premium over USTs is now just 3.7%, and after expenses the yield above 5-Year USTs is just 3.2%. When we look at the long-term performance of the HYG, it has tended to underperform its expected returns based on its yield to maturity by 2% annually, which largely reflects the losses from bond defaults. Even if defaults remain at this average level, investors should expect to receive just over 1% per year above equivalent maturity USTs.

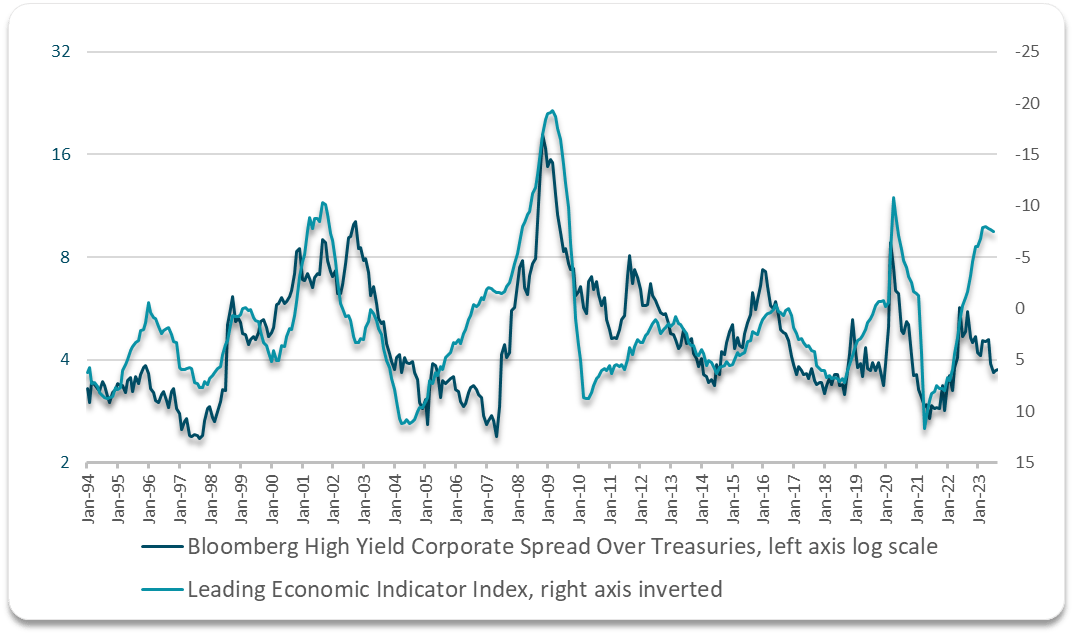

However, with real bond yields continuing to rise and nominal economic growth slowing, these are the conditions under which we should see bond defaults rise. The main risk to the HYG over the coming months comes not from any rise in defaults but a rise in credit spreads in anticipation of such. The following chart shows the spread of the Bloomberg High Yield Corporate yields over USTs plotted against the Conference Board's Leading Indicator Index. Low credit spreads contrast with the weak economic outlook, with an LEI figure of -7.5% consistent with historical credit spreads of over 10%.

Bloomberg, Conference Board

The performance of high yield bonds relative to equivalent maturity USTs has closely tracked confidence in the economy as measured by the Conference Board's Consumer Confidence Index. Again here we see a large disconnect, with high yield bonds continuing to outperform despite the drop in confidence.

Ratio of High Yield Corporate Total Return Relative To USTs and Consumer Confidence (Bloomberg, Conference Board)

Risk Appetite Is Breaking Down

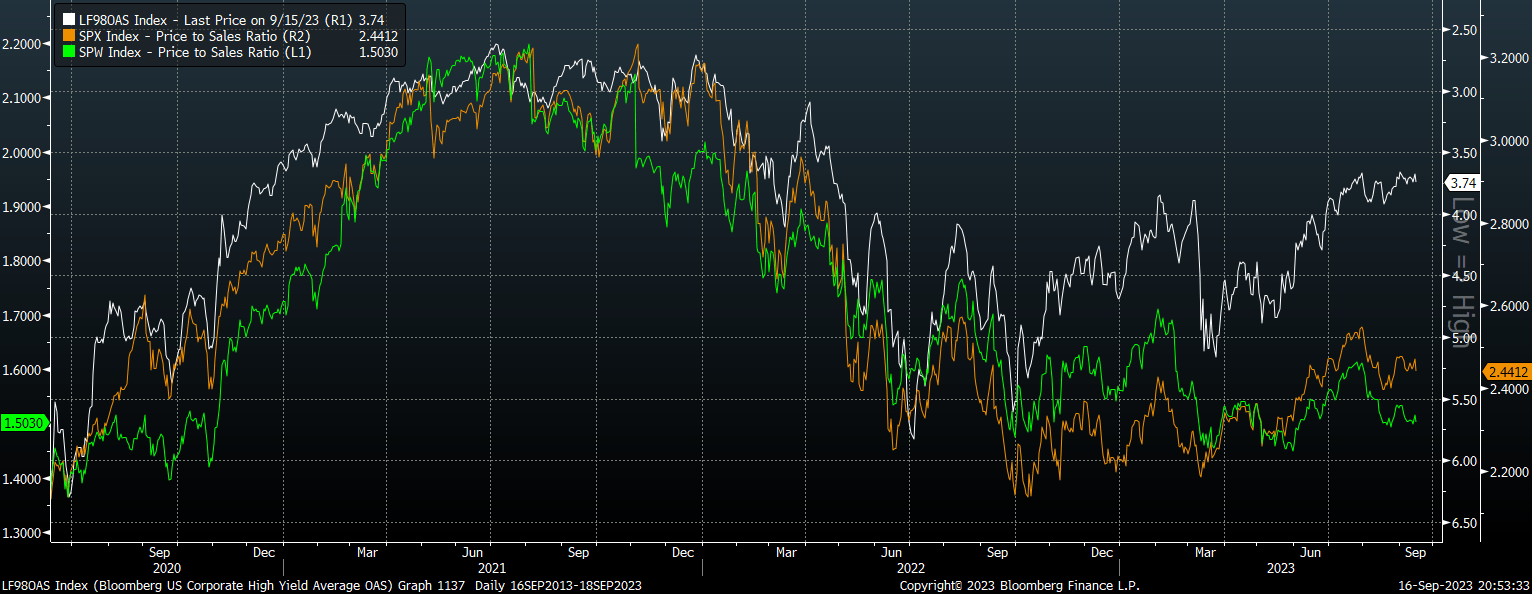

While high yield credit spreads show extreme levels of complacency about the slowing economy, there are signs that risk appetite is fraying at the edges. In fact, equity valuations have fallen substantially over the course of this year, and while this has typically driven up credit spreads in the past, they have continued to compress.

High Yield Credit Spreads Vs Price To Sales Ratio Of SPX And Equal Weighted SPX (Bloomberg)

Any rise in risk aversion that drives up high yield credit spreads is likely to also put downside pressure on Treasury yields therefore helping to provide support to the HYG. However, with relatively low duration and high credit risk the HYG is much more susceptible to changes in credit spreads than changed in UST yields.

Outperformance Likely Versus Stocks Due To High Risk Free Rate

To be clear, the HYG is still highly likely to outperform stocks over the coming years and generate respectable returns after inflation. However, this is due to the high real yield available on Treasuries themselves. The 5-year UST now yields 2.2% above 5-year inflation expectations as measured by the yield on Treasury Inflation Protected Securities, so even if defaults wipe out all of the credit spreads above USTs investors should still generate positive real returns. However, I would not buy the HYG at these levels other than as a relative value play against US stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.